Is Archer Daniels Midland (ADM) Still Attractive After Strong 12 Month Share Price Gains

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

If you are wondering whether Archer-Daniels-Midland (ADM) is still offering value at today’s levels, this breakdown will help you see what the current share price really reflects.

The stock last closed at US$69.73, with returns of 18.1% year to date and 57.5% over the past year, even though the 7 day and 30 day returns of 5.6% and 3.1% are negative.

Recent headlines have focused on Archer-Daniels-Midland’s role in global food supply chains and its position in agricultural processing. This keeps attention on the stock when sentiment around food and commodity related names shifts, and these themes help frame how investors think about both upside potential and risks around the current price.

Archer-Daniels-Midland currently has a valuation score of 3 out of 6. The sections that follow will walk through what that means using different valuation approaches, before finishing with a broader way to think about ADM’s valuation story over time.

A Discounted Cash Flow model projects a company’s future cash flows and then discounts them back to today’s value, so you can compare that estimate with the current share price.

For Archer-Daniels-Midland, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about $4.12b. Analysts provide explicit forecasts out to 2027, including an estimate of $1.99b in free cash flow for 2027, and Simply Wall St extrapolates further, with projected free cash flow of about $2.18b in 2035. All these future values are discounted back into today’s dollars to arrive at an estimated intrinsic value per share of $94.74.

Compared with the recent share price of $69.73, the DCF output suggests Archer-Daniels-Midland is trading at a 26.4% discount to this intrinsic value. On this model, the stock appears undervalued.

For a profitable company like Archer-Daniels-Midland, the P/E ratio is a useful way to see how much you are paying for each dollar of earnings. It effectively reflects what the market is willing to pay today for those earnings, given its view of the business and its risks.

In general, stronger growth expectations and lower perceived risk tend to support a higher, or more generous, P/E ratio, while slower expected growth or higher risk usually align with a lower P/E. Archer-Daniels-Midland currently trades on a P/E of 31.17x. That compares with the Food industry average P/E of about 21.02x and a peer group average of 54.00x, so the stock sits above the sector but below peers on this metric.

Simply Wall St’s Fair Ratio for Archer-Daniels-Midland is 22.07x. This is a proprietary P/E level that reflects factors such as the company’s earnings growth profile, industry, profit margins, market cap and risk characteristics. Because it blends these fundamentals, it can give you a more tailored reference point than a simple comparison with peers or industry averages. Set against the current P/E of 31.17x, the Fair Ratio suggests Archer-Daniels-Midland is trading on a richer multiple than those fundamentals might support.

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring your view of Archer-Daniels-Midland together in one place by tying a simple story about the business to a set of revenue, earnings and margin assumptions. This is then turned into a Fair Value that you can compare with the current price on the Simply Wall St Community page. Because Narratives update when new news or earnings arrive, you can see in real time how different views line up. For example, one investor might lean toward a higher Fair Value of about US$77.00 based on faster growth and margin expansion, while another leans toward a lower Fair Value of about US$50.00 based on more conservative assumptions. This gives you a clear range of perspectives to test your own decision about whether the current price feels high, low or roughly in line with your expectations.

For Archer-Daniels-Midland, we will make it really easy for you with previews of two leading Archer-Daniels-Midland Narratives:

Each one ties a simple story about the business to explicit assumptions on revenue, margins, earnings and the P/E multiple that would need to apply, so you can quickly see which set of expectations is closer to your own.

🐂 Archer-Daniels-Midland Bull Case

Fair Value: US$77.00

Implied discount to this Fair Value: 9.5% based on the latest close of US$69.73

Assumed revenue growth: 14.35% a year

Leans on faster expansion in higher margin areas such as enhanced nutrition, flavors, Specialty Ingredients and decarbonization projects to support revenue mix quality and earnings.

Relies on analysts who expect revenues of about US$120.0b and earnings of US$2.3b by 2029, with profit margins rising from 1.3% to 1.9% and a P/E of 20.0x on those earnings.

Frames the current market price as close to fair, with the bullish fair value only modestly above the latest share price. As a result, the gap rests more on confidence in execution than on a large pricing difference.

🐻 Archer-Daniels-Midland Bear Case

Fair Value: US$63.82

Implied premium to this Fair Value: 9.3% based on the latest close of US$69.73

Assumed revenue growth: 4.73% a year

Builds in more modest revenue growth and higher profit margins of 2.3% by 2029, with earnings of US$2.1b and a P/E of 17.9x, and still lands below the current share price.

