As European markets navigate a landscape marked by geopolitical tensions and economic uncertainties, the pan-European STOXX Europe 600 Index recently experienced a decline, reflecting broader market sentiment. In such an environment, identifying promising small-cap stocks requires careful consideration of factors like resilience to market volatility and potential for growth in traditionally defensive sectors.

Name

Debt To Equity

Revenue Growth

Earnings Growth

Health Rating

Dekpol

61.42%

9.03%

14.54%

★★★★★★

Lion Capital

NA

5.77%

4.53%

★★★★★★

Moury Construct

1.91%

12.60%

22.14%

★★★★★☆

Caisse Regionale de Credit Agricole Mutuel Toulouse 31

Underneath we present a selection of stocks filtered out by our screen.

Simply Wall St Value Rating: ★★★★★☆

Overview: Toyota Caetano Portugal, S.A. imports, assembles, and commercializes light and heavy vehicles with a market capitalization of €255.50 million.

Operations: The company’s primary revenue stream is from the domestic commercialization of motor vehicles, generating €821.91 million, followed by external commercialization at €41.44 million. Additional revenues come from domestic rental and services in both motor vehicles and industrial equipment sectors.

Toyota Caetano Portugal, a relatively small player in the automotive sector, has shown resilience with an earnings growth of 8.9% over the past year, outpacing the broader auto industry’s -49.4%. Despite a volatile share price recently, its debt to equity ratio increased from 22.9% to 33.2% over five years but remains satisfactory with a net debt to equity ratio of 23.1%. The company’s interest payments are well covered by EBIT at seven times coverage, suggesting financial stability amidst industry challenges and positioning it as an intriguing prospect within its market segment.

ENXTLS:SCT Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★☆☆

Overview: Embention Sistemas Inteligentes, S.A. is a drone company that develops, manufactures, and sells components and ready-to-fly autonomous vehicles for civil and military applications, with a market capitalization of €245.29 million.

Operations: Embention generates revenue primarily through the sale of drone components and autonomous vehicles for civil and military applications. The company has a market capitalization of €245.29 million, reflecting its position in the drone industry.

Embention Sistemas Inteligentes, a nimble player in the aerospace sector, has recently turned profitable, marking a significant milestone. Despite its share price volatility over the past three months, the company boasts high-quality earnings and more cash than total debt. With cash equivalents at US$2.21 million as of December 2024 and a positive change in net working capital of US$1.31 million from the previous year, Embention’s fiscal health seems robust. However, with financial reports older than six months and no clear data on free cash flow trends, future performance remains uncertain but potentially promising given its recent profitability shift.

ENXTPA:MLUAV Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Idun Industrier AB (publ) is an investment holding company that focuses on investing in and developing industrial and service businesses across Sweden, the rest of the Nordic countries, Europe, and internationally, with a market capitalization of approximately SEK3.71 billion.

Operations: Idun generates revenue primarily from its Manufacturing segment, contributing SEK1.43 billion, and its Service & Maintenance segment, adding SEK866 million.

Idun Industrier, a smaller player in the industrials sector, has been making waves with its impressive earnings growth of 74.2% over the past year, outpacing the industry average of 18.1%. Despite a high net debt to equity ratio at 98.8%, interest payments are well covered with EBIT covering them 3.4 times over. The company is trading at an attractive valuation, being priced 33.9% below its estimated fair value and boasts high-quality earnings alongside positive free cash flow trends. Recent announcements include a dividend increase to SEK 1.15 per share, reflecting confidence in ongoing financial health and future prospects.

OM:IDUN B Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENXTLS:SCT ENXTPA:MLUAV and OM:IDUN B.

📌 Top story — scroll down for more updates Top of the Morning 8:20 am By Alicia AlfiereTeam Rule Breakers Etsy (ETSY 0.75%) stock popped earlier this year on the news that it is selling its second-hand and vintage clothing business, Depop, for $1.2 billion in cash. This could be a good thing for the

Actively managed by PineBridge Investments, the VanEck CLO Opportunities Fund seeks high income and attractive total return through exposure to CLO equity and junior mezzanine debt, building on the success of VanEck’s CLO ETF suite, which includes CLOI for investment grade CLOs and CLOB for mezzanine CLOs. The Fund is an unlisted interval fund with

As global markets navigate a landscape marked by record highs in major U.S. stock indexes and robust retail sales growth, the technology sector continues to capture investor attention with its potential for innovation and expansion. In this context, identifying high-growth tech stocks with global potential involves looking at companies that not only capitalize on the

Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide. The Morning Bull – US Market Morning Update Friday, May, 1 2026 US stock futures are slightly higher this morning, as investors balance slower growth with hotter inflation. First quarter US GDP grew at

Image source: Getty Images If you’re a typical British investor considering your pension or ISA, you’ve probably heard the chatter about stock market jitters lately. Oil prices, having spiked to over $110 a barrel amid Middle East tensions, have led to significant volatility on the FTSE 100. March was particularly rough but the recent recovery

Asian stock markets tracked Wall Street higher in holiday-thinned trade (Mohd RASFAN) · Mohd RASFAN/AFP/AFP Oil prices edged up Friday after the previous day’s wild swings, with investors awaiting the next move in the Middle East crisis, while Asian stocks rose in holiday-thinned trade following a tech-led record day on Wall Street. With peace talks

The United Kingdom’s market has been experiencing some turbulence, with the FTSE 100 index recently closing lower due to weak trade data from China, highlighting global economic interdependencies. Despite these challenges, investors continue to seek opportunities within the stock market that align with both value and growth potential. Penny stocks—though an older term—still represent a

