Exploring Three Undiscovered Gems in Europe’s Stock Market

As European markets show signs of optimism, with the STOXX Europe 600 Index posting a notable gain of 3.92% amidst easing geopolitical tensions, investors are increasingly looking toward small-cap opportunities that might offer unique value in this dynamic environment. With inflationary pressures and economic forecasts impacting broader market sentiment, identifying stocks that demonstrate resilience and growth potential can be particularly rewarding for those exploring Europe’s stock landscape.

Let’s explore several standout options from the results in the screener.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Danske Andelskassers Bank A/S offers a range of banking products and services to private individuals, small and medium-sized businesses, and agricultural clients in Denmark, with a market capitalization of DKK3.88 billion.

Operations: The bank generates revenue primarily from its banking segment, which amounts to DKK863.87 million. It serves private individuals, small and medium-sized enterprises, and agricultural clients in Denmark.

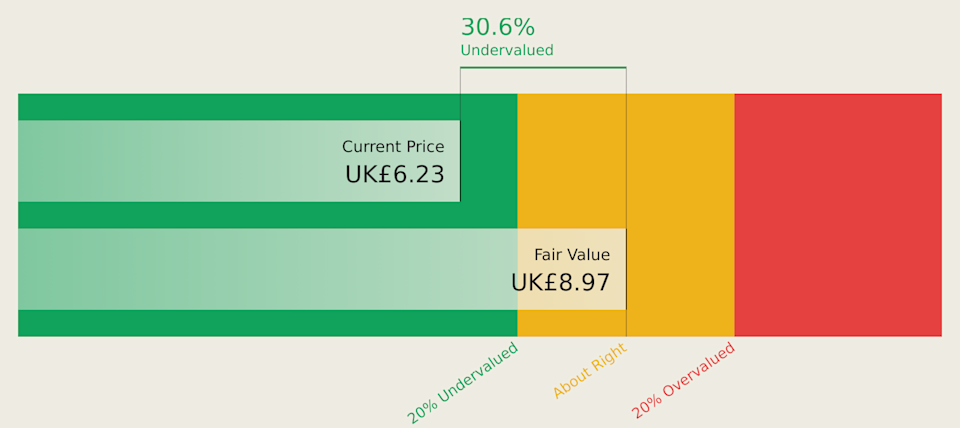

Danske Andelskassers Bank, with assets totaling DKK18.7 billion and equity of DKK2.9 billion, stands as a notable player in the financial sector. Its liabilities are primarily low-risk, with 91% sourced from customer deposits. Despite a recent dip in earnings growth at -4.5%, this is still ahead of the industry average of -8.2%. Total deposits amount to DKK14.4 billion against loans of DKK9 billion, reflecting a stable funding structure. The bank trades at 23% below estimated fair value, suggesting potential upside for investors seeking value opportunities within Europe’s financial landscape.

CPSE:DAB Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★★★

Overview: Caisse Régionale de Crédit Agricole Mutuel du Languedoc Société coopérative is a French cooperative bank offering a range of banking products and services, with a market capitalization of approximately €1.56 billion.

Operations: Caisse Régionale generates revenue primarily from its Retail Banking in France segment, contributing €470.49 million, while Non-Business Activities add €116.72 million.

