- Tariffs off. A new twist in the global trade war story saw most of President Trump’s tariffs deemed illegal by a US trade court, ordering levies to be stopped within 10 days. This would reduce the effective US tariff rate to below 6% from a high of almost 27% last month.

- Dollar up. The initial reaction was USD strength, whilst equities extended higher with the S&P500 up 1.6% this week primed for a more than 5% monthly advance.

- Tariffs on. Less than 24 hours after, the White House appealed, and a federal appeals court temporarily paused the trade court’s ruling, which means that tariffs will stay in place – for now.

- Dollar down. The dollar came under renewed selling pressure, suggesting traders were eager to align with the broader trend of de-dollarization. Investors had better buckle up for a turbulent summer.

- Japan’s quick fix. In other news, Japan’s ministry of finance survey hints at reduced issuance, complicating global rate dynamics. Bond markets from Japan to the UK and US reacted positively, pushing prices up and yields down.

- Yields relief. That paused the weeks-long bond selloff forced by investors demanding bigger yields as they braced for increased inflation and government spending caused by US Trump’s trade and tax policies.

- Mixed macro. US consumer sentiment saw sharpest rise in four years but remains historically weak. Continuing jobless claims hit highest since 2021, and GDP in Q1 confirmed at -0.2%.

Global Macro

Tariff twists and turns

More flip-flopping. Markets were caught off guard by President Trump’s latest tariff threats targeting Europe and Apple. However, past Sunday, President Trump agreed to push the deadline to July 9 following a phone call with European Commission President Ursula von der Leyen.

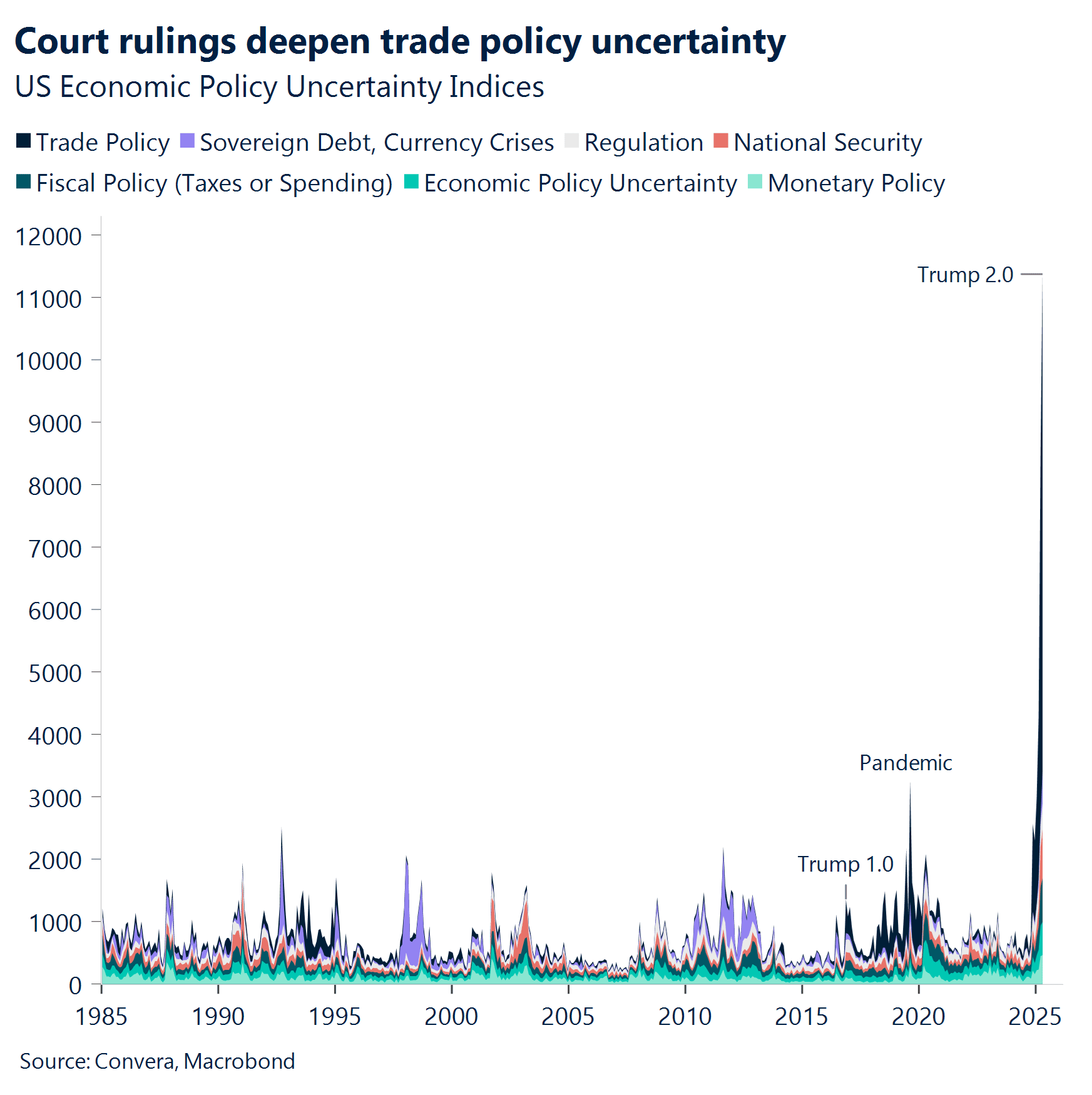

Tariffs are challenged. On Thursday, the US Court of International Trade ruled President Trump’s tariffs illegal, affecting fentanyl and immigration-related tariffs (10%–30%) on imports from China, Canada, and Mexico, as well as global trade surplus tariffs (10%+), with reciprocal tariffs suspended until 9 July. The ruling does not impact steel, aluminum (25%), auto, or auto parts tariffs. The administration has appealed, with the case likely headed to the Supreme Court to determine the legality of IEEPA-based tariffs.

