Undervalued European Small Caps With Insider Action For May 2026

The European market has recently experienced modest gains, with the pan-European STOXX Europe 600 Index reflecting improved sentiment due to easing geopolitical tensions and strong corporate earnings, although concerns over potential U.S. tariffs loom. In this environment of fluctuating market dynamics, identifying small-cap stocks that are potentially undervalued can be crucial for investors seeking opportunities; these stocks often offer unique growth prospects when backed by solid fundamentals and strategic insider actions.

Top 10 Undervalued Small Caps With Insider Buying In Europe

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Value Rating: ★★★★★★

Overview: AddLife is a company engaged in providing products and services within the Labtech and Medtech sectors, with a market cap of approximately SEK 14.12 billion.

Operations: The company generates revenue primarily from its Labtech and Medtech segments, with recent figures showing SEK 3949 million and SEK 6442 million, respectively. The gross profit margin has seen fluctuations, reaching up to 38.29% in early 2026. Operating expenses are substantial, driven mainly by sales and marketing costs. Over the years, net income margins have varied significantly, reflecting changes in non-operating expenses and other financial factors.

PE: 31.3x

AddLife, a European small cap, shows potential despite its high debt levels, relying solely on external borrowing. The company reported SEK 2,645 million in sales for Q1 2026 with net income of SEK 127 million. Earnings per share rose to SEK 1.04 from SEK 0.98 last year, reflecting solid earnings quality despite large one-off items impacting results. Insider confidence is evident with recent share purchases in April 2026, suggesting optimism about future growth prospects at a forecasted rate of nearly 15% annually.

OM:ALIF B Share price vs Value as at May 2026

Simply Wall St Value Rating: ★★★★★★

Overview: Ratos is a Swedish private equity conglomerate that invests in and develops medium-sized Nordic companies, with a market cap of approximately SEK 17.91 billion.

Operations: Ratos generates revenue primarily through its sales, with recent figures showing SEK 33.98 billion in revenue for the quarter ending September 30, 2023. The company’s cost of goods sold (COGS) significantly impacts its gross profit, which was SEK 14.51 billion for the same period, resulting in a gross profit margin of 42.69%. Operating expenses include depreciation and amortization along with general and administrative costs, which together influence net income outcomes. Over time, variations are observed in both revenue and profitability metrics such as net income margin and gross profit margin.

PE: -12.7x

Ratos, a European company with potential for growth, recently reported mixed financial results. While sales for Q1 2026 slightly increased to SEK 4.5 billion from SEK 4.47 billion the previous year, net income fell to SEK 193 million from SEK 248 million. Despite these challenges, insider confidence is evident as insiders have been purchasing shares over recent months. The company’s earnings are projected to grow significantly at over 64% annually, although reliance on external borrowing poses risk concerns moving forward.

OM:RATO B Share price vs Value as at May 2026

Simply Wall St Value Rating: ★★★★☆☆

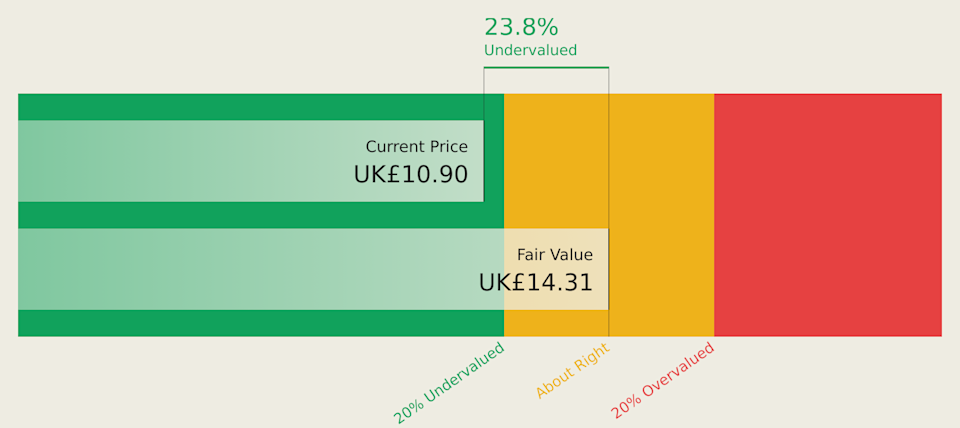

Overview: Sdiptech focuses on providing infrastructure technology solutions across sectors such as energy, water management, safety, and transportation, with a market capitalization of approximately SEK 10.92 billion.

