The US markets remain remarkably steady overnight despite a string of soft US economic releases overnight. Disappointing job and services data failed to trigger any meaningful selloff in equities, while Dollar edged slightly lower. Market pricing for Fed policy remains broadly unchanged, with a 96% chance of a hold at the upcoming meeting and a 70% probability for no change in July. Still, Friday’s non-farm payrolls report looms as a potential catalyst for repricing should the labor market disappoint more sharply than expected.

On the trade front, tensions are simmering as the US formally doubled its tariffs on imported steel and aluminum. Canada is now openly preparing retaliatory measures should ongoing negotiations with Washington break down. Prime Minister Mark Carney told lawmakers that Canada is engaged in “intensive negotiations” but is also preparing reprisal tariffs in parallel.

Meanwhile, EU-US trade talks appear to be moving in a more constructive direction. After a meeting in Paris, EU negotiator Maros Sefcovic and US Trade Representative Jamieson Greer described the discussions as productive and advancing “at pace.” Sefcovic noted the talks are now “very concrete,” and Greer echoed that sentiment, signaling genuine willingness from both sides to achieve a reciprocal agreement.

Attention now turns to ECB’s policy decision later today. A 25 bps rate cut is fully priced in, with the real focus on whether President Lagarde signals a pause for July. Given the subdued market response to recent central bank events and the current range-bound conditions, it remains to be seen whether today’s meeting will break the stalemate .

In weekly performance terms, Dollar is currently the worst performer, followed by Swiss Franc and Loonie. At the other end of the spectrum, Kiwi leads gains, with the Aussie and Sterling also modestly firmer. Euro and Ten are trading in the middle of the pack. Yet, almost all major pairs and crosses remain trapped within last week’s ranges.

In Asia, at the time of writing, Nikkei is down -0.53%. Hong Kong HSI is up 0.60%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is down -0.039 at 1.466. Overnight, DOW fell -0.22%. S&P 500 rose 0.01%. NASDAQ rose 0.32%. 10-year yield fell -0.095 to 4.365.

Looking ahead, German factory orders, UK PMI construction and Eurozone PPI will be released in European session, but the main event is defintely ECB rate decision and press conference. Later in the data, Canada will release trade balance and Ivey PMI. US will release jobless claims and trade balance.

ECB to cut, focus on Lagarde’s signal for a July pause

ECB is set to lower its deposit rate by 25 bps to 2.00% today, marking the eighth cut of this easing cycle and bringing policy deep into neutral territory. With inflation falling back below the 2% target in May, the case for further easing is clear in the near term. However, the main focus will be on President Christine Lagarde’s forward guidance, particularly whether she signals a July pause in rate cuts, and the ECB’s updated economic projections.

The case for caution is clear. The Eurozone faces a highly uncertain backdrop with multiple crosscurrents. Trade war remain front and center, with US President Donald Trump’s tariff agenda weighing heavily on confidence and investment. Retaliatory moves from the EU could compound the hit to activity. At the same time, the surprised surge in Euro risks exerting additional downward pressure on inflation. Amid this uncertainty, ECB is expected to lower both its 2025 growth and inflation forecasts, acknowledging the softening outlook.

At the same time, medium-term fundamentals could provide some support. The EU’s major rearmament plans and Germany’s fiscal pivot to expansion are likely to bolster investment and domestic demand over time. That said, these structural measures will take time to feed through.

A July pause would allow policymakers to evaluate how these domestic tailwinds and external headwinds ultimately shape the outlook, particularly as geopolitical and policy unpredictability continues to cloud the picture.

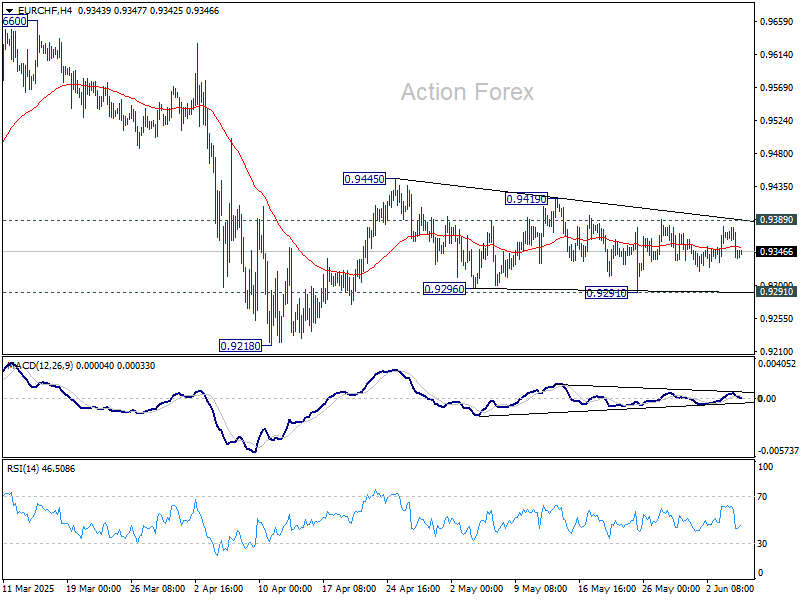

Technically, EUR/CHF’s near term price actions from 0.9445 are more likely than not a triangle consolidation pattern. That is, rise from 0.9218 is in favor to resume, even as a corrective move. Break of 0.9389 minor resistance will be a bullish sign and further break of 0.9419 should sent EUR/CHF through 0.9445 resistance.

Japan’s real wages fall -1.8% yoy in April, down for the fourth month

Real wages in Japan fell by -1.8% yoy in April, marking the fourth consecutive month of decline as persistent inflation continued to erode household purchasing power.