Tariffs remain (for now). A federal appeals court granted a bid from the White House to temporarily suspend the lower court’s order though. The next hearing is on 5 June.

Japan bond market in focus. A recent survey by Japan’s Ministry of Finance suggests a potential reduction in bond issuance, introducing new complexities to market dynamics. Meanwhile, the Bank of Japan’s move toward policy normalization, ending yield curve control and possibly raising rates, poses risks to U.S. yields, as demand for new issuance can’t be given. Although global rates have declined through the week, under this evolving landscape, long-term yields are likely to stay elevated.

Mixed macro data. Consumer sentiment improved for the first time since November, with May’s Conference Board confidence index posting its sharpest rise in four years, though still at the lower end of the recent range. Meanwhile, US continuing jobless claims hit their highest level since 2021, pending home sales fell short of expectations, and Q1 2025 GDP contracted by -0.2%, slightly less than previously reported.

Week ahead

Tariff drama could overshadow macro data

Focus on inflation and growth. The upcoming week features a relatively heavy economic calendar, with inflation and growth metrics taking centre stage. Key releases include Eurozone preliminary CPI data on Tuesday, Australia’s Q1 GDP on Wednesday morning, and Canadian and US labour market data on Friday. These events will provide critical insights into economic conditions and central bank policy direction.

Inflation in focus. Inflation data from the Eurozone will set the tone for the week. Preliminary May CPI releases are scheduled for Tuesday evening, and these figures will inform expectations for the European Central Bank’s (ECB) policy decisions later in the week. Markets will also monitor inflation-related data from the US and other regions for further clues on global price pressures.

Growth indicators from major economies. Growth remains a key theme, with GDP data from Australia (Q1) dominating the midweek schedule. Factory orders and industrial production figures from Germany will further shape the growth narrative, while US factory orders and durable goods data will offer insights into business activity. Canada and the US cap the week with labour market updates, including US Nonfarm Payrolls on Friday.

Central bank decisions. The Bank of Canada rate decision on Wednesday will be a highlight for monetary policy watchers. Similarly, the ECB’s rate decision on Thursday will attract attention with a 25-basis point cut baked into market pricing.

Tariff drama. For now, the appeals court decision allow Trump’s tariffs to be used while the case is litigated. The next hearing is on 5 June, whilst the Trump administration has been ordered to respond again by June 9. The matter is widely expected to end up at the Supreme Court. Broad uncertainty remains elevated, keeping investors on edge.

