Bloom Energy (BE +5.79%) is a clean energy company making large, box-shaped power generators that let businesses generate their own electricity instead of buying it from the grid. It essentially gives companies their own mini power plant that keeps the lights on even if the larger grid goes out.

Bloom’s technology is gaining momentum right now, and its stock over the last 12 months is proof of that. Shares of Bloom’s stock have exploded over 1,350% since last May, with a market-crushing 178% gain so far in 2026.

As of May 11, Bloom trades at about $275, about 9% below its 52-week high of $302. With strong tailwinds from artificial intelligence (AI) data center construction at its back, I think this stock is worth buying while it’s below $300. Here’s why.

Today’s Change

(5.79%) $16.79

Current Price

$306.55

Key Data Points

Market Cap

$82B

Day’s Range

$282.42 – $306.92

52wk Range

$17.01 – $306.92

Volume

134K

Avg Vol

10M

Gross Margin

31.08%

The bull case for Bloom Energy hitting $300 and beyond

Whenever the bull case for Bloom Energy is discussed, data center growth is nearly always at the center of it. And for good reason. U.S. data centers consumed about 176 terawatt-hours of electricity in 2023, a number Lawrence Berkeley National Laboratory expects to jump between 325 TWh and 580 TWh by 2028. At the high end, that would translate to roughly 400 TWh of annual electricity demand added within just five years.

That would be easier to dismiss if the grid could absorb that demand or expand at the same speed. The uncomfortable truth is that it probably can’t, at least not everywhere or as quickly as data centers are popping up.

It can take about two to three years to build a data center. But as the International Energy Agency points out, new transmission line installation can take four to eight years, while wait times for other critical components, such as transformers and cables, could also stall planned data center construction.

This is where Bloom can thrive.

Bloom can deploy one of its servers in a company’s backyard in as little as 90 days. That’s a huge time advantage when the alternative is waiting years before a finished data center can be connected to the grid. That might explain why data center companies like Equinix and Intel are currently using Bloom’s servers at their data centers, while others, such as Brookfield Corporation and Oracle, are in agreements to deploy them.

Image source: Bloom Energy.

Why the bears might be holding out

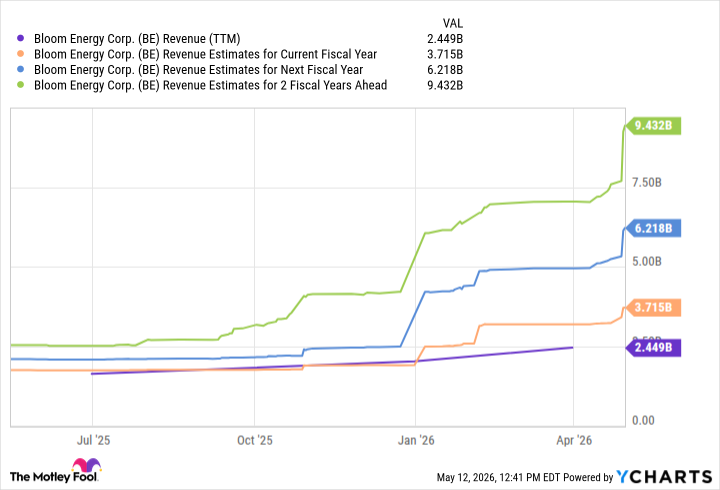

Bloom’s advantage has translated into blockbuster earnings. First-quarter revenue for 2026 grew about 130% to $751 million from last year, while full revenue guidance for 2026 is expected to be between $3.4 billion and $3.8 billion. Indeed, the next two years could be electrifying, as the chart predicts.

Data by YCharts

Bloom Energy stock, however, is trading like a software company, not one that builds power equipment. The stock is trading at 128 times forward earnings and a price-to-book ratio of 80. That kind of valuation leaves little room for ordinary bad news, let alone a real slowdown.

Still, this company clearly has an edge. For aggressive investors, a small position would make sense. For others, a clean energy exchange-traded fund (ETF) that owns Bloom may be a less risky way to invest.