While nominal wages rose 2.3% yoy, slightly below the expected 2.6%, gains were outpaced by a still-elevated consumer inflation rate of 4.1%, driven by rising food and energy costs. The inflation metric used by the labor ministry has remained near 4% for five straight months, keeping real income in negative territory.

On the positive side, base salaries rose 2.2% yoy, the fastest increase in four months and well above March’s 1.4% yoy gain. This also marked the 42nd consecutive month of growth in regular pay. Overtime pay rebounded with a modest 0.8% yoy rise, while special payments grew 4.1% yoy.

China’s Caixin PMI composite falls to 49.6, contracts for first time since 2022

China’s Caixin PMI Services rose modestly from 50.7 to 51.1 in May, aligning with expectations. However, the gain in services was not enough to offset the drag from manufacturing, as PMI Composite slipped into contraction at 49.6, its first reading below 50 since December 2022.

Wang Zhe of Caixin Insight Group noted that the manufacturing slump was weighing heavily on the overall market, with new export orders remaining “sluggish” across both goods and services. Although input costs rose slightly, firms were unable to pass these on to customers, with selling prices continuing to fall and compressing profit margins.

Caixin flagged “unfavorable factors remain relatively prevalent”, with growing external trade uncertainty and “noticeable weakening” in macro indicators at the start of Q2. The “significantly intensified”downward pressure raises the urgency for further targeted policy support.

Fed’s Beige Book: General tone slightly pessimistic and uncertain

Fed’s Beige Book report paints a picture of slowing US economy marked by pervasive caution and subdued sentiment.

Economic activity was reported to have “declined slightly” overall, with half of the twelve Districts seeing slight to moderate declines, while three reported no change and three noted slight growth. The general tone remains “slightly pessimistic and uncertain,” echoing the previous report, as elevated policy and economic uncertainty continues to weigh on both business and household decision-making.

Consumer spending trends were mixed, with most Districts reporting little change or modest declines. However, in some cases, spending picked up on goods expected to be affected by tariffs—suggesting front-loading behavior amid trade concerns. Employment levels were largely stable, while price pressures persisted, rising at a moderate pace.

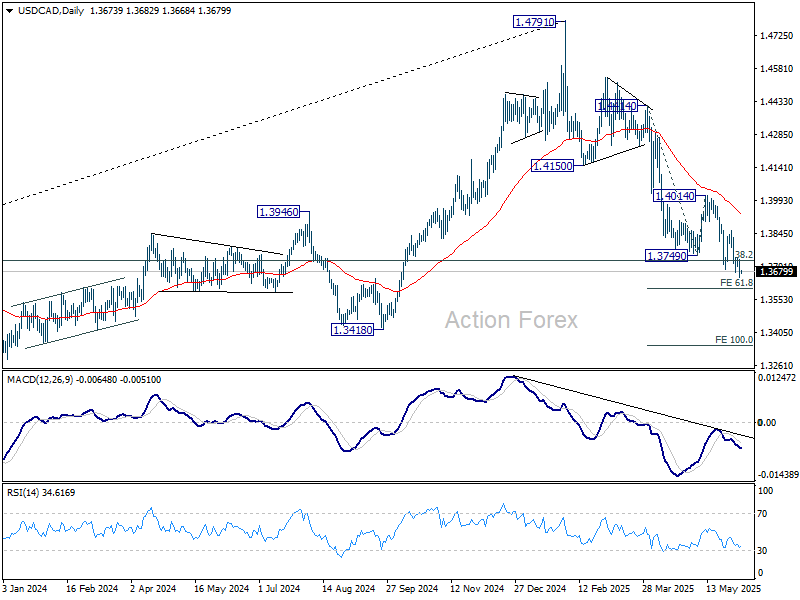

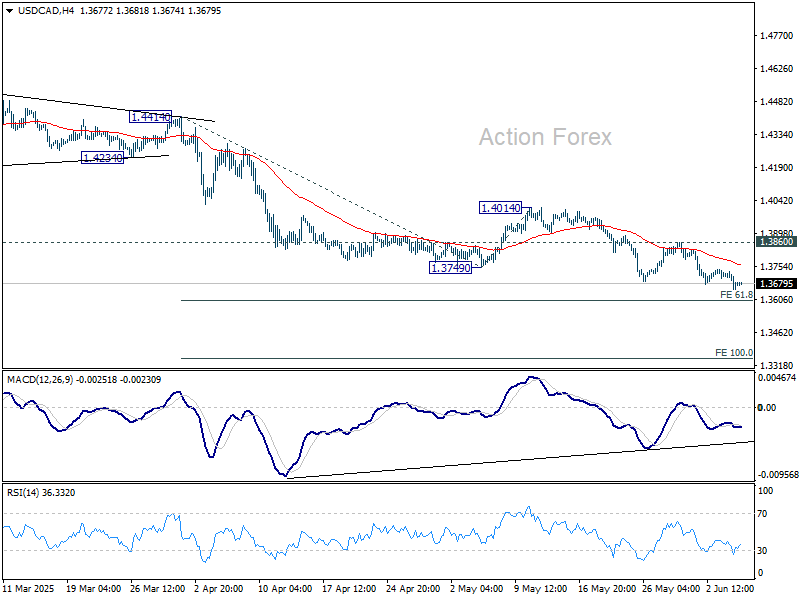

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3645; (P) 1.3688; (R1) 1.3724; More…

USD/CAD’s decline from 1.4791 is still in progress and intraday bias stays on the downside. Next target is 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. Firm break there will pave the way to 100% projection at 1.3349. On the upside, outlook will stay bearish as long as 1.3860 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.