FX Views

G10 strength on USD slide

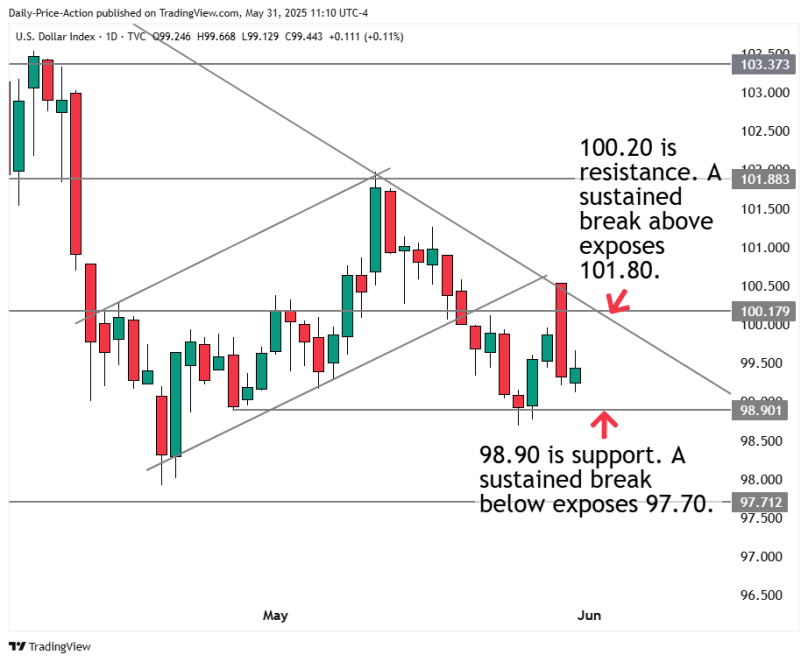

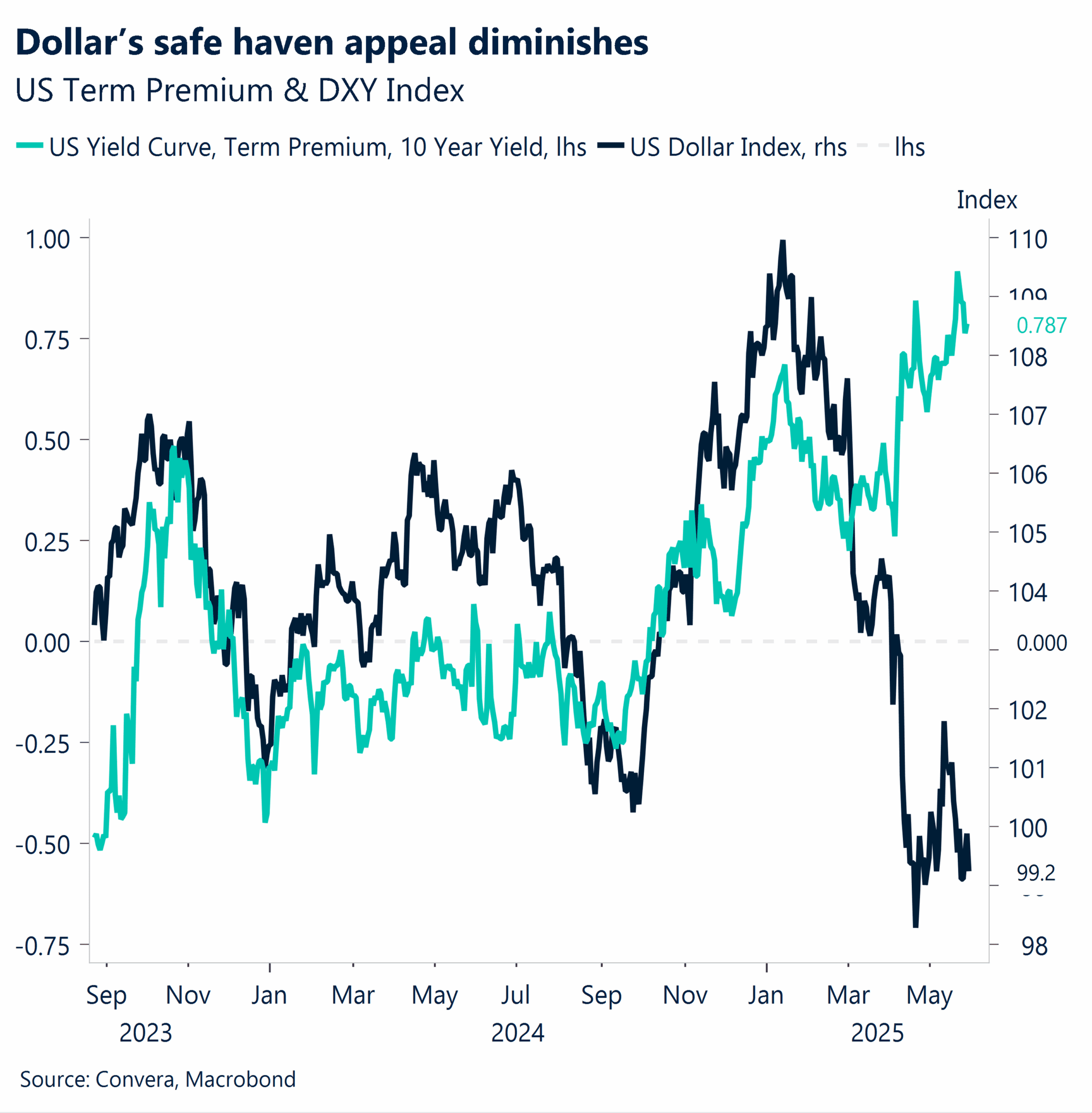

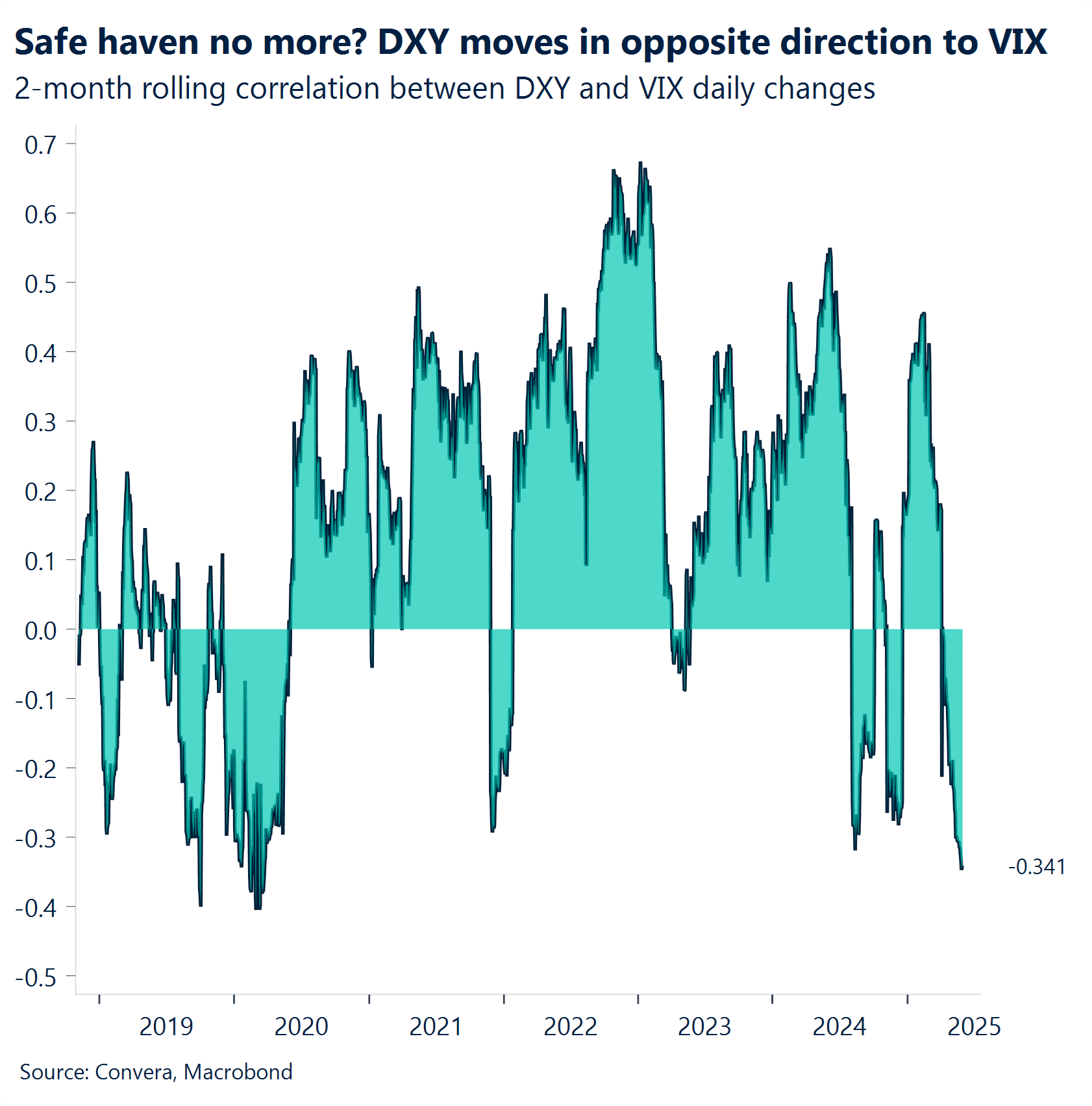

USD Dollar comes down from haven. The US dollar has seen a decline in its traditional safe-haven appeal, moving inversely to yields and the VIX. This suggests that despite current market volatility, the DXY is not being sought as a refuge, and higher yields are insufficient to attract investors, leading to capital outflows from US assets. Federal Reserve officials Kashkari and Williams reinforced the Fed’s “wait and see” stance this week, and the FOMC minutes echoed this sentiment, indicating that rate cuts are unlikely until there is greater clarity on tariffs and their impact on inflation. US durable goods orders fell by 6.3% in April, and the disappointing GDP release (-0.2% QoQ) confirmed the prevailing downbeat sentiment. Compounding this, the US Court of International Trade ruled late Wednesday that President Trump’s tariffs are illegal. While this ruling could provide some support for the dollar, the timing—coinciding with weak economic data—exacerbated market concerns, sending the DXY below 99.5. Looking ahead, the implications of this ruling remain uncertain. Earlier in the week, positive trade headlines had buoyed sentiment, raising hopes for policy improvements. The ruling could serve as a catalyst for more market-friendly policies, supporting the dollar, or conversely, prompt President Trump to shift focus toward imposing more aggressive tariffs on unaffected sectors.

EUR Euro momentum falters. Despite being the second most liquid alternative to the U.S. dollar, the euro has lost some traction this month, with EUR/USD slipping 0.1%, hovering around the $1.14 handle. Optimism surrounding the euro remains intact, particularly after ECB President Christine Lagarde’s “global euro moment” remarks, which have reinforced a euro-positive sentiment. However, soft German retail sales for April, disappointing PMI figures, and a weaker-than-expected CPI print from France highlight a lack of robust domestic macroeconomic support for the euro. The ECB maintains its dovish stance, with a rate cut expected on June 5, emphasizing growth over inflation. The key question now is whether deflationary risks will prove transitory or become more persistent, affecting future policy rate decisions. For now, markets are pricing in a 58bp rate cut from the ECB compared to 50bp from the Fed for the year, reinforcing the view that rate differentials alone should push EUR/USD lower while favoring the USD. Any further removal of risk premiums from the dollar—following eased trade tensions and recent legal battles—could see EUR/USD trading a leg lower in the near term.

