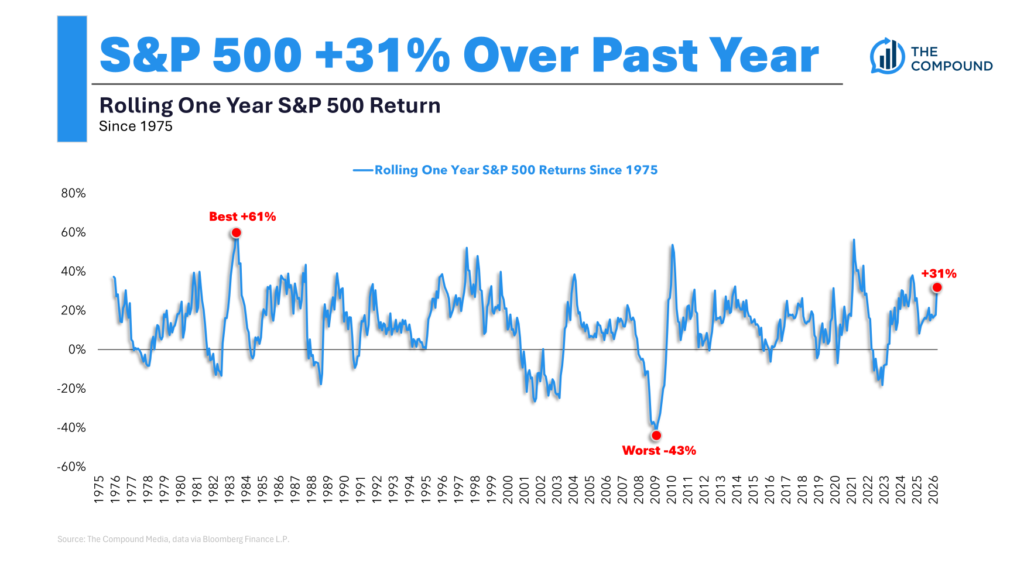

Nvidia‘s (NASDAQ: NVDA) stock has rallied more than 600% over the past two years. Most of that rally was driven by the growth of the artificial intelligence (AI) market, which boosted its sales of data center GPUs for processing complex AI tasks.

The market’s insatiable demand for its data center chips continues to outstrip its available supply, and analysts expect Nvidia’s revenue to increase at a compound annual growth rate (CAGR) of 45% from fiscal 2024 to fiscal 2027 (which ends in January 2027). They expect its earnings per share (EPS) to rise at a CAGR of 51%.

Image source: Nvidia.

So even though Nvidia is already worth more than $3 trillion, it could still have plenty of room to run. But before investors buy this high-flying stock, they should pay attention to these four red flags that could unexpectedly end its historic rally.

1. It’s become an all-in play on AI chips

Back in fiscal 2022 (which ended in January 2022), Nvidia generated 46% of its revenue from its gaming GPUs, 39% from its data center GPUs, and the rest from its professional visualization, auto, and OEM chips. However, that product mix completely changed over the following two years as its sales of data center chips eclipsed its gaming chips.

In the first quarter of fiscal 2025, Nvidia generated 87% of its revenue from data center chips, 10% from gaming chips, and the remaining 3% from its other categories. It generated $22.6 billion in data center revenue in that single quarter compared to its total revenue of nearly $27 billion for all of fiscal 2023. That breakneck expansion transformed Nvidia from a more diversified GPU maker to an all-in play on AI chips.

That’s fine if you believe Nvidia will continue dominating the AI market as it expands. But if the AI market abruptly cools off, Nvidia’s chip shortage could quickly become a supply glut. If its data center business sputters out, it can’t fall back on the growth of its gaming segment and other smaller divisions to soften those year-over-year comparisons.

2. It faces unpredictable regulatory challenges

Nvidia’s overwhelming dependence on the AI market exposes it to a lot of unpredictable regulatory challenges. U.S. regulators have repeatedly tightened their export curbs on its AI chip shipments to China, and that pressure could drive Chinese chipmakers to accelerate the development of their own AI chips.

Tighter regulations for generative AI technologies, which have already taken effect in Europe, could throttle the growth of the red-hot industry and drive companies to rein in their purchases of new AI chips. Complaints about mass plagiarism and other ethical issues could also force AI companies to expand at a slower and more measured pace.

3. It faces clear competitive threats

Nvidia controls 88% of the discrete GPU market, according to JPR, but its top rival AMD has been rolling out cheaper AI accelerators. AMD’s MI300 Instinct GPUs have already beat Nvidia’s H100 GPUs — which cost about four times more — in terms of raw processing power and memory usage across several industry benchmarks. Intel also recently claimed its new Gaudi 3 AI accelerators are faster and more power efficient than Nvidia’s H100 GPUs.

Super Micro Computer, which grew rapidly over the past few years by producing dedicated AI servers powered by Nvidia’s chips, has also been developing new servers optimized for AMD’s and Intel’s cheaper AI accelerators. These cheaper servers could attract cost-conscious data center operators and erode Nvidia’s market share.

Meanwhile, Nvidia’s tight supply and high prices are driving its top customers — including OpenAI, Microsoft, Alphabet‘s Google, and Amazon — to develop their own first-party AI accelerators. These chips won’t threaten Nvidia’s near-term growth, but they could gradually loosen its iron grip on the hyperscale data center market.

4. Its insiders are net sellers

Nvidia’s stock isn’t cheap at 49 times forward earnings and 26 times this year’s sales. But if it had the potential to double or triple again in near term, its valuations would seem reasonable and its insiders should be scooping up more shares.

Yet over the past 12 months, Nvidia’s insiders sold more than 4 times as many shares as they bought. Over the past three months, they sold more than 52 times as many shares as they bought. Those insider sales don’t necessarily mean it stock is headed off a cliff, but it’s a worrisome trend that suggests its near-term upside is limited.

Is it still safe to buy Nvidia’s stock?

I believe Nvidia is still worth buying, but investors shouldn’t assume it’s a perfect growth stock. Its transformation from a gaming company into an AI one was abrupt, and it could experience significant growing pains over the next few years. But assuming it overcomes all those competitive, regulatory, and macro challenges, it should remain one of the easiest ways to profit from the secular expansion of the AI market.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $757,001!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Leo Sun has positions in Amazon. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.