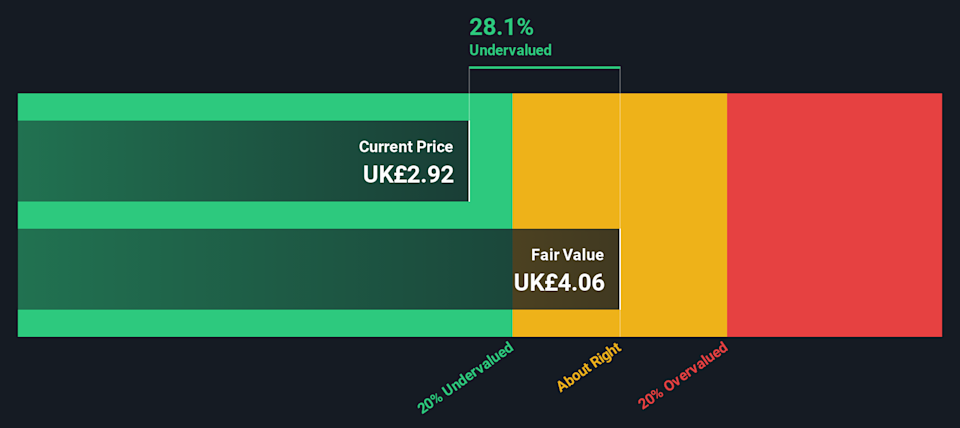

With total assets of €36.3 billion and equity at €6.1 billion, Caisse Régionale de Crédit Agricole Mutuel du Languedoc stands out with its solid financial footing. The cooperative’s allowance for bad loans is robust at 128%, while non-performing loans are kept low at 1.7%. Despite a challenging five-year period with earnings dipping by 2.1% annually, the past year’s performance was strong with a 9.4% growth in earnings, surpassing the industry average of 1%. Its price-to-earnings ratio of 8.2x offers good value compared to the broader French market’s 16.1x benchmark.

ENXTPA:CRLA Debt to Equity as at Apr 2026

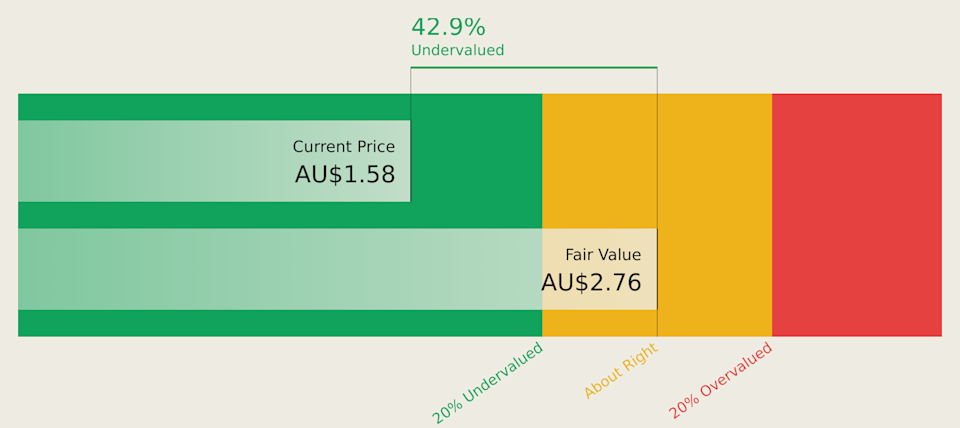

Simply Wall St Value Rating: ★★★★★★

Overview: FM Mattsson AB (publ) is engaged in the development, manufacturing, and sale of water taps and related products for bathrooms and kitchens across various European countries and internationally, with a market capitalization of approximately SEK3.99 billion.

Operations: FM Mattsson generates revenue primarily from the Nordic Countries, contributing SEK1.14 billion, followed by international markets with SEK832.70 million. The company’s financial performance is reflected in its net profit margin trends over recent periods.