Highlights risks from policy uncertainty around biofuels, softer volumes and margins in Ag Services and Carbohydrate Solutions, and ongoing compliance and reputational pressures.

Suggests that even with business improvement, the current price already reflects optimistic expectations. Any setback on policy, commodities or execution could therefore pressure the multiple investors are willing to pay.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

From the attention they received after President Donald Trump issued executive orders to secure the nation’s supply of critical minerals to the interest that rare-earth stocks like MP Materials (MP +2.49%) and USA Rare Earth (USAR 3.41%) received after the government announced equity investments in them, it’s clear that rare-earth stocks are having their day

A Palantir sign displayed on an office building by Poetra_RH via Shutterstock Retail trader darling and AI-led data analytics company Palantir’s (PLTR) stock should have been an expected beneficiary of the U.S./Israel and Iran war in the Middle East. Thanks to its advanced suite of products that aid decision-making and its proximity to the U.S.

Despite its volatility and occasional bear markets, the U.S. stock market remains one of the best long-term wealth-creation tools for everyday investors. It represents the potential, growth, and possibilities of the global economy in a way that nothing else really does. What’s interesting is that it often rewards those who do the least with it.

Got story updates? Submit your updates here. › An extreme close-up of the intricate machinery powering the stock market’s complex financial ecosystem, reflecting the technical analysis and data-driven insights that guide investment decisions.Boston Today The article provides an in-depth analysis of the current stock market trends, focusing on the performance of major Indian stock indices

Nvidia (NVDA +2.59%) and Broadcom (AVGO +4.69%) are two of the top AI computing companies to invest in right now. Each of their stocks has done incredibly well over the past few years, with Nvidia up 36% since the start of 2025 and Broadcom up over 50%. Each stock has risen so much over the

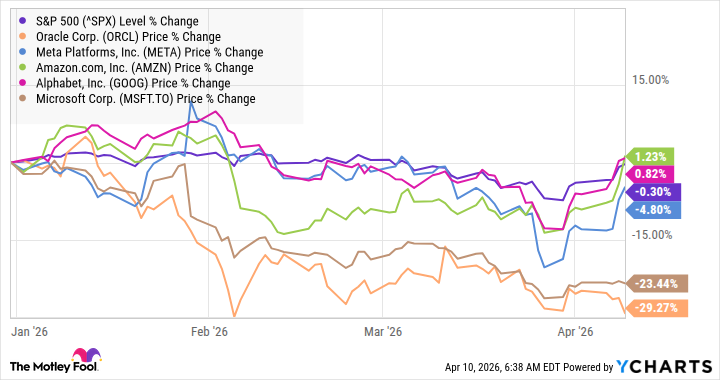

The market is, completely understandably, focused on artificial intelligence (AI) hyperscalers to determine whether there’s an AI bubble brewing. Those concerns are magnified by the share price performance of the leading hyperscaler companies in 2026 (see chart). The two that stand out the most are Oracle (NYSE: ORCL) and Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), and

Stock market volatility is the new norm, Goldman Sachs says, and it’s not as simple as markets being upset by geopolitical turmoil like the Iran war. Loading audio narration… The conflict in the Middle East has fueled the recent spike in equity volatility, Goldman says, but the firm’s macro strategy research team sees an ongoing

Dow Inc. (NYSE:DOW) is among the stocks Jim Cramer reviewed while discussing the Iran ceasefire that triggered a relief rally. Cramer explained why stocks like Dow are benefiting, as he commented: LyondellBasell and Dow, commodity chemical makers, they’re benefiting from the man-made petrochemical shortage caused by the war… you know what? I’m not so sure

Nvidia (NVDA +2.59%) remains the leader in the artificial intelligence (AI) industry thanks to its market-leading advanced chips that are ideal for training AI models, as well as its CUDA software platform that unlocks the power of its chips and makes it hard for competitors to lure developers away, which has given Nvidia a competitive

