Morgan Stanley strategists stated that robust earnings from U.S. companies, led by a thriving technology sector, are overshadowing concerns that conflicts in the Middle East could weigh on the stock market.

According to Zhitong Finance APP, Morgan Stanley strategists stated that robust earnings from U.S. companies led by a thriving technology sector are overshadowing concerns that conflicts in the Middle East could weigh on the stock market. In a report, the Morgan Stanley strategy team led by Michael Wilson wrote that the Q1 earnings season delivered strong results, with the median earnings per share of S&P 500 companies exceeding market expectations by 6%, marking the strongest performance in four years. Meanwhile, earnings forecasts for the S&P 500 across multiple time horizons have been revised upward over the past month—Q2 earnings expectations rose by 2%, while full-year 2026 and next 12-month earnings expectations increased by 3% and 4%, respectively.

Wilson noted that cloud computing giants and semiconductor companies were ‘the primary contributors to resilient corporate earnings growth’ as they benefited from accelerated cloud demand and solid order backlogs. However, the earnings growth was not limited to these sectors, as ‘upward revisions in earnings expectations for financials, industrials, and consumer cyclicals also expanded, indicating stronger persistence in profit growth expansion.’

Wilson added that the impact of the war in the Middle East is expected to remain uneven rather than systemic, with cost pressures affecting individual companies without dragging down entire industries. He pointed out that energy companies acted as a tailwind for overall earnings, as rising oil prices boosted their profit growth.

Wilson added that the impact of the war in the Middle East is expected to remain uneven rather than systemic, with cost pressures affecting individual companies without dragging down entire industries. He pointed out that energy companies acted as a tailwind for overall earnings, as rising oil prices boosted their profit growth.

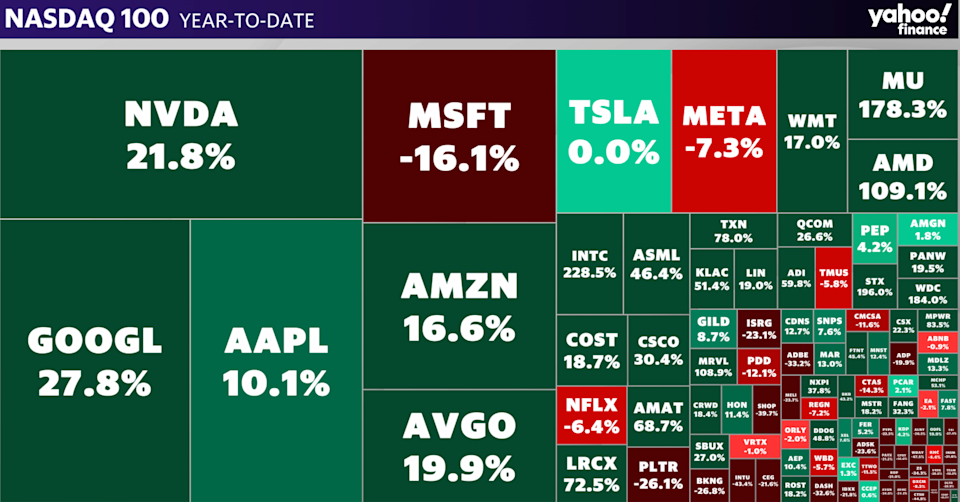

Despite strong corporate earnings resilience and repeated record highs in the U.S. stock market, concentration risk remains a concern for investors. Data shows that seven stocks in the S&P 500 contributed approximately 80% of the index’s returns this year.

However, Goldman Sachs strategists stated that the spending boom on artificial intelligence (AI) infrastructure showed no signs of slowing down, and analysts further raised their expectations for cloud computing giants’ expenditures since the start of the earnings season. The strategists remarked, ‘The surge in spending expectations has driven similar increases in earnings forecasts for AI infrastructure companies, helping improve the overall market’s earnings outlook and tilting our S&P 500 earnings-per-share forecast risk to the upside.’

Against the backdrop of sustained AI demand growth, rising chip and data center costs, four of the ‘Magnificent Seven’ U.S. tech giants that reported earnings last week did not signal plans to cut investments but instead raised capital expenditure forecasts further. Data showed that Microsoft (MSFT.US), Amazon (AMZN.US), Meta (META.US), and Google (GOOGL.US) increased their capital expenditure scale to $725 billion this year—mainly for AI data center equipment—higher than the pre-earnings market expectation of $670 billion.

Middle East Conflicts Take a Backseat as Profit Growth Narrative Returns to Center Stage on Wall Street

Although the geopolitical storm in the Middle East remains unresolved, after an initial wave of sharp sell-offs, investors seem to be filtering out war-related noise. Unlike early March, when the war was considered a ‘core variable determining market direction,’ investors are now largely ‘ignoring the noise of conflict.’

As the U.S. earnings season kicked off in mid-April, strong profit expansion driven by the AI infrastructure boom provided a floor for expectations. Additionally, the market believed that parties involved in the Middle East conflict were likely to reach agreements. Top Wall Street investment institutions, including BlackRock, Goldman Sachs, and Morgan Stanley, became more optimistic about the future outlook for the stock market.

The S&P 500 surged 10.4% in April, marking its best monthly performance since November 2020; the Nasdaq Composite climbed 15.3%, its largest gain since April 2020. Both indices hit new all-time highs last Friday.

Several financial giants on Wall Street directly attribute the current resilience in the stock market to continuously improving corporate earnings expectations, particularly the robust profit outlook for technology companies closely tied to explosive demand for AI computing infrastructure, which has remained unbroken by the conflict.

Despite overall robust corporate profitability, some investors have expressed concerns about the frenzy of AI spending by tech giants. Doubts about the sustainability of certain software business models are also beginning to emerge, prompting some relatively cautious investors on the theme of AI computing power investment to reassess their portfolios. A ClearBridge Investments portfolio manager stated, ‘The disruptive potential of AI in software, services, finance, and other industries has created uncertainty in the market regarding the durability and ultimate value of certain business models.’

However, in the short term, the recent upward momentum in U.S. stocks is expected to continue, and investors blindly following the old Wall Street adage—’Sell in May and go away’—may end up paying a price. As market expectations lean towards an optimistic path for peace talks between the U.S. and Iran, and strong earnings reports driven by AI computing power outweigh oil prices and geopolitical risks, Wall Street anticipates that the robust rally seen after the strongest monthly gain in years will likely extend into May.

Seasonal factors have not played a role in recent periods. According to CFRA data, dating back to 1945, the S&P 500 Index’s long-term performance from May to October has been lackluster, with an average increase of 2%—far below the nearly 7% gain seen from November to April. However, this period has performed much stronger over the past decade, with an average increase reaching 7%, including last year’s 22.1% surge.

Ryan Detrick, Chief Market Strategist at Carson Group, stated, ‘You really hate to say ignore the saying ‘Sell in May and go away’… but over the past decade, it simply hasn’t worked.’ Referring to the market performance of the past ten years, he said, ‘If investors had blindly sold in May and shifted to cash or even defensive allocations, they would have significantly hurt themselves.’

A senior strategist noted that several factors this year paint a more optimistic picture for the stock market, suggesting that being overly bearish based solely on calendar-related factors is unwarranted. With concerns over a large-scale escalation of the U.S.-Iran conflict easing, equities have strongly rebounded from a sharp sell-off. Strong corporate earnings have supported market sentiment, while the U.S. economy has shown resilience amid the energy shock triggered by the Iran war. Jim Carroll, Portfolio Manager at Ballast Rock Private Wealth, remarked, ‘If there’s any year you might want to throw seasonality out the window, it could very well be this one.’