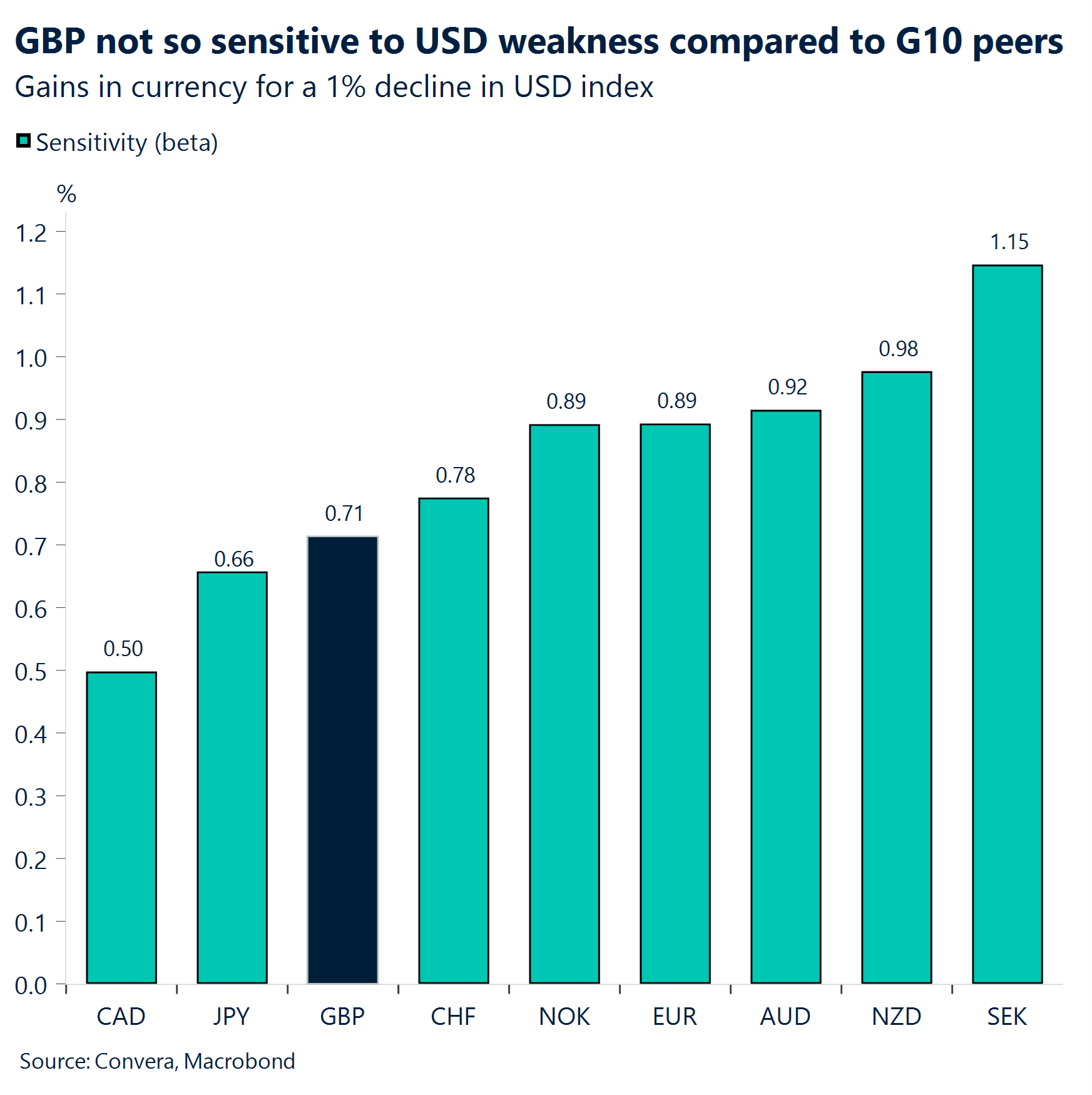

GBP Homegrown momentum. Sterling’s 7.6% gain against the dollar this year may largely reflect broad USD weakness, but its lower beta to the DXY sets it apart from many G10 peers, making it less reactive to dollar declines. Beyond dollar dynamics, GBP sentiment has notably improved too though, driven by UK trade agreements, strong domestic economic data, and the BoE’s relatively hawkish stance. These factors reinforce sterling’s idiosyncratic strength, making its rally more than just a dollar story. Although GBP/USD has fallen from $1.36 towards $1.34 this week due to renewed dollar demand, the pair remains above its 21-day moving average and other long-term moving averages in a sign that the uptrend is still intact for now. Indeed, zooming out on a monthly chart, we note the currency pair is primed to clock its fourth monthly rise in a row having last month closed comfortably above its 100-month moving average for the fourth time in about ten years. This chart looks bullish, with upside potential of $1.40 a possibility later this year, particular if investors resume offloading dollar-denominated assets amidst ongoing US policy angst. Meanwhile, GBP/EUR, is trading 1.5% higher month-to-date and might be poised to test the €1.20 handle soon thanks largely to widening rate differentials and the UK’s better trade position with the US.

CHF Defiant but SNB on the brink. Despite the tariff ruling and equity market rally, EUR/CHF remains below 0.94, reflecting growing distrust in US Treasuries and concerns over the Swiss National Bank’s policy constraints. That said, USD/CHF has rallied over 1% over the past week after rebound off the 0.82 support. Looking ahead, the SNB faces a tough decision ahead of its June 19 meeting, with markets split between a 25bp or 50bp rate cut. While the central bank is reluctant to return to negative rates, it may have little choice given economic pressures. Additionally, investors expect the SNB to be more constrained in FX intervention, aligning with Washington’s directives. The key question remains whether the SNB can be dovish enough to ease EUR/CHF downside risks, especially if the ECB proceeds with two more rate cuts.

CNY Manufacturing focus dominates new policy framework. China’s government is developing a comprehensive five-year plan targeting high-end technology manufacturing, particularly chip-making equipment production. The strategy aims to maintain manufacturing’s GDP share over the medium term, reflecting Beijing’s continued emphasis on industrial capacity expansion. The manufacturing-centric approach suggests policymakers prioritize export competitiveness over domestic demand rebalancing, potentially supporting yuan stability through trade surplus maintenance. USD/CNH remains below key psychological handle of 7.2000. The next key resistance levels for the pair will be 21-day EMA of 7.2109, 50-day EMA of 7.2385 and 200-day EMA of 7.2455. We do expect range-bound price action for this pair. It is still circa 3% from its all-time highs of 7.4290. Market participants will closely watch upcoming Chinese manufacturing PMI, non-manufacturing PMI, Caixin manufacturing PMI, and Caixin Services PMI for economic momentum insights.

