Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

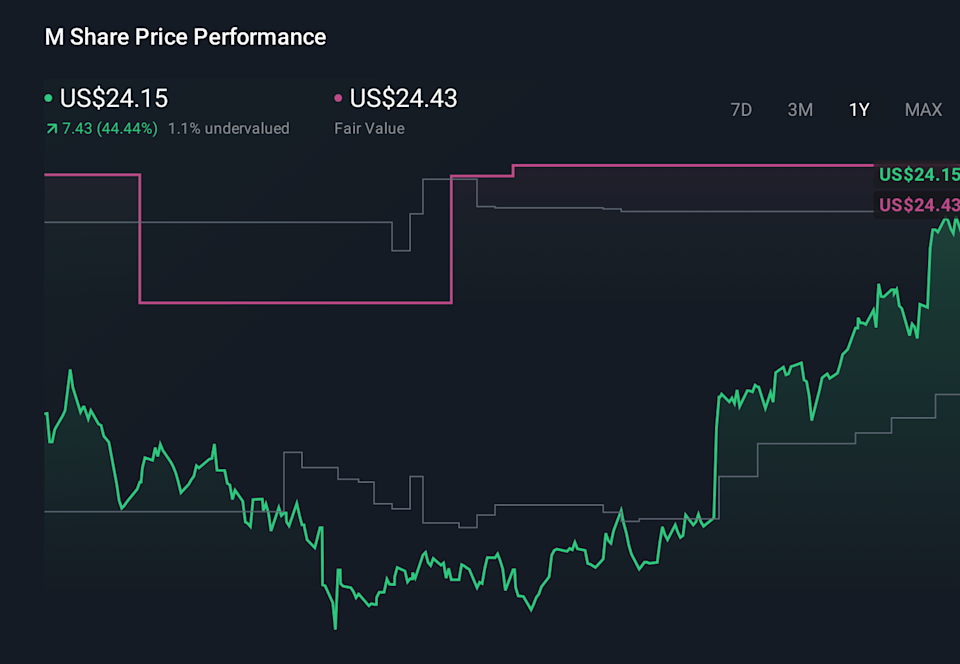

Tigo Energy’s updated analyst model now points to a fair value price target of US$6.13, compared with the previous US$5.63. That shift is closely tied to new revenue and earnings estimates, along with balance sheet moves such as using cash to address the US$50m convertible, rather than a simple change in sentiment. Read on to see what is driving the revised target, the mix of bullish and cautious views, and how you can track this evolving narrative over time.

-

Northland, via analyst Gus Richard, lifted its Tigo Energy price target to US$5.50 from US$5. This supports the view that the revised fair value in the analyst model is in line with at least one published target.

-

Northland increased its revenue, GAAP EPS and EBITDA estimates after Tigo’s latest report. This indicates that the firm sees room for operating and earnings metrics to support the updated valuation work.

-

The use of cash on hand to fully pay off the US$50m convertible due in Q3 is viewed positively by Northland. This suggests a cleaner balance sheet that may reduce financing overhang in future quarters.

-

Northland’s rating remains at Outperform rather than a higher conviction stance. This can signal that, while the firm is positive, it still sees execution and earnings delivery as key watchpoints.

-

The earnings print was described as in line with consensus once the IP sale is excluded. As a result, recent results are not a clear beat, leaving less immediate fundamental momentum for investors looking for stronger upside signals.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

We’ve flagged 2 risks for Tigo Energy. See which could impact your investment.

-

Tigo Energy filed a US$15,000,000 follow-on equity offering, issuing 5,000,000 common shares at US$3.00 per share in a registered direct deal.

-

The company completed a separate at-the-market equity program, raising US$14,221,459 through multiple tranches and issuing more than 7,000,000 common shares at various prices.

-

Management issued earnings guidance with expected revenue of US$25,000,000 to US$27,000,000 for the quarter ending 31 March 2026 and US$130,000,000 to US$135,000,000 for full year 2025, tied to projected 26% to 30% growth.

-

Tigo announced a partnership with CELTEC to distribute its rapid shutdown and optimizer products across Central America and the Caribbean and reported expansion of its Green Glove and installer support programs, which was associated with fewer installation related support tickets.

-

Fair value in the updated model is US$6.13, compared with the prior US$5.63.

-

Revenue growth assumption is now about 25.77%, compared with roughly 28.63% previously.

-

Net profit margin assumption is now roughly 9.61%, compared with about 10.61% before.

-

Future P/E in the model is now roughly 37.2x, compared with about 27.0x previously.

-

The discount rate input is now about 9.29%, compared with 9.30% previously.

Narratives link a company’s business story to the forecasts and assumptions that sit behind a fair value estimate. They refresh as new earnings, guidance, and balance sheet data come through so you can see how the story evolves over time.

Head over to the Simply Wall St Community and follow the Narrative on Tigo Energy to stay up to date on:

-

How Tigo’s push into EMEA markets with supportive solar policies ties into expectations for revenue growth and earnings stability.

-

The role of rising solar safety and rapid shutdown requirements in supporting demand for Tigo’s module level power electronics and margin assumptions.

-

Key risks such as heavy reliance on a single MLPE product family, concentrated international exposure, and the refinancing or repayment of the US$50m convertible.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TYGO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com