Taiwan Semiconductor is my favorite investment pick right now.

One area where there is a ton of cash being spent is the artificial intelligence sector. AI hyperscalers seem to be tripping over themselves to spend as much money as possible to build out their computing capacity. Several companies are benefiting from this massive spending spree. One of my favorites is Taiwan Semiconductor Manufacaturing Co. (TSM +0.51%), which provides many of the chips used in AI computing units.

I think TSMC is one of the best investment options now, and its stock could be slated to triple in the next five years if the AI buildout projections come to fruition.

Image source: Getty Images.

Taiwan Semiconductor may be the most important company on Earth

If I were to ask you what the most important company on Earth is, you might answer with one of the tech giants, like Nvidia (NVDA 0.56%) or Apple (AAPL 0.75%). While these are reasonable answers, keep in mind that these businesses only design the product; they don’t manufacture it. Both companies outsource their chip production to Taiwan Semiconductor, and the technology these two produce wouldn’t be possible without the impressive capabilities TSMC has developed.

In the high-end chip world, there are really only two other foundry options: Samsung and Intel. Intel is struggling to find clients for its foundry division due to its poor long-term performance, and Samsung often competes against its clients in non-foundry businesses, making it a less popular option. That leaves Taiwan Semiconductor in a class of its own, and that is the reason why it’s the largest semiconductor manufacturer by revenue.

Taiwan Semiconductor Manufacturing

Today’s Change

(0.51%) $1.49

Current Price

$294.42

Key Data Points

Market Cap

$1528B

Day’s Range

$293.25 – $300.77

52wk Range

$134.25 – $311.37

Volume

437K

Avg Vol

13M

Gross Margin

57.75%

Dividend Yield

0.98%

Taiwan Semiconductor supplies most of the world’s high-end chips, and with massive amounts of money being spent on AI data centers, it’s slated to benefit from the buildout. Nvidia believes that annual global data center capital expenditure will rise to $3 trillion to $4 trillion by 2030 — a quintupling at the low end from 2025’s expected value of $600 billion. AMD (AMD +0.89%), one of Nvidia’s chief rivals, believes its data center division can grow at a 60% compound annual growth rate (CAGR) through 2030. A 60% CAGR over five years indicates nearly 10x growth, which is nearly unbelievable.

But if both companies are correct about a huge jump in AI spending, a lot more chips will be needed. And that will put Taiwan Semiconductor in an excellent position to thrive. It could easily triple over the next five years as this spending occurs. It’s risen about 260% over the past three years, more than tripling.

Taiwan Semiconductor is increasing production capacity

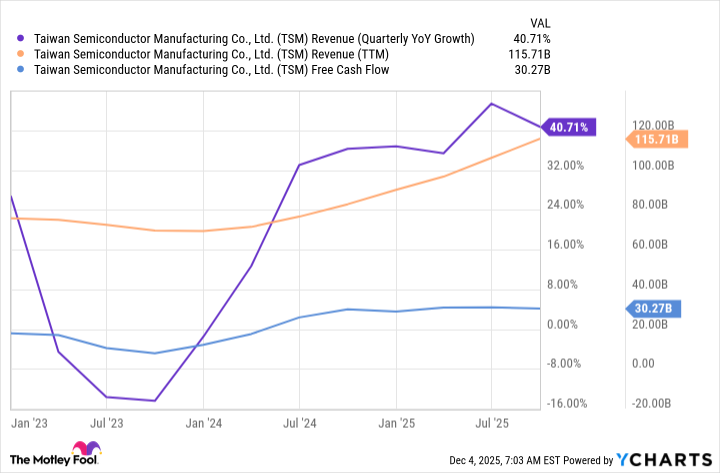

Although Taiwan Semiconductor’s revenue has risen as the AI arms race has intensified, its free cash flow has remained fairly steady recently, though it’s up 70% over the past three years.

TSM Revenue (Quarterly YoY Growth) data by YCharts

That’s because Taiwan Semiconductor has had to increase its production capacities, including investing $160 billion in U.S.-based production facilities. These investments are already paying off big time for Taiwan Semiconductor, as they allow it to sidestep import tariffs by bringing manufacturing to U.S. soil.

Once Taiwan Semiconductor’s U.S. facilities are up and running and don’t require massive cash investments, Taiwan Semiconductor’s free cash flow should explode higher, allowing it to boost share buybacks or pay a dividend. Though it might choose to continue to reinvest in itself by increasing production capacity — a decision that has already had a great return on investment.

If the AI buildout occurs at the pace that many companies in the know think it will, then Taiwan Semiconductor is a no-brainer buy. I think the stock could easily triple over the next three years, but if the AI market reaches Nvidia’s projected levels, the returns could be even greater.

Keithen Drury has positions in Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Intel, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.