“The catalyst was about mid-2024,” says Stephanie Wilks-Wiffen from eToro, an online broker. That was when she read the annual Boring Money report. It showed that the gender investment gap had widened in the UK, with men making up almost 60% of investors. eToro then started developing its “Loud Investing” campaign, which aims to educate

FIL:E – The New York Stock Exchange is shown in New York’s Financial District on Dec. 23, 2024. Peter Morgan/AP Specialist Anthony Matesic works at his post on the floor of the New York Stock Exchange, Thursday, April 30, 2026. Richard Drew/AP A person stands in front of an electronic stock board showing Japan’s Nikkei

As geopolitical tensions in the Middle East heighten, regional stock markets have experienced a downturn, with key indices like the Qatari and Abu Dhabi benchmarks slipping amid concerns over potential U.S. military action against Iran. Despite these challenges, investors may find opportunities in undiscovered gems that demonstrate resilience through strong fundamentals and strategic positioning within

The Australian share market has recently faced a challenging period, marked by a series of declines and broader economic pressures. In such conditions, investors often look for opportunities in smaller companies that can offer both affordability and potential growth. Penny stocks, though an older term, still capture the essence of investing in emerging companies with

Today’s Change (0.76%) $1.99 Current Price $265.03 Key Data Points Market Cap $2.8T Day’s Range $256.19 – $273.89 52wk Range $183.85 – $273.89 Volume 4.1M Avg Vol 52M Gross Margin 50.29% Amazon (AMZN +0.76%), a leader in both e-commerce and cloud computing, closed Thursday at $265.06, up 0.77%. The stock moved as investors weighed a

Today’s Change (9.63%) $0.85 Current Price $9.73 Key Data Points Market Cap $6.0B Day’s Range $9.01 – $10.16 52wk Range $7.95 – $21.08 Volume 4.1M Avg Vol 34M Gross Margin 86.68% Dividend Yield 10.14% Blue Owl Capital (OWL +9.63%), an alternative asset manager and private credit firm, closed Thursday at $9.75, up 9.80%. The stock

As global markets navigate geopolitical uncertainties and economic shifts, Asia’s stock markets have shown resilience, with mainland equities maintaining stability amid strong economic data. In this context, growth companies with significant insider ownership can be particularly appealing as they often indicate confidence from those closest to the business. Top 10 Growth Companies With High Insider

Today’s Change (15.52%) $0.79 Current Price $5.88 Key Data Points Market Cap $10.0B Day’s Range $5.13 – $6.33 52wk Range $3.60 – $8.25 Volume 59M Avg Vol 18M Gross Margin -240000.00% Aurora Innovation (AUR +15.52%), a developer of self-driving technology for various vehicle types and applications, closed Thursday at $5.88, up 15.52%. The stock moved

Today’s Change (-8.49%) $-56.81 Current Price $612.31 Key Data Points Market Cap $1.7T Day’s Range $600.00 – $620.62 52wk Range $520.26 – $796.25 Volume 3M Avg Vol 15M Gross Margin 82.00% Dividend Yield 0.31% Meta Platforms (META 8.49%), a social media and virtual reality company, closed Thursday at $611.91, down 8.55%. Shares dropped after Q1

From some perspectives, Tesla (TSLA +2.45%) looks outrageously expensive. For example, its shares trade at nearly 14 times sales. For comparison, Rivian, another popular electric vehicle (EV) stock, trades below 4 times sales. To be clear, I’m a big fan of Rivian. I think shares are ridiculously cheap with 1,000% upside potential. But I also

As the Australian share market experiences a downturn with a potential -0.7% drop, investors are navigating challenging conditions marked by global economic pressures and fluctuating commodity prices. In such an environment, dividend stocks can offer stability and potential income, making them an attractive option for those seeking to balance risk while capitalizing on consistent returns.

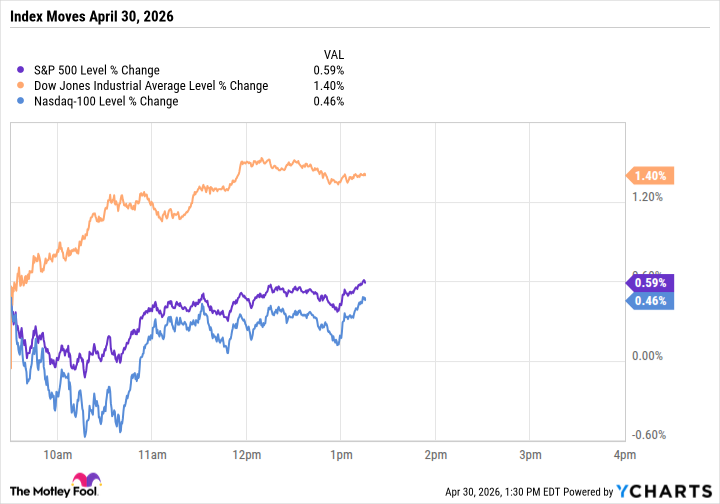

The three major U.S. stock indexes moved higher by midday Thursday, though the gains were uneven. The themes of the day were earnings reports, oil prices, and artificial intelligence (AI). As usual, right? The Dow Jones Industrial Average (^DJI +1.77%) led with a 1.3% advance as of 1:08 p.m. ET, buoyed by a double-digit surge

📌 Top story — scroll down for more updates Today’s Lunchtime News 1:10 pm — NVDA -4.1% Nvidia (NVDA 4.17%) shares fell more than 4% as investors weighed mounting competitive pressure from hyperscalers building and selling their own AI chips, even as other chipmakers climbed. Hyperscaler encroachment: On its earnings call Wednesday, Amazon (AMZN 0.44%)