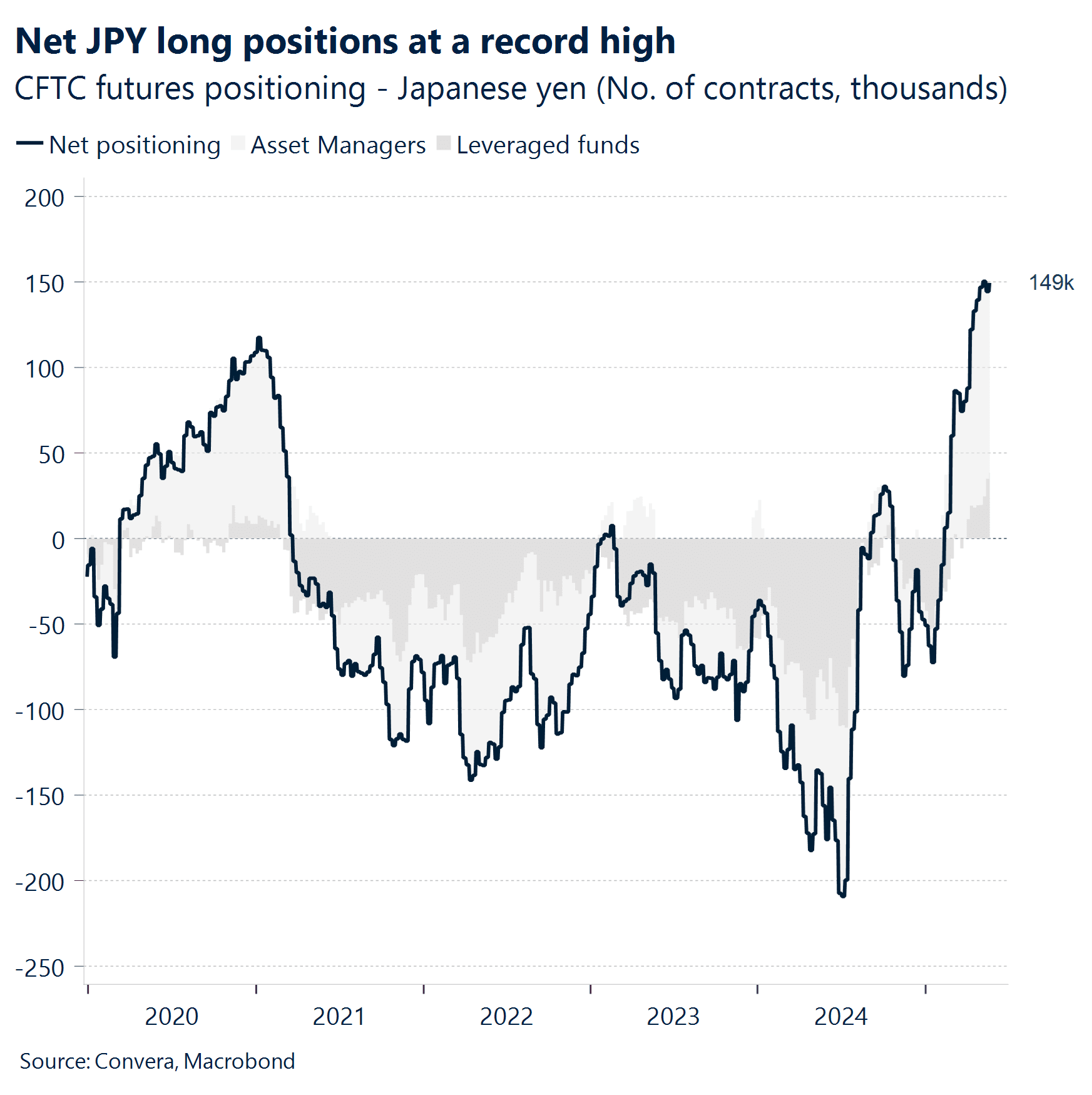

JPY Bond market tensions drive range-bound trading. Japan’s Ministry of Finance is considering adjustments to its bond issuance composition, potentially reducing super-long debt offerings amid record-high yields and declining institutional demand. Life insurers, traditionally major buyers, have reduced appetite for ultra-long duration bonds. The MoF will likely decide by mid-to-late June, having surveyed market participants about appropriate issuance volumes. USD/JPY has failed to break the psychological level of 145, after having touch recent highs of 146.28. USD/JPY has established a new trading range following recent volatility. The technical setup suggests consolidation below the 149.11 200-day moving average, while maintaining support above the crucial 140 level. Next key resistance barriers for the pair include 21-day EMA of 144.45 and 50-day EMA of 145.53. Market participants will focus on upcoming capital spending data, household spending figures, and au Jibun Bank Services PMI for economic activity confirmation.

