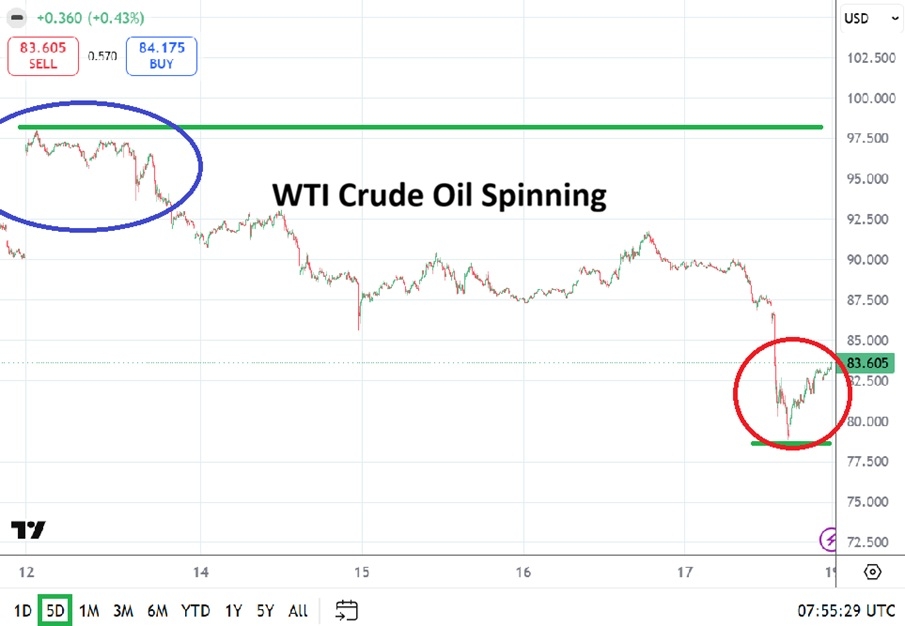

Markets began the week with a measured response to intensifying US–Iran tensions, even as the ceasefire showed visible signs of strain. The Dollar edged higher and oil prices rebounded, but broader markets remained composed, indicating that investors are not yet pricing a full shift toward conflict. The retreat of the “peace trade” is evident but incomplete. Oil’s move higher reflects a partial reintroduction of geopolitical risk, yet the absence of a sharper breakout above $100 suggests that supply disruption is not the base case. This balance is keeping risk sentiment broadly intact.

Equity markets in Asia reinforced this interpretation, trading modestly higher despite the negative headlines. The resilience underscores a prevailing view that while risks are rising, they have not yet crossed a threshold that would force a decisive repositioning. In FX markets, Dollar’s recovery has been notable but lacks conviction. For now, the move appears more corrective than directional, consistent with a broader market environment characterized by uncertainty rather than clear trend formation.

Beneath the surface, however, the ceasefire is being tested across multiple fronts. A series of escalating developments has weakened the foundation of the agreement, even if none has yet triggered a full breakdown in market expectations.

The naval blockade remains the most persistent point of contention. Iran views the continued US presence and restrictions as a violation of the ceasefire terms, while the US maintains that enforcement will continue until a final settlement is secured. This disagreement reflects a deeper impasse over sequencing and trust.

Meanwhile, the situation in the Strait of Hormuz has become increasingly volatile. The reversal from a brief reopening to renewed closure has reintroduced uncertainty around maritime access, with Iran now imposing stricter controls and issuing warnings to commercial vessels.

The “Desh Garima” incident has further heightened tensions. The reported interception and damage of an Iranian-linked vessel by US forces has been framed by Tehran as an act of aggression, raising concerns that isolated incidents could escalate into broader confrontation.

Meanwhile, the situation regarding the second round of US-Iran peace talks in Islamabad is currently in a state of high-stakes diplomatic whiplash. There is a direct contradiction between Washington and Tehran regarding whether these talks will even happen. The “second round” may end up being a one-sided arrival.

From Washington’s side, President Donald Trump said over the weekend that a high-level US delegation would travel to Pakistan, led by Vice President JD Vance, to advance discussions. Trump struck a cautiously optimistic tone, stating that the “concept of the deal is done,” suggesting that remaining negotiations are focused on final implementation details rather than core disagreements.

Iran, however, has pushed back forcefully against that narrative. According to the state-run Islamic Republic News Agency and national broadcaster, Tehran has not agreed to participate in a second round under current conditions. Iranian officials described the US announcement as a “media game” designed to create diplomatic pressure, rejecting the idea that talks are progressing toward a finalized agreement.

For markets, this leaves a narrow but critical window of uncertainty ahead of the April 22 ceasefire deadline. The coexistence of escalating tensions and unresolved diplomacy is keeping positioning cautious. Until one narrative clearly dominates, markets are likely to remain steady—absorbing shocks, but not yet reacting decisively.

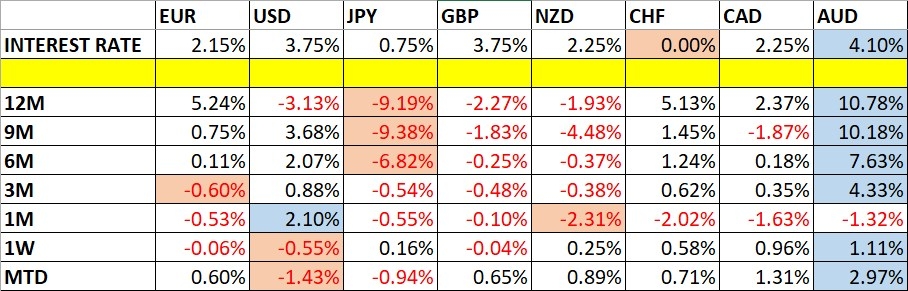

In the currency markets, for the day so far, Dollar is currently the strongest, followed by Loonie, and then Euro. Aussie is the worst, followed by Yen, and then Kiwi. Sterling and Swiss Franc are positioning in the middle.

