As European markets navigate the complexities of Middle East tensions and energy market volatility, the pan-European STOXX Europe 600 Index has shown resilience, ending the week with a 3.92% gain. Amidst these broader market dynamics, small-cap stocks in Europe present intriguing opportunities for investors seeking value, particularly when insider activity suggests confidence in a company’s prospects.

|

Name |

PE |

PS |

Discount to Fair Value |

Value Rating |

|---|---|---|---|---|

|

CellaVision |

23.5x |

4.7x |

43.79% |

★★★★★★ |

|

Eurocell |

11.2x |

0.3x |

47.98% |

★★★★★☆ |

|

Morgan Advanced Materials |

NA |

0.6x |

44.47% |

★★★★★☆ |

|

Bilia |

15.0x |

0.3x |

25.20% |

★★★★★☆ |

|

Lemonsoft Oyj |

19.0x |

2.9x |

44.05% |

★★★★★☆ |

|

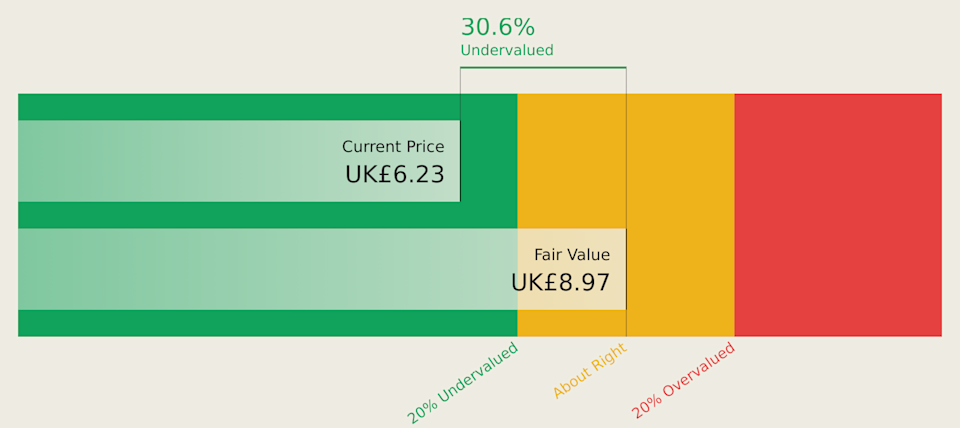

everplay group |

12.4x |

2.0x |

13.02% |

★★★★★☆ |

|

Embracer Group |

2.7x |

0.6x |

37.56% |

★★★★★☆ |

|

THG |

NA |

0.3x |

22.29% |

★★★★★☆ |

|

Eastnine |

9.7x |

6.6x |

18.63% |

★★★☆☆☆ |

|

ABL Group |

NA |

0.4x |

-44.52% |

★★★☆☆☆ |

Let’s uncover some gems from our specialized screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: Everplay Group is a company that develops and publishes games and apps, with a market cap of £1.25 billion.

Operations: The group generates revenue primarily from developing and publishing games and apps, with a reported revenue of £165.995 million in the latest period. The cost of goods sold (COGS) stands at £89.932 million, leading to a gross profit of £76.063 million and a gross profit margin of 45.82%. Operating expenses are significant, including general and administrative expenses amounting to £41.561 million, impacting the company’s net income margin which is 16.41%.

PE: 12.4x

Everplay Group, a European company with potential for growth, is seeing insider confidence as Frank Sagnier purchased 33,200 shares valued at £99,932. Their earnings are set to grow by 5.5% annually despite higher risk funding from external borrowing. Recent results show stable sales at £166 million and a rise in net income to £27.24 million for 2025. The dividend proposal of 2.9p per share reflects steady shareholder returns amid market challenges, pending approval in June 2026.

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Norbit is a company engaged in providing technology solutions across its Oceans, Connectivity, and Product Innovation and Realization segments, with a market capitalization of NOK 3.65 billion.

Operations: The company generates revenue from three primary segments: Oceans, Connectivity, and Product Innovation and Realization (PIR). Gross profit margin has shown an upward trend, reaching 61.99% in the first quarter of 2025 before a slight decrease to 55.64% by year-end. Operating expenses are primarily driven by general and administrative costs, which amounted to NOK 498.8 million at the end of 2025.