The currency markets remain subdued in early trading this week, with the exception of a broad, mild Dollar weakness. Among the major currencies, movements have been muted despite notable developments. Swiss inflation falling back to 0% has increased pressure on the SNB to cut rates further to avoid deflation, but the Swiss Franc showed little response. Similarly, an unexpected improvement in Eurozone investor confidence failed to generate any sustained lift in the Euro.

In equities, European stocks were mixed, lacking clear conviction, while UK markets closed for a public holiday. US futures also point to a slightly weaker open. Meanwhile, oil prices saw some stabilization but remained lower for the day after OPEC+ agreed to a production hike over the weekend. WTI crude is attempting to recover, but the bearish bias remains as markets now anticipate a potential production surplus in the second half of the year.

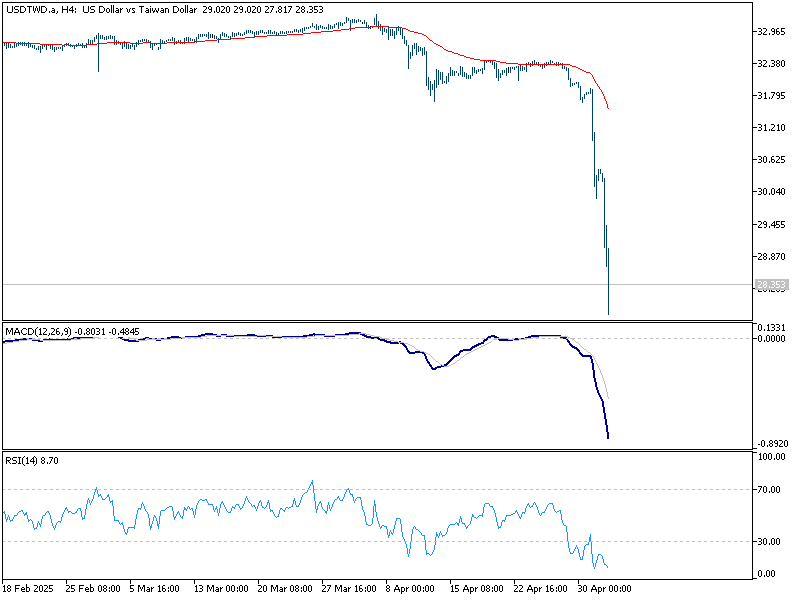

The most eye-catching action is unfolding in Asian currency markets. Taiwanese Dollar soared more than 5% to a three-year high against Dollar, capping an 8% gain in just two sessions. The sharp move followed the conclusion of US-Taiwan trade talks last week, stoking speculation that a tacit agreement to strengthen the TWD may have been reached. While it’s denied by Taiwan’s central bank, the pace and scale of the rally suggest market confidence in a policy-backed shift, which would align with US interests in reducing bilateral trade imbalances.

China’s offshore yuan also rallied sharply, touching a six-month high against the greenback. While no official catalyst was pinpointed, the move followed speculation that the US and China may soon begin tariff negotiations. However, any such discussions would be complex and drawn-out, likely injecting fresh volatility into CNY markets.

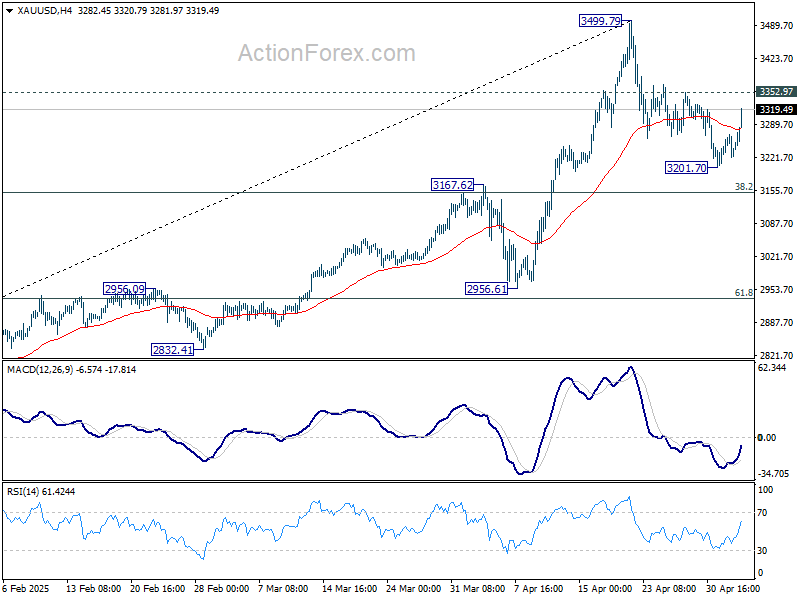

Technically, one focus now is on how far Gold’s rebound could go. Firm break of 3352.97 resistance will indicate that correction from 3499.79 has already completed at 3201.70, ahead of 3167.62 resistance turned support. Retest of 3499.79 should be seen next, with prospect of breaking through this level to resume the record run.

Eurozone Sentix confidence surges to -8.1 as investors cheer calm EU response to trade war

Eurozone Sentix Investor Confidence rose sharply from -19.5 to -8.1,well above expectations. Current Situation Index climbed from -23.3 to -19.3, the highest level since August 2024. Expectations Index turned positive, rising from -15.8 to 3.8.