Operations: The company’s revenue is primarily driven by its Supply Chain & Transportation segment, contributing SEK 2.06 billion, followed by Energy & Electrification at SEK 1.11 billion. Gross profit margin shows a notable trend with an increase from 11.36% in mid-2015 to 31.84% in early 2026, reflecting improvements over time in managing cost of goods sold relative to revenue growth.

PE: -92.1x

Sdiptech’s recent financial performance indicates challenges, with Q1 2026 sales and net income declining compared to last year. Despite this, insider confidence is evident as the CFO purchased 4,000 shares for approximately SEK 750,400 in early 2026. This move suggests belief in potential value despite current hurdles. The company recently repurchased bonds and redeemed preference shares to streamline finances. While earnings growth is projected at over 58% annually, reliance on external borrowing poses risks.

OM:SDIP B Share price vs Value as at May 2026

Where To Now?

Ready To Venture Into Other Investment Styles?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include OM:ALIF B OM:RATO B and OM:SDIP B.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

The United Kingdom’s stock market has experienced recent fluctuations, with the FTSE 100 index closing lower amid concerns over weak trade data from China and its impact on commodity-dependent companies. In this environment of uncertainty, identifying undervalued stocks can present opportunities for investors seeking potential value plays. Top 10 Undervalued Stocks Based On Cash Flows

Why are US stock market futures down today, and will S&P 500, Nasdaq and Dow Jones stay in red or turn green? Investors started the trading week with caution as US futures slipped after rising geopolitical risks in the Persian Gulf. Oil supply concerns and threats to shipping routes increased uncertainty. Diplomatic efforts between the

The Middle Eastern stock markets have recently experienced fluctuations, with UAE equities easing due to renewed tensions in the Gulf region. Despite these challenges, resilient local fundamentals and potential regional de-escalation could provide opportunities for investors seeking stable returns. In this context, dividend stocks can be attractive as they offer consistent income streams even amid

If the CPI significantly exceeds expectations, the market may shift from ‘the Fed pausing rate cuts this year’ to ‘the Fed possibly having to reconsider rate hikes.’ This would also mean that the dovish optimistic and bullish assumptions supporting the Risk-On environment (i.e., ‘fully embracing risk assets’) would be undermined. According to Zhitong Finance APP,

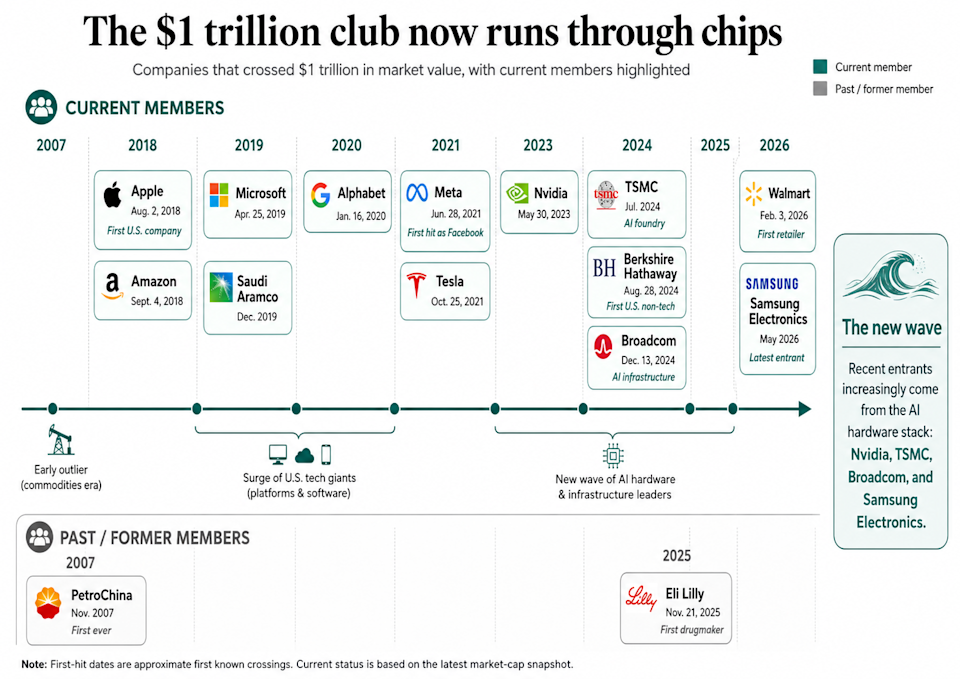

Market royalty is getting a hardware makeover. Samsung Electronics (005930.KS) just climbed past $1 trillion in market capitalization, making it the latest company tied to the AI build-out to enter the market’s most exclusive tier. It’s joining Nvidia (NVDA), TSMC (TSM), and Broadcom (AVGO) in a newer class of giants that make the chips, memory,