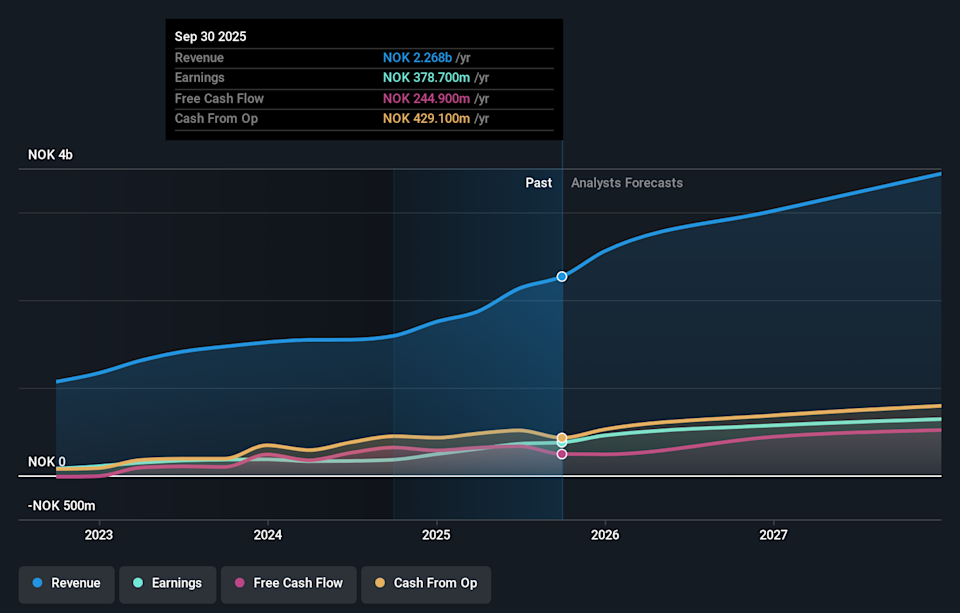

FM Mattsson, a notable player in the European market, has shown impressive earnings growth of 42.3% over the past year, outpacing the Building industry’s -5.3%. With no debt burden and high-quality earnings, it stands on solid financial ground. The company reported sales of SEK 1.97 billion for the full year ending December 2025, up from SEK 1.88 billion previously, and net income rose to SEK 145 million from SEK 101.9 million a year ago. Trading at 3.1% below its estimated fair value suggests potential room for appreciation as revenue is forecasted to grow by approximately 6% annually.

OM:FMM B Debt to Equity as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CPSE:DAB ENXTPA:CRLA and OM:FMM B.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

👋 Good morning! Stocks had an interesting Thursday, opening deep in the red before paring back the losses after news broke about Iran drafting a protocol with Oman to manage ship traffic in the Strait of Hormuz. As managing traffic means there must be traffic to manage, investors grasped that news and cast aside some

The S&P 500 is down almost 9% from its January record high. Ongoing geopolitical tensions in the Middle East have triggered a spike in oil prices, which could stoke inflation for any products requiring transportation by land, air, or sea. As a result, investors are bracing for economic uncertainty and even a potential increase in interest

McCormick & Company, Incorporated (NYSE:MKC) is among the stocks in focus as Jim Cramer highlighted a market yearning for the status quo ante. Cramer discussed the company’s deal with Unilever during the episode, as he commented: Sometimes, a group is just so hated that it doesn’t matter what any of its members do. You know

Uncertainty is a part of life, and it also plays a big role in the stock market. During periods of high uncertainty, investors tend to become anxious, and right now, there is a lot to be nervous about. Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company,

The European stock markets have recently seen a positive shift, with the pan-European STOXX Europe 600 Index rising by 3.92% amid hopes for a shorter-lived Middle East conflict and despite inflationary pressures driven by energy costs. In this environment, growth companies with high insider ownership can be particularly appealing as they often signal strong confidence

The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 index experiencing declines influenced by weak trade data from China and a global economic slowdown. Amid these conditions, identifying undervalued stocks can be crucial for investors seeking opportunities, as such stocks may offer potential value when broader market sentiments are subdued. Name

As European markets navigate the complexities of Middle East tensions and energy market volatility, the pan-European STOXX Europe 600 Index has shown resilience, ending the week with a 3.92% gain. Amidst these broader market dynamics, small-cap stocks in Europe present intriguing opportunities for investors seeking value, particularly when insider activity suggests confidence in a company’s

Buying and holding stocks for the long run is a great strategy for building wealth over time. However, companies change, and some investments that looked solid a few years ago may turn out to be duds if you give them more time to stretch. For instance, Kraft Heinz (KHC +2.33%) used to be a solid

①Global stock markets experienced a roller-coaster ride this week, with Asian markets and U.S. stocks affected by Trump’s remarks. Market sentiment turned pessimistic on Thursday, while oil prices surged significantly; ②Wall Street has adopted risk-averse strategies. Some reduced their growth stock positions to increase value stock holdings, others shifted to foreign exchange trading or hedging

Satellite stocks were hot among investors on Thursday, and one beneficiary of this was telecom services specialist Iridium Communications (IRDM +15.32%). Following a widely read media report about a peer company potentially being acquired, Iridium’s share price zoomed more than 15% higher. That crushed the essentially flat performance of the S&P 500 index. Star turn

Stock price down Sometimes, the stock market hands investors a puzzle. All three of the Straits Times Index’s worst performers for March 2026 reported strong headline results for their latest full year. Profits surged, dividends were raised, and order books looked healthy. Yet their share prices lagged behind the rest of the pack. The common

CoreWeave (CRWV +4.87%) is one of the fastest-growing companies in artificial intelligence (AI). Revenue hit $5.1 billion in 2025 — up 168% year over year — and the company is guiding for more than twice that in 2026. Its backlog swelled more than 300% to $66.8 billion. I see why bulls believe in this one,

