Discover 3 Asian Growth Companies With Insider Ownership Up To 23%

As global markets navigate geopolitical uncertainties and economic shifts, Asia’s stock markets have shown resilience, with mainland equities maintaining stability amid strong economic data. In this context, growth companies with significant insider ownership can be particularly appealing as they often indicate confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Asia

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Growth Rating: ★★★★★★

Overview: Akeso, Inc. is a biopharmaceutical company focused on the research, development, manufacture, and commercialization of antibody drugs globally with a market cap of HK$125.09 billion.

Operations: The company’s revenue primarily comes from the research, development, production, and sale of biopharmaceutical products, amounting to CN¥3.06 billion.

Insider Ownership: 18.1%

Akeso is poised for growth with a strong pipeline of innovative bispecific antibodies, including ivonescimab and cadonilimab, which have shown promising clinical results. The company is trading at 25.2% below estimated fair value and is expected to achieve profitability within three years. Revenue growth forecasts at 29.1% annually surpass market averages, supported by significant advancements in oncology treatments like the recent upgrades for ivonescimab in NSCLC guidelines.

SEHK:9926 Ownership Breakdown as at Apr 2026

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Daimay Automotive Interior Co., Ltd specializes in the research, development, and sale of passenger car components both in China and internationally, with a market cap of CN¥23.51 billion.

Operations: Shanghai Daimay Automotive Interior Co., Ltd generates revenue through the development and sale of passenger car components across domestic and international markets.

Insider Ownership: 23.3%

Shanghai Daimay Automotive Interior is positioned for growth, with earnings projected to rise 29.41% annually, outpacing the Chinese market’s 26.9%. Despite trading at 30.8% below its fair value estimate, recent quarterly results showed a decline in both sales (CNY 1,539.31 million) and net income (CNY 186.43 million) compared to last year. The dividend yield of 2.46% lacks earnings coverage, yet revenue growth remains robust at an annual rate of 16%.

SHSE:603730 Ownership Breakdown as at Apr 2026

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zhuzhou Huarui Precision Cutting Tools Co., Ltd. operates in the manufacturing sector, specializing in precision cutting tools, with a market cap of CN¥14.22 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 20.1%

Zhuzhou Huarui Precision Cutting Tools Ltd. demonstrates significant growth potential, with revenue forecasted to increase by 22.6% annually, surpassing the Chinese market’s average. Recent earnings showed substantial improvement, with Q1 net income rising to CNY 175.19 million from CNY 29.22 million a year earlier. Despite high share price volatility and an unstable dividend history, its price-to-earnings ratio of 42.7x is below the market average, indicating relative value in its sector.

SHSE:688059 Earnings and Revenue Growth as at Apr 2026

Key Takeaways

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:9926 SHSE:603730 and SHSE:688059.

The Australian share market has recently faced a challenging period, marked by a series of declines and broader economic pressures. In such conditions, investors often look for opportunities in smaller companies that can offer both affordability and potential growth. Penny stocks, though an older term, still capture the essence of investing in emerging companies with

Today’s Change (0.76%) $1.99 Current Price $265.03 Key Data Points Market Cap $2.8T Day’s Range $256.19 – $273.89 52wk Range $183.85 – $273.89 Volume 4.1M Avg Vol 52M Gross Margin 50.29% Amazon (AMZN +0.76%), a leader in both e-commerce and cloud computing, closed Thursday at $265.06, up 0.77%. The stock moved as investors weighed a

Today’s Change (9.63%) $0.85 Current Price $9.73 Key Data Points Market Cap $6.0B Day’s Range $9.01 – $10.16 52wk Range $7.95 – $21.08 Volume 4.1M Avg Vol 34M Gross Margin 86.68% Dividend Yield 10.14% Blue Owl Capital (OWL +9.63%), an alternative asset manager and private credit firm, closed Thursday at $9.75, up 9.80%. The stock

Today’s Change (15.52%) $0.79 Current Price $5.88 Key Data Points Market Cap $10.0B Day’s Range $5.13 – $6.33 52wk Range $3.60 – $8.25 Volume 59M Avg Vol 18M Gross Margin -240000.00% Aurora Innovation (AUR +15.52%), a developer of self-driving technology for various vehicle types and applications, closed Thursday at $5.88, up 15.52%. The stock moved

Today’s Change (-8.49%) $-56.81 Current Price $612.31 Key Data Points Market Cap $1.7T Day’s Range $600.00 – $620.62 52wk Range $520.26 – $796.25 Volume 3M Avg Vol 15M Gross Margin 82.00% Dividend Yield 0.31% Meta Platforms (META 8.49%), a social media and virtual reality company, closed Thursday at $611.91, down 8.55%. Shares dropped after Q1

From some perspectives, Tesla (TSLA +2.45%) looks outrageously expensive. For example, its shares trade at nearly 14 times sales. For comparison, Rivian, another popular electric vehicle (EV) stock, trades below 4 times sales. To be clear, I’m a big fan of Rivian. I think shares are ridiculously cheap with 1,000% upside potential. But I also

As the Australian share market experiences a downturn with a potential -0.7% drop, investors are navigating challenging conditions marked by global economic pressures and fluctuating commodity prices. In such an environment, dividend stocks can offer stability and potential income, making them an attractive option for those seeking to balance risk while capitalizing on consistent returns.

