As global markets navigate a complex landscape marked by geopolitical tensions and shifting central bank policies, Asian equities present intriguing opportunities for investors seeking growth beyond the familiar large-cap stocks. In this dynamic environment, identifying promising small-cap companies with robust fundamentals and strategic positioning can offer unique advantages, especially as these firms often remain under the radar despite their potential to thrive amid broader market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Triocean Industrial Corporation | 37.55% | 44.05% | 72.36% | ★★★★★★ |

| Jiangsu JIXIN Wind Energy Technology | 10.91% | -9.44% | -19.27% | ★★★★★★ |

| Xi’an High Voltage Apparatus Research Institute | 1.24% | 12.83% | 20.14% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.42% | 17.83% | 29.70% | ★★★★★☆ |

| Xiamen King Long Motor Group | 96.48% | 11.56% | 52.73% | ★★★★★☆ |

| Zhongyeda Electric | 0.55% | -2.85% | -18.84% | ★★★★★☆ |

| Shanghai Fortune Techgroup | 18.02% | 11.69% | -6.00% | ★★★★★☆ |

| Jiangsu ChengXing Phosph-Chemicals | 58.58% | -0.89% | 3.69% | ★★★★★☆ |

| Wholetech System Hitech | 3.94% | 12.11% | 17.56% | ★★★★☆☆ |

| Shanghai New Power Automotive Technology | 0.12% | -38.61% | -6.02% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Simply Wall St Value Rating: ★★★★★★

Overview: Shijiazhuang Kelin Electric Co., Ltd. is engaged in the electrical machinery and equipment manufacturing industry both in China and internationally, with a market cap of CN¥8.75 billion.

Operations: Kelin Electric generates revenue primarily from the manufacturing and sale of electrical machinery and equipment. The company has a market capitalization of CN¥8.75 billion, reflecting its significant presence in both domestic and international markets.

Kelin Electric, a nimble player in the electrical industry, showcases impressive earnings growth of 45.1% over the past year, outpacing the sector’s 2.6%. The company trades at a discount of 19.1% below its estimated fair value and has reduced its debt-to-equity ratio from 26.2% to 21.8% over five years, indicating prudent financial management. Despite recent first-quarter results showing sales at CNY 866 million and net income down to CNY 42 million from CNY 73 million last year, Kelin remains profitable with robust cash flow and well-covered interest payments by EBIT (24.9x).

Simply Wall St Value Rating: ★★★★★☆

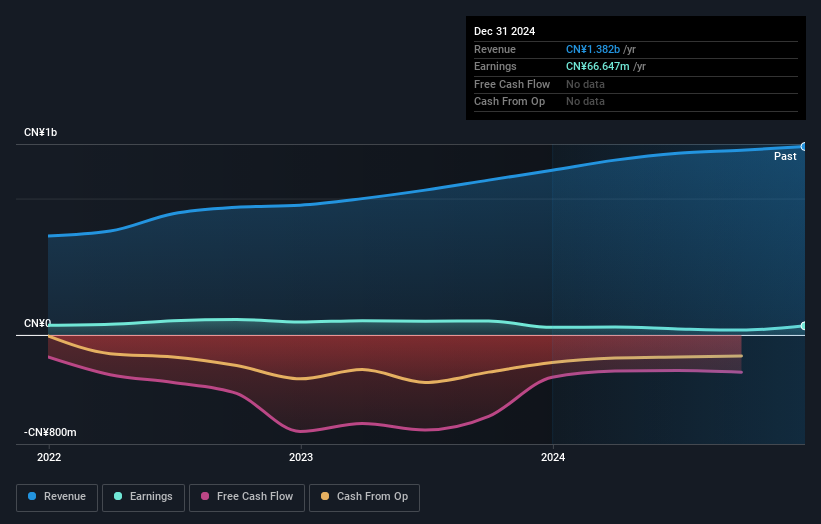

Overview: Jiangsu Longda Superalloy Co., Ltd. focuses on the research, development, production, and sale of alloy and superalloy materials both in China and internationally, with a market cap of CN¥9.25 billion.

Operations: Jiangsu Longda Superalloy generates revenue primarily from the sale of alloy and superalloy materials. The company’s net profit margin trends provide insights into its profitability.

Jiangsu Longda Superalloy, a small player in the metals and mining sector, has shown impressive earnings growth of 38.9% over the past year, outpacing industry averages. Despite a volatile share price recently, its net income rose to CNY 47.57 million in Q1 2026 from CNY 28.54 million a year ago, reflecting strong operational performance. The company has successfully reduced its debt to equity ratio from 53.6% to 26% over five years and maintains more cash than total debt, indicating sound financial management. However, free cash flow remains negative at -CNY 273 million as of September 2025 due to significant capital expenditures likely impacting liquidity dynamics.

Simply Wall St Value Rating: ★★★★★★

Overview: DeHua TB New Decoration Material Co., Ltd specializes in the production and sale of environmentally friendly furniture panels both in China and internationally, with a market capitalization of CN¥12.15 billion.

Operations: The company generates revenue primarily from the production and sale of environmentally friendly furniture panels. It has a market capitalization of CN¥12.15 billion.

DeHua TB New Decoration Material Co., Ltd, with its modest market size, has shown impressive financial resilience. The company reported a net income of CNY 148.03 million for Q1 2026, up from CNY 101.14 million the previous year, reflecting robust growth in earnings per share from CNY 0.12 to CNY 0.18. Over the past five years, its debt to equity ratio significantly decreased from 54.9% to just 0.5%, highlighting effective debt management strategies and positioning it well within industry standards as it trades at a value below its estimated fair value by about 23%.

Make It Happen

Looking For Alternative Opportunities?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com