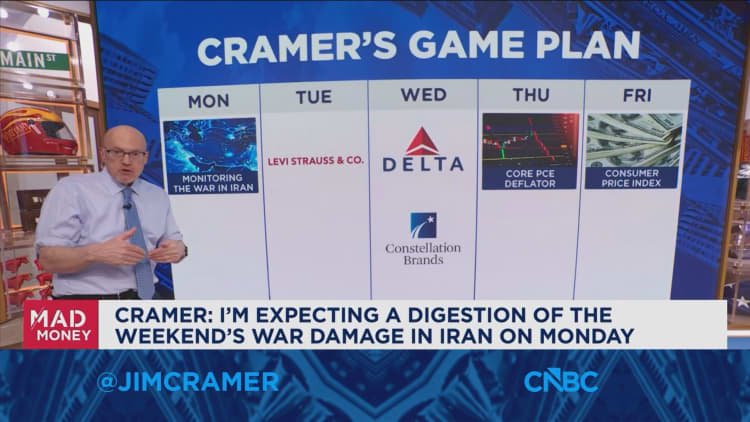

CNBC’s Jim Cramer outlined Thursday what investors should watch in the week ahead, including Middle East developments, major earnings releases and key economic prints. The “Mad Money” host’s weekly game plan follows a volatile session on Wall Street. Stocks ripped higher Thursday on media reports that Iran is working with Oman to draft a protocol

The tech-heavy Nasdaq Composite recently entered correction territory, as defined as a 10% drop from its most recent high. That means it is halfway to bear-market levels. Many investors are staying away from equities right now, given the challenging broader macroeconomic conditions that are partly to blame for the Nasdaq’s decline. However, it might actually

As the Australian stock market shows signs of stabilization with a +0.5% advance, investors are cautiously optimistic about the resolution of geopolitical tensions in the Middle East and its impact on global markets. In this environment, identifying stocks that may be trading below their estimated value can offer potential opportunities for those looking to capitalize

Reddit, Inc. was added to the FTSE All-World Index (USD) on 21 March 2026, bringing the social platform into a widely tracked global equity benchmark. This inclusion can influence how large institutional investors gain exposure to Reddit, potentially affecting trading volumes and the stock’s investor base composition. We’ll now examine how this index inclusion, against

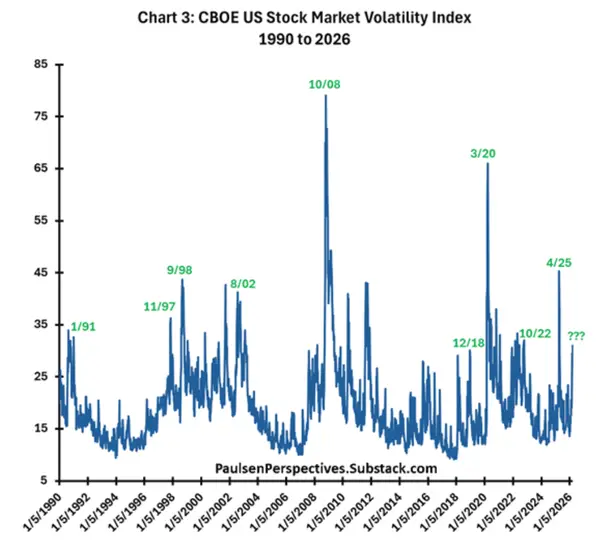

The outlook for stocks hasn’t looked this gloomy in recent memory. But one Wall Street veteran is feeling confident that the bull market isn’t over. Jim Paulsen, current Substack writer and former chief investment strategist at The Leuthold Group, says he’s seeing a handful of signs that suggest the market was on its way to

Over half (55%) of investors surveyed believe artificial intelligence (AI) will have a positive impact on the stock market over the next 10 years, according to recent research by The Motley Fool. But opinions vary widely by age. Surprisingly, it’s millennials, not Gen Z, who are most bullish about AI. Nearly three-quarters (73%) expect a

Image source: Getty Images Is a stock market crash inevitable this year? Some are suggesting as much. The FTSE 100 and S&P 500 have both already dipped into (and then out of) the territory of a stock market correction. The Iran war could drag on and on, with all the effects on inflation and supply