Gold Drops as Ceasefire Cracks, But Oil Says Markets Aren’t Pricing War Yet

Gold drops as US–Iran ceasefire cracks, but oil below $100 signals markets aren’t pricing war. Fading momentum leaves gold vulnerable to a deeper move toward the 4,000 level if tension turns into conflicts. Read More.

China Holds LPR Steady for 11th Month, Signals Stability Amid Global Risks

China kept its benchmark lending rates unchanged for an 11th straight month, reinforcing a cautious stance as policymakers balance growth support against rising global risks. With the PBoC signaling a “moderately loose” policy bias but prioritizing currency stability, markets are watching how Beijing navigates geopolitical and trade tensions. Read More.

New Zealand Posts NZD 698M Trade Surplus as China, Australia Drive Export Growth

New Zealand’s trade surplus held at NZD 698M in March as exports climbed on strong demand from China and Australia, but a faster surge in imports signals rising domestic demand and cost pressures. Read More.

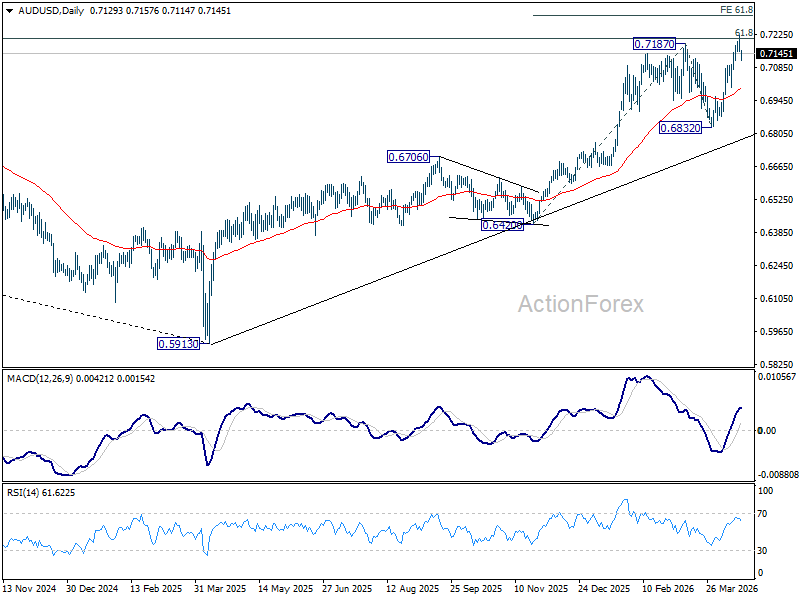

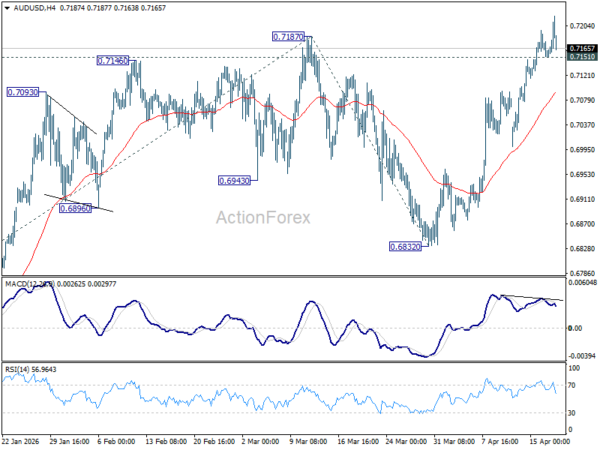

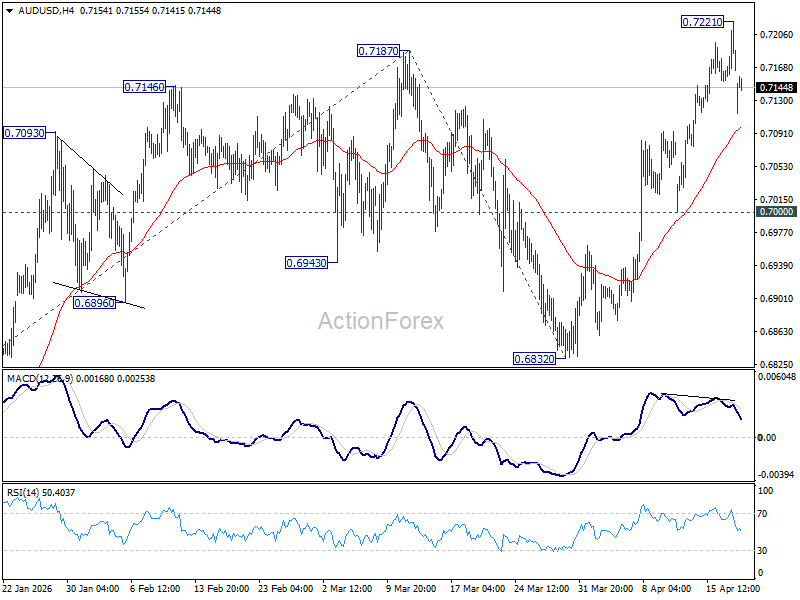

AUD/USD Daily Report

Daily Pivots: (S1) 0.7141; (P) 0.7181; (R1) 0.7209; More…

Intraday bias in AUD/USD is turned neutral again with current retreat. Some consolidations would be seen first, but downside should be contained above 0.7000 support. On the upside, above 0.7221 will extend the larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. However, break of 0.7000 will bring deeper fall back to 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.