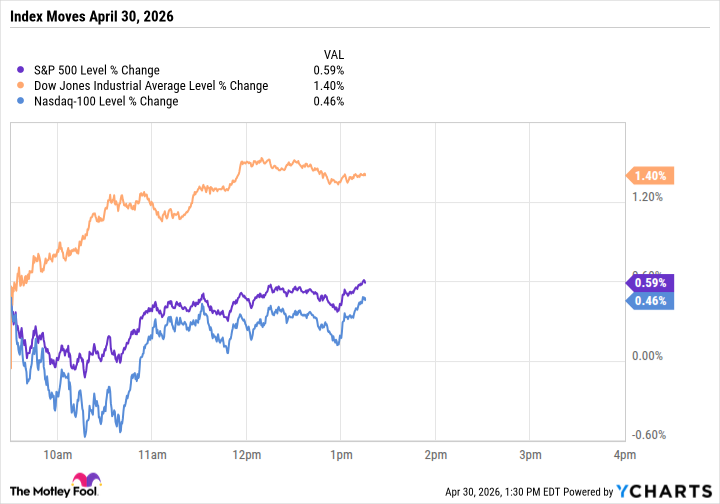

The three major U.S. stock indexes moved higher by midday Thursday, though the gains were uneven. The themes of the day were earnings reports, oil prices, and artificial intelligence (AI). As usual, right? The Dow Jones Industrial Average (^DJI +1.77%) led with a 1.3% advance as of 1:08 p.m. ET, buoyed by a double-digit surge

📌 Top story — scroll down for more updates Today’s Lunchtime News 1:10 pm — NVDA -4.1% Nvidia (NVDA 4.17%) shares fell more than 4% as investors weighed mounting competitive pressure from hyperscalers building and selling their own AI chips, even as other chipmakers climbed. Hyperscaler encroachment: On its earnings call Wednesday, Amazon (AMZN 0.44%)

Elior Manier Market Analyst Elior brings over seven years of experience in financial markets to our analyst team. Since 2018, he has actively engaged in observing, charting, and trading, driven by his passion for mastering market dynamics. With a profound understanding of the geopolitical and macroeconomic forces that shape market movements, Elior focuses on analysing

Mark Zuckerberg, CEO of Meta Platforms. David Paul Morris | Bloomberg | Getty Images Alphabet‘s stock surged more than 5% on Thursday, while Meta shares plunged 10%, as investors digested Wednesday’s first-quarter earnings results, which included plans to up the ante on artificial intelligence spending. It is pacing to be Meta’s worst day since October

Gas prices are well above $4, ceasefire negotiations are on ice and airlines are warning that they’re running out of jet fuel. So, it sure seems odd that stocks are at record highs. Blame CNN. No, really. Not for world events or the machinations of the markets, but for the perception that those two things

There’s one thing for sure about the stock market: It will always be volatile. Always has been, always will be — it’s part of its DNA. Unfortunately, part of that volatility involves stock prices dropping, but it doesn’t always have to be a bad thing. Market dips can be a great time to buy good

U.S. tech stocks have had a long run of success. In the past five years, the tech-heavy Nasdaq-100 index has gained 97%, outperforming the S&P 500 (SNPINDEX: ^GSPC), which is up 72%. What if you could do even better than that 97% gain? The ProShares UltraPro QQQ (NASDAQ: TQQQ) offers investors a unique way to

Intercontinental Exchange (NYSE: ICE), one of the world’s leading providers of financial market technology and data powering global capital markets, announced today a $0.52 per share dividend for the second quarter of 2026, which is up 8% from the $0.48 per share dividend paid in the second quarter of 2025. The cash dividend is payable

Most investors see Brookfield Corporation (BN 2.40%) as an asset manager. That’s not wrong, but it misses what the business is becoming. Brookfield Corporation isn’t just managing capital anymore. It’s building a system that can generate, control, and reinvest capital within its own ecosystem — a model that increasingly resembles how Berkshire Hathaway compounds wealth

A lot has happened since the beginning of April. The US sent a spacecraft around the moon and back. They had Coachella (twice) and also Stagecoach. Spirit Airlines was pushed to the brink of bankruptcy, and now the US government wants to bail it out. Life comes at you fast. Loading audio narration… When you

As the UK market grapples with the impact of weak trade data from China, reflected in the recent dip of the FTSE 100 and FTSE 250 indices, investors are increasingly seeking stability amid global economic uncertainties. In such an environment, dividend stocks can offer a reliable income stream, providing a buffer against market volatility while

OSB GROUP PLC LEI: 213800ZBKL9BHSL2K459 Published: 30.04.2026 OSB GROUP PLCTrading update for the first quarter to 31 March 2026 OSB GROUP PLC (the Group), the specialist lending and retail savings group, today issues its trading update for the period from 1 January 2026 to date. The Group delivered a resilient financial performance combined with strategic