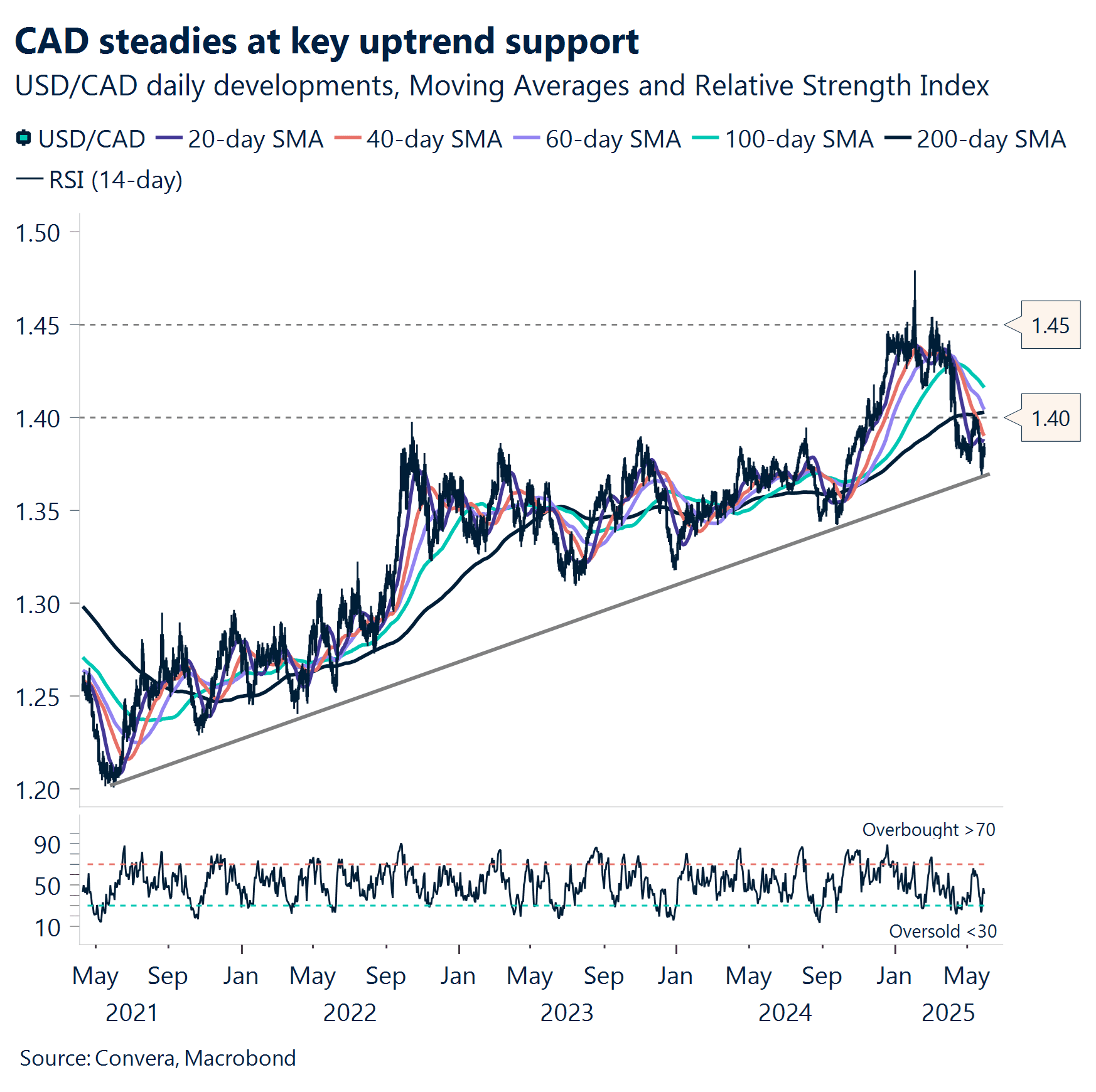

CAD Bounce from 2-year average. The USD/CAD has retreated about 6.6% from its 2025 high of 1.479, though it remains up approximately 4% year-to-date. Over the past month, the pair has been largely driven by persistent dollar weakness, further supported by investor relief following developments on tariffs and the U.S. tax bill. These factors prompted a shift away from the greenback, leading the USD/CAD to hit 1.368—its lowest level in eight months—before rebounding above 1.38 as fiscal concerns eased. Despite weakening domestic fundamentals and lingering global uncertainty, USD/CAD has stabilized after bouncing off its two-year average, finding key support at 1.37. This level coincides with a year-long trendline dating back to June 2021, reinforcing medium-term uptrend support. The recent recovery to 1.38 was influenced by oversold conditions, U.S.-Canada bond yield differentials, and renewed dollar strength. From a technical standpoint, the Loonie remains unable to close below its 100-week simple moving average (SMA) at 1.375, reinforcing its current range-bound trading pattern. If USD/CAD holds above 1.381, it could signal the end of its three-month decline. Additionally, the 60-day SMA is approaching a crossover below the 200-day SMA, setting up a key resistance zone near 1.40.

AUD Inflation progress stalls near critical technical junction. Australia’s headline CPI in April printed 2.4% y/y, higher than estimates of 2.3% but still tracking below the RBA’s inflation target midpoint of 2.5%. Trimmed mean CPI was 2.8%, up from 2.7% in March, suggesting underlying price pressures remain elevated. Several CPI lead indicators have recently rebounded, with business surveyed selling prices and the inflation gauge both rising back above 3% y/y, indicating potential stickiness in the disinflation process. AUD/USD has already gained circa 8%+ since rebounding from April 9 lows of 0.5915. AUD/USD continues to hover at its strong 21-day EMA as key support. A decisive break below 50-day EMA of 0.6385 would likely trigger an impulsive move lower, potentially targeting the next support confluence of 0.6200. A decisive break above key psychological resistance of 0.6500 will augur well for the pair. Market participants will monitor upcoming current account data, RBA meeting minutes, GDP figures, and trade balance for further policy guidance.

