Undiscovered Gems In The UK Three Small Caps With Promising Potential

The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China, highlighting global economic uncertainties. In this environment, small-cap stocks can offer unique opportunities for investors seeking growth potential, as these companies are often less exposed to international fluctuations and may benefit from domestic market dynamics.

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★★★

Overview: Supreme Plc is a company that owns, manufactures, and distributes fast-moving branded and discounted consumer goods across the UK, Ireland, the Netherlands, France, other parts of Europe, and internationally with a market cap of £193.57 million.

Operations: Revenue is primarily driven by the Vaping segment, contributing £137.57 million, followed by Drinks & Wellness at £65.16 million.

Supreme, a nimble player in the UK market, showcases a mixed performance with recent developments. Despite a negative earnings growth of 8.6% last year, it stands out by being debt-free compared to five years ago when its debt-to-equity ratio was 174.1%. The company’s free cash flow is robust, reaching £21.63 million as of March 2024. Supreme’s recent exclusive licensing agreement with Carabao for manufacturing and distributing energy drinks across the UK hints at promising prospects, aiming for significant revenue growth of approximately £265 million in FY26 from £231.1 million in FY25.

AIM:SUP Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★★★

Overview: ME Group International plc operates automated instant-service equipment in the United Kingdom and has a market capitalization of £578.17 million.

Operations: The company’s primary revenue stream is from its Personal Services segment, generating £315.39 million.

ME Group International, a nimble player in the UK market, is making waves with its strategic pivot towards self-service laundry and automated solutions. Over the past five years, earnings have surged by 24.8% annually, indicating robust growth despite a recent 4.6% increase that lagged behind industry averages. The company’s debt-to-equity ratio has impressively shrunk from 74.5% to 14.1%, showcasing financial prudence while maintaining more cash than total debt—an encouraging sign of stability. With plans to install over 1,300 Wash.ME machines in partnership with ASDA this fiscal year and a share repurchase program worth £18 million underway, ME Group seems poised for continued expansion and value creation amidst evolving market dynamics.

LSE:MEGP Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★☆☆

Overview: Metro Bank Holdings PLC is a bank holding company for Metro Bank PLC, offering business, commercial, retail, and private banking products and services in the United Kingdom with a market capitalization of approximately £968.30 million.

Operations: Metro Bank Holdings PLC generates revenue primarily from its banking segment, amounting to £574 million.

Metro Bank Holdings, with total assets of £16.5 billion and equity of £1.5 billion, stands out for its relationship-driven approach and substantial low-risk funding, as 92% of liabilities are customer deposits. Despite a high bad loans ratio at 5.1%, the bank’s earnings grew by 23% last year, surpassing industry averages. Total deposits sit at £13.8 billion against loans of £8.8 billion, though the allowance for bad loans remains low at 37%. Metro Bank is focusing on digital upgrades and expanding in urban areas to enhance operational efficiency amidst rising competition from digital banks.

LSE:MTRO Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:SUP LSE:MEGP and LSE:MTRO.

Making history is nothing unusual for Wall Street’s benchmark indexes. As of the closing bell on April 17, the S&P 500 (SNPINDEX: ^GSPC) and Nasdaq Composite (NASDAQINDEX: ^IXIC) were both at record highs, while the Dow Jones Industrial Average (DJINDICES: ^DJI) was one solid day away from joining its peers. The Nasdaq was also on

PRESS RELEASE Share Buyback Transaction Details April 16 – April 22, 2026 Alphen aan den Rijn – April 23, 2026 – Wolters Kluwer (Euronext: WKL), a global leader in professional information solutions, software and services, today reports that it has repurchased 95,594 of its own ordinary shares in the period from April 16, 2026, up to

Despite inflows, RIAs account for just 0.38% of overseas holdings Traders at KB Securities in Seoul monitor the market on April 23, after the Kospi broke through 6,500 points, following a tech-led surge from Wall Street and stellar performance by SK hynix. (The Korea Herald) South Korea’s record-setting Kospi rally is driving a surge in

The Middle Eastern stock markets have recently faced challenges, with Gulf indices experiencing declines due to geopolitical tensions and the closure of the Strait of Hormuz. Despite these headwinds, certain investment opportunities remain attractive, particularly in the realm of penny stocks. Although often considered a term from past market eras, penny stocks continue to offer

Micron (NASDAQ: MU) stock is roaring higher in Wednesday’s trading. The artificial intelligence (AI) memory-chip leader’s share price was up 7.7% as of 1:15 p.m. ET. Meanwhile, the S&P 500 was up 0.6%, and the Nasdaq Composite had risen 1.2%. The stock market is rallying on news that the U.S. and Iran have agreed to

Kazuhiro Nogi | AFP | Getty Images Japan and South Korea stocks hit record highs Thursday, trailing overnight gains on Wall Street after President Donald Trump‘s extended a ceasefire with Iran, boosting investor sentiment alongside strong corporate earnings. Trump extended a two-week U.S. ceasefire on Tuesday, saying it was warranted due to Tehran’s “seriously fractured” government.