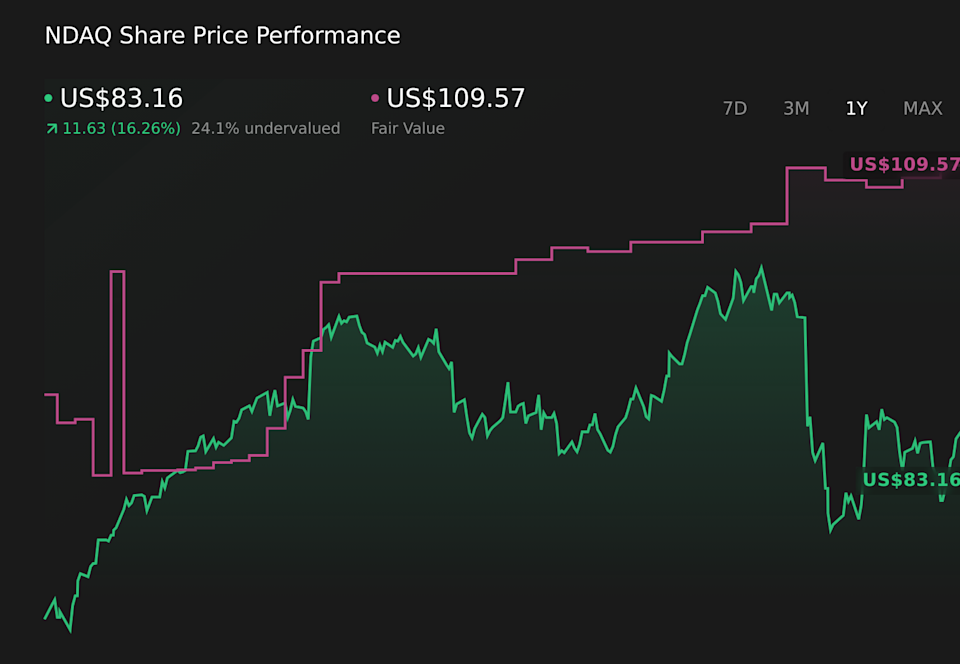

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE. Nasdaq’s latest fair value estimate has been nudged from US$109.57 to US$106.87, a shift of about US$3 per share that signals a more finely tuned

Bread Financial Holdings, Inc. (NYSE:BFH) is among the stocks Jim Cramer reviewed while discussing the Iran ceasefire that triggered a relief rally. Cramer said that the company has a “real niche,” as he stated: There’s a real business here. This company is the financing engine behind a lot of branded credit card programs that consumers

Every share of the SPDR S&P 500 ETF Trust (NYSEMKT: SPY) you own, and every Treasury bond in your retirement account, exist inside a market that foreign investors have filled with more than $35 trillion in capital. That figure, from the U.S. Treasury’s most recent annual survey published in June 2025, is up from roughly

Nvidia (NVDA +2.59%) hasn’t been its normal self lately. Over the past few years, Nvidia has always been a top performer. However, it hasn’t lived up to those expectations so far in 2026. The stock is down about 5% this year and hasn’t really done anything since August 2025. Given the explosive returns Nvidia has

The stock market has been on pins and needles over the past six weeks as news about the war in the Middle East, energy prices, and President Donald Trump’s inconsistent predictions about the war have sent it whipsawing up and down. The Chicago Board Options Exchange Volatility Index, or VIX, spiked above 30 in recent

American Express Company (NYSE:AXP) is among the stocks Jim Cramer reviewed while discussing the Iran ceasefire that triggered a relief rally. Cramer was bullish on the stock during the episode, as he said: American Express, its customer base skews wealthier, and demand for premium products can stay strong even if the rest of the economy

When it comes to investing in the stock market, it’s not always about trying to achieve the highest levels of capital growth in your portfolio. Some people have the simple objective of owning companies that provide them with a nice income stream. Along those lines, here’s one of the best dividend stocks to buy with

Roughly three decades ago, the mainstream proliferation of the internet changed America forever. After a long wait, the next game-changing technology has arrived: artificial intelligence (AI). Empowering software and systems with the tools to make split-second, autonomous decisions is a greater than $15 trillion global opportunity by 2030, according to PwC analysts. The rise of

Despite a fragile ceasefire currently, there’s still potential trouble brewing from the conflict in Iran. Mainstream automakers such as Ford Motor Company (F 0.90%) and General Motors (GM 0.40%) don’t do big business in the Middle East and remain relatively unimpacted by the current Iran conflict. It’s a different scenario for high-flying luxury stocks such

We’ve certainly seen a handful of solidly bullish days of late. Broadly speaking, though, the market’s still at risk of a full-blown correction. At the very least, investors would be wise to remain defensively minded. To this end, there’s one particular dividend stock that will not only become more attractive on any marketwide pullback, but

Over the last century, no other asset class has come particularly close to rivaling stocks in annualized returns. While bonds, commodities, and real estate have all increased in value, the Dow Jones Industrial Average (^DJI 0.56%), S&P 500 (^GSPC 0.11%), and Nasdaq Composite (^IXIC +0.35%) have outpaced them all. But just because stocks outperform over