The People’s Bank of China left its benchmark lending rates unchanged, keeping the 1-year Loan Prime Rate at 3.00% and the 5-year LPR at 3.50%. The decision marks the tenth consecutive month of steady policy.

For now, policymakers are seen favoring targeted structural tools—supporting sectors such as technology and green energy—rather than deploying broad-based rate cuts. Holding benchmark rates also helps anchor the Yuan, which has been hovering near a 34-month high, buoyed in part by broad Dollar weakness.

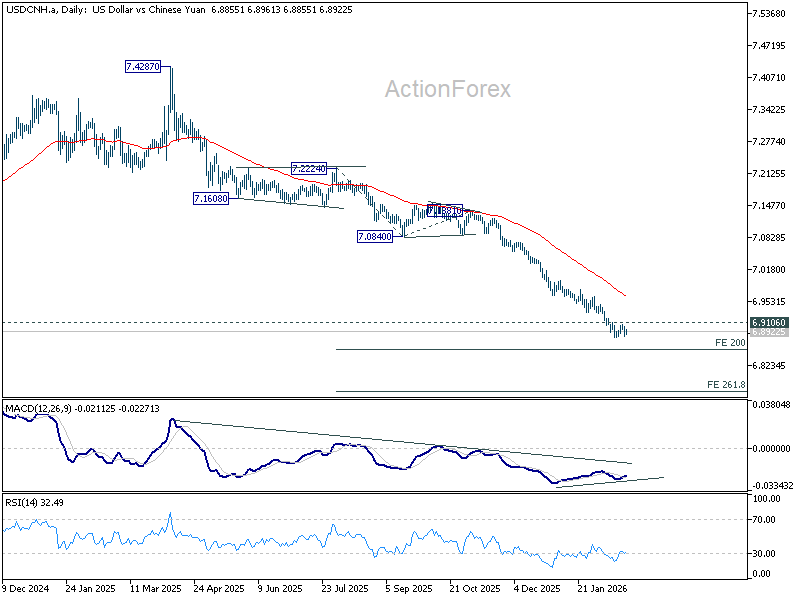

USD/CNH has been trending lower since early 2025, reflecting persistent Dollar softness. However, technically, downside momentum appears to be fading, with bullish convergence emerging on D MACD. That suggests selling pressure may be losing traction in the near term.

Support may emerge near 200% projection of 7.2224 to 7.0840 from 7.1381 at 6.8613 to bring rebound. Firm break above 6.9105 resistance would indicate short-term bottoming and open the way toward the 55 D EMA (now at 6.9629).

Still, renewed broad-based Dollar weakness could quickly push the pair through 6.8613 toward 261.8% projection at 6.7758, and possibly revive medium term downside momentum along the way.