Up about 21% in 2026 as of this writing, Interactive Brokers (IBKR 2.04%) has been crushing the market this year. But this strong performance raised the stakes going into the company’s earnings report this week. For the most part, however, the broker delivered. While revenue came in just shy of analysts’ expectations, it was arguably

Palantir (NASDAQ: PLTR) has a reputation for being an overvalued stock. It came by that reputation honestly, as it truly was one of the most expensive stocks on the market by the standard valuation metrics for a while. However, with the stock now down by around 30% from its all-time high, is it still overvalued,

One Wall Street strategist puts the probability of a market “meltdown” at 35% amid the current convergence of tariff pressures and the Iran conflict. Goldman Sachs has warned of a stagflation-like effect in the short term as oil-driven inflation rises even as growth slows, per Yahoo Finance’s April 2026 reporting. J.P. Morgan now expects the

CNBC’s Jim Cramer on Wednesday offered investors a mental framework to make buying high-flying stocks easier to stomach. “In a hot market … you needed to have the discipline to pay up for great stocks to avoid missing out,’” the “Mad Money” host said. Cramer described a lesson from earlier in his career, when a

Costco Wholesale stock surged out of the gate in 2026, with the shares currently up about 17% year to date. It has benefited from investors’ desire for more defensive consumer goods stocks amid caution around heavy technology spending and the broader economy. But the downside to buying Costco stock right now is its high valuation,

Partnership will support NZX’s highly anticipated launch of S&P/NZX 20 Index Futures contract CHICAGO, April 22, 2026 /PRNewswire/ — Trading Technologies International, Inc. (TT), a global capital markets technology platform services provider, announced that it has partnered with NZX, the company operating New Zealand’s equity, debt, funds, derivatives and energy markets, to deliver native connectivity

Real-time Estimate Cboe BZX 03:27:30 2026-04-22 pm EDT 5-day change 1st Jan Change 334.52 USD -0.03% +1.71% +3.22% Published on 04/22/2026 at 03:05 pm EDT S&P Capital IQ The Sherwin-Williams Company announced a regular quarterly dividend of $0.80 per common share, payable on June 5, 2026, to shareholders of record on May 22, 2026. 03:05pm

NEW YORK, April 22, 2026 (GLOBE NEWSWIRE) — BitsStrategy has launched a new free AI stock trading bot designed to help users identify market opportunities with greater precision and participate in stock trading through a simpler, more structured workflow. Built for users who want smarter support in fast-moving equity markets, the new release reflects growing

At first glance, Enbridge (NYSE: ENB), Procter & Gamble (NYSE: PG), and International Business Machines (NYSE: IBM) have very little in common. That’s the point. Diversification is important when you build a dividend portfolio. But so is owning good companies. Here’s why I have no plans to sell these stocks for the next 20, or

In the past decade, the S&P 500 index (SNPINDEX: ^GSPC) registered a total return of 303% (as of April 17). On an annualized basis, the 15% gain is significantly higher than the market’s long-run historical average. With a stellar performance like this, it might encourage anyone to seriously consider putting money to work. But first,

Elior Manier Market Analyst Elior brings over seven years of experience in financial markets to our analyst team. Since 2018, he has actively engaged in observing, charting, and trading, driven by his passion for mastering market dynamics. With a profound understanding of the geopolitical and macroeconomic forces that shape market movements, Elior focuses on analysing

After three years of high growth, the stock of SoFi Technologies (SOFI +2.26%) has dropped like a rock this year. It’s off 47% from its November high, and a recent short-seller’s report hasn’t helped the situation. A low price could create an opportunity, or it could also be a value trap. Here’s why I think

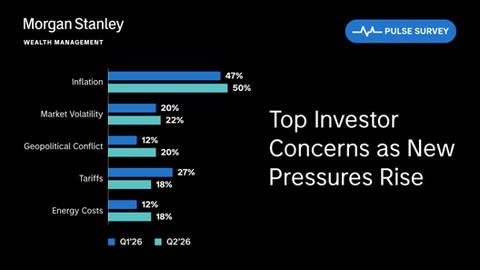

As uncertainty rises, investors keep a close watch on their portfolios NEW YORK, April 22, 2026–(BUSINESS WIRE)–Morgan Stanley Wealth Management today announced the results of its quarterly retail investor pulse survey: Bullish sentiment holds. More than half of investors (55%) remain bullish this quarter, only slightly below last quarter (56%). Inflation remains the top concern