Sentix credited the European Commission’s “level-headed response” toward escalating US trade actions for the improving sentiment. Additionally, a surprising improvement in inflation data has reinforced expectations that ECB will be able to continue its gradual rate-cutting cycle.

While investors are clearly more upbeat, Sentix noted the mood was “more subdued but basically ‘calm’”, comparing to March.

ECB’s Panetta warns protectionism threatens global prosperity

Italian ECB Governing Council member Fabio Panetta warned today that rising protectionism poses a serious threat to global economic stability

Speaking at an event, Panetta said, “Openness to trade has benefited both advanced and developing nations, reducing inequality and lifting hundreds of millions of people out of extreme poverty.”

However, “protectionism threatens to undo these achievements and to weaken the very fabric of global prosperity,” he added.

He emphasized that geopolitical tensions, alongside growing uncertainty in global trade, are becoming central considerations for policymakers.

Swiss CPI drops to 0% as import deflation worsens

Swiss consumer price growth came to a standstill in April, with headline CPI unchanged month-on-month for a second consecutive month.

On an annual basis, inflation slowed sharply from 0.3% yoy to 0.0% yoy, marking a return to flat price levels not seen since the disinflationary spell of early 2021.

Core CPI (excluding fresh and seasonal products, energy and fuel) also lost momentum, easing from 0.9% yoy to 0.6% yoy.

The softness in inflation was driven by a decline in domestic product prices, which fell -0.1% mom and decelerated from 1.0% yoy to 0.8% yoy. Meanwhile, imported product prices offered a small offset, rising 0.3% mom but still contracting -2.5% yoy (prior -1.7% yoy).

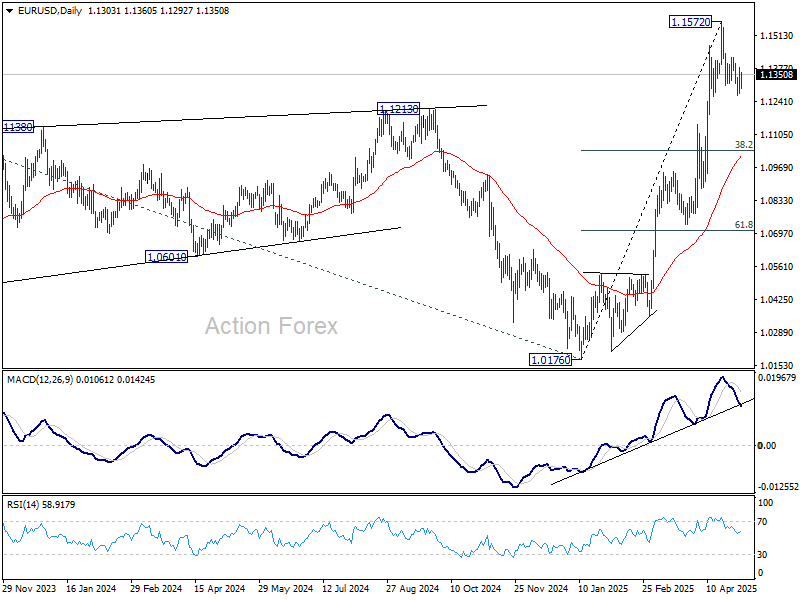

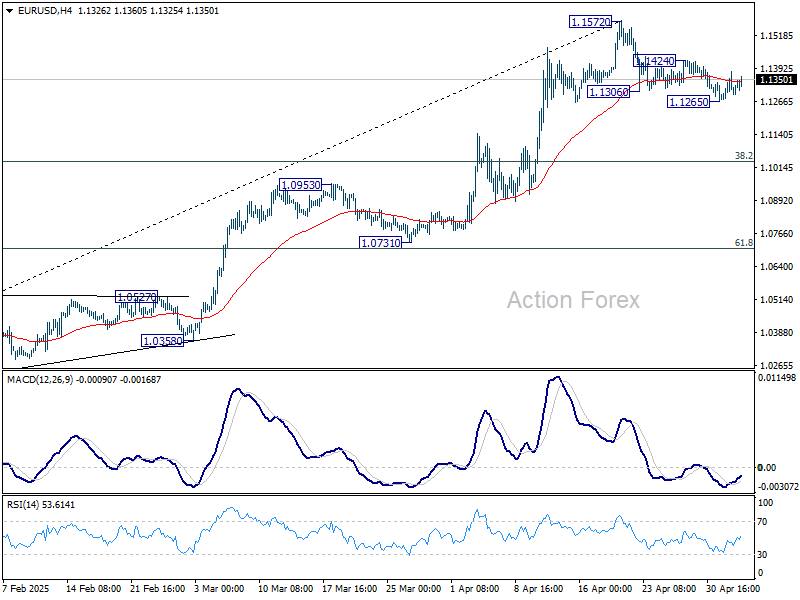

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1257; (P) 1.1319; (R1) 1.1364; More…

EUR/USD is staying in tight range above 1.1265 and intraday bias remains neutral. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.