Semiconductor stocks leading the S&P 500 (^GSPC) and Nasdaq Composite (^IXIC) to record highs have one common thread: They sit at the bottlenecks of the artificial intelligence trade. It used to be that Nvidia (NVDA) graphics processing units (GPUs) — the primary engines of the AI boom — were hard to get. But advancements in

Hinge Health logo Key Points Interested in Hinge Health Inc.? Here are five stocks we like better. Hinge Health beat Q1 expectations with revenue of $182 million, up 47% year over year, and raised its full-year 2026 guidance. The company also posted stronger profitability, including an 85% gross margin, $46 million in non-GAAP operating income,

HA Sustainable Infrastructure Capital logo Key Points Interested in HA Sustainable Infrastructure Capital, Inc.? Here are five stocks we like better. HASI posted record first-quarter performance, with adjusted EPS of $0.77, adjusted ROE of 15.7% and adjusted recurring net investment income up 29% year over year to $101 million. Managed assets also rose 13% to

I got an early copy of Ben Carlson’s new book, “Risk & Reward.” It’s terrific. (And it goes on sale May 12!) Carlson, of Ritholtz Wealth Management, has a gift for being both entertaining and informative. His accessible writing makes for a casual read, and yet with each page you turn, you get a little

So you’re worried about a stock market crash. You’re certainly not alone. Global disturbances alone might be enough to cause worry, but check out the last few years’ performance of the S&P 500: Year S&P 500 Return 2016 12% 2017 21.8% 2018 (4.4%) 2019 31.5% 2020 18.4% 2021 28.7% 2022 (18.11%) 2023 26.29% 2024 25.02%

The S&P 500 index (SNPINDEX: ^GSPC) is trading near all-time highs despite the geopolitical conflict in the Middle East, high oil prices, and increasing concerns around a global recession. If you are like me, you probably watch all this with wonder, trying to understand why Wall Street is so positive given all of the negatives

①ICBC and Agricultural Bank of China will distribute dividends on May 13. ②The total dividend distributions for ICBC and Agricultural Bank of China in 2025 are approximately RMB 110.593 billion and RMB 87.321 billion, respectively. Cailian Press reported on May 10 that two major state-owned banks, ICBC and Agricultural Bank of China, will distribute dividends

The market has consistently reached new all-time highs over the last few months. But no bull market can last forever, and right now may be a smart time to look at the big picture. To be clear, nobody knows exactly what the market will do, especially in the near term. Even the best stock market

These past few years have been major ones for stock splits. Some of the world’s biggest companies have executed these operations after periods of explosive stock performance. The idea is to bring the price level back down to Earth, making the shares more accessible for investors — and opening the door to another era of

The S&P 500 (SNPINDEX: ^GSPC) is considered the single best gauge for the overall U.S. stock market. Tom Lee at Fundstrat Global Advisors thinks the benchmark index will reach 15,000 by 2030. That implies 103% upside from its current level of 7,386. Investors can position their portfolios to benefit by purchasing shares of an S&P

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below. President Donald Trump celebrated record stock market gains, saying strong job growth and rising retirement accounts reflected continued economic momentum. Stock Market Hits Record High On Wednesday, Trump posted on Truth Social, “Stock Market hit an ALL-TIME HIGH

Nvidia founder and CEO, Jensen Huang, speaks during the 29th annual Milken Institute Global Conference at the Beverly Hilton in Beverly Hills, California on May 4, 2026. Patrick T. Fallon | AFP | Getty Images Nvidia stepped on the gas last year, putting cash into companies up and down the AI infrastructure stack and helping

Warren Buffett is one of the greatest investors in history. He spent over 70 years publicly managing money, including 60 years at the helm of Berkshire Hathaway (NYSE: BRKA) (NYSE: BRKB). But the last three years before he retired were marked by behavior that many investors couldn’t help but notice. In each of Buffett’s last

Jerome Powell’s term as chair of the Federal Reserve’s Board of Governors ends on May 15. However, Powell plans to remain on the board for an indefinite period. Powell is eligible to do so because his term on the board of governors officially ends in early 2028. The move breaks 75 years of precedent, in

Not every stock stays down for long during market corrections. Sandisk (SNDK +16.60%) seems unstoppable at current levels. It’s up by 400% year to date and has surged by nearly 3,900% over the past year. The best part is that this growth is fueled by transformative fundamentals. Sandisk acts as a key bottleneck in the