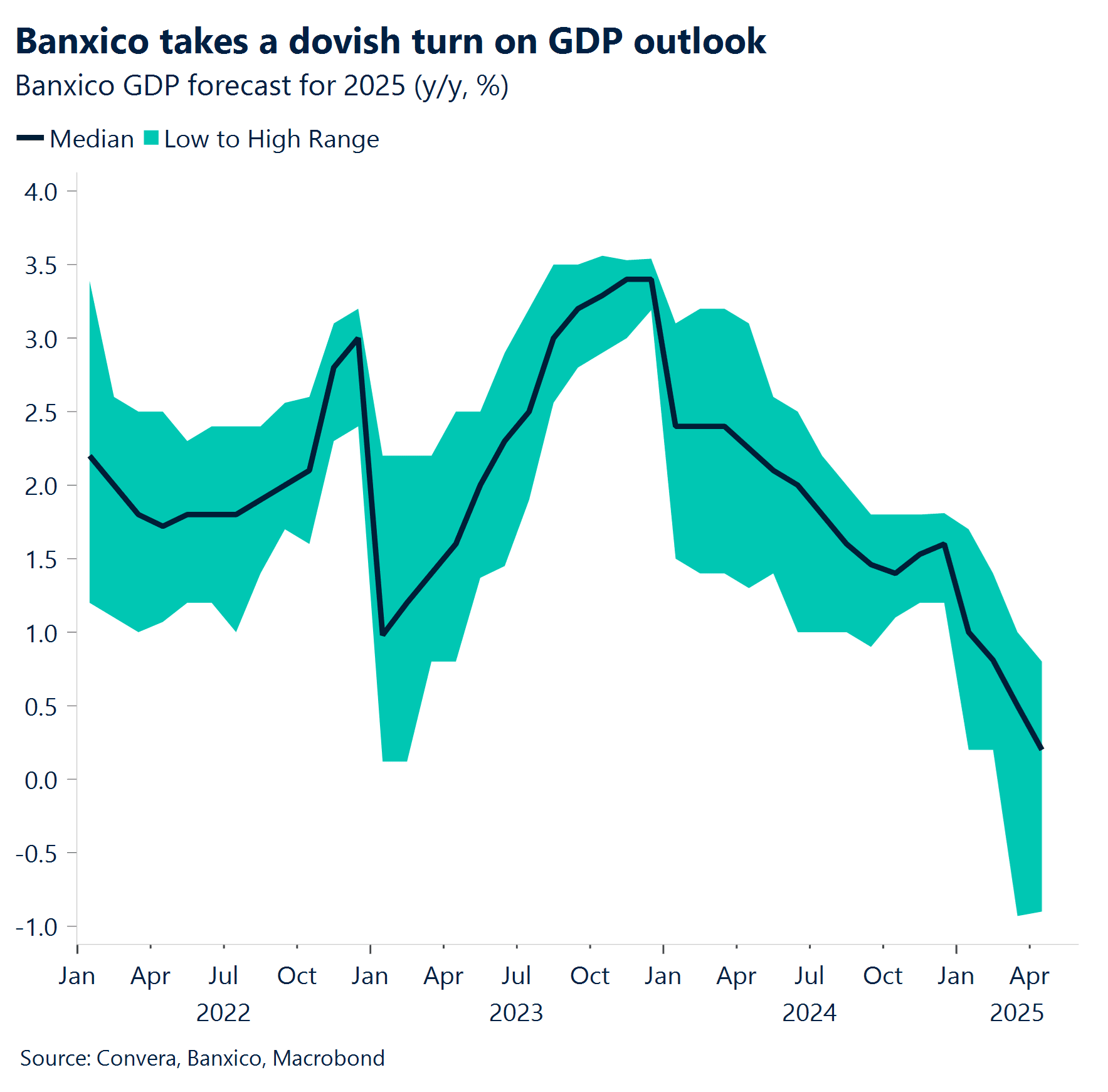

MXN Peso rally stalls. Banco de Mexico (Banxico) released this week its quarterly economic forecast, painting a cautious picture with clear downside risks to growth. GDP projections for 2025 took a sharp hit, falling well below market expectations. Governor Victoria Rodríguez Ceja announced that Mexico’s GDP is now expected to grow only 0.1% in 2025, down from a previous estimate of 0.6%. The 2026 outlook was also revised downward, from 1.8% to 0.9%, with Banxico citing a combination of internal economic weakness and global challenges, particularly shifts in U.S. trade policy, as key factors adding uncertainty to Mexico’s external demand. The Mexican peso reacted negatively to Banxico’s dovish tone. After three consecutive weeks of gains, momentum has lost steam and the USD/MXN has found support just above its 60-week SMA at 19.2, rebounding from weekly and 2025 lows at 19.18, though still below its five-year average of 19.5. A push to retest 2025 lows will require fresh momentum and weaker dollar. Banxico’s reluctance to signal a more aggressive easing cycle has kept market expectations anchored around a terminal rate near 6.5%, leaving carry-erosion concerns unchanged. In the near term, with the dollar strengthening across the board, the peso’s range is likely to hover between 19.2 and 19.4. The Mexican peso has staged a solid comeback, appreciating 9% from its yearly high of 21.2. After a rough 2024, where it tumbled nearly 20% from its low of 16.2, the currency has rebounded, posting a year-to-date gain of approximately 7% against the U.S. dollar.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.