Global markets have recently shown resilience, with U.S. equity markets rallying on the back of strong corporate earnings and a robust labor market, while European indices experienced modest gains amid easing geopolitical tensions. Despite these positive trends, certain stocks remain undervalued relative to their intrinsic value estimates, presenting potential opportunities for investors who focus on fundamentals and long-term growth prospects.

Top 10 Undervalued Stocks Based On Cash Flows

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

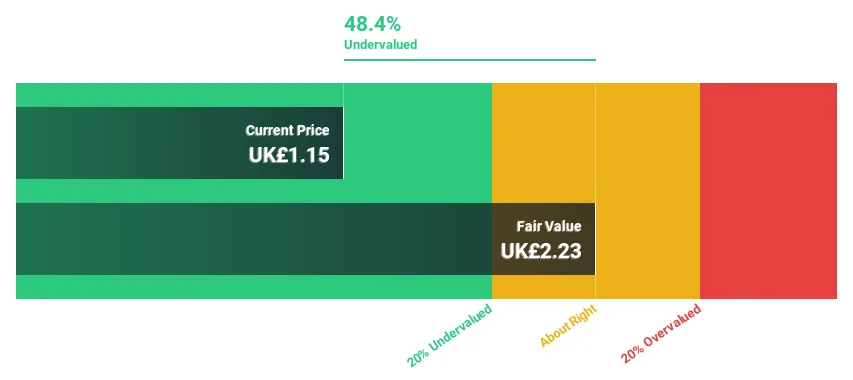

Yurtec (TSE:1934) |

¥2509.00 |

¥4947.89 |

49.3% |

|

Tfe (KOSDAQ:A425420) |

₩61600.00 |

₩119675.15 |

48.5% |

|

Sicily by Car (BIT:SBC) |

€3.14 |

€6.26 |

49.8% |

|

Shenzhen Dynanonic (SZSE:300769) |

CN¥78.60 |

CN¥155.98 |

49.6% |

|

Sanoma Oyj (HLSE:SANOMA) |

€8.88 |

€17.75 |

50% |

|

Metriks AI. Società Benefit (BIT:MTK) |

€3.62 |

€7.13 |

49.3% |

|

Enea (OM:ENEA) |

SEK77.40 |

SEK153.22 |

49.5% |

|

Coloplast (CPSE:COLO B) |

DKK407.10 |

DKK807.65 |

49.6% |

|

B&S Group (ENXTAM:BSGR) |

€5.85 |

€11.66 |

49.8% |

|

AlbaLinkLtd (TSE:5537) |

¥2077.00 |

¥4116.19 |

49.5% |

Let’s take a closer look at a couple of our picks from the screened companies.

Overview: APT Medical Inc. focuses on the research, development, production, and sale of cardiovascular interventional medical devices in China with a market cap of CN¥33.13 billion.

Operations: The company generates revenue of CN¥2.72 billion from its medical products segment.

Estimated Discount To Fair Value: 31.5%

APT Medical appears undervalued, trading 31.5% below its estimated fair value and significantly under its future cash flow value. Recent earnings show strong growth with Q1 net income at CNY 229.44 million, up from CNY 183.15 million the previous year. The company has initiated a share buyback program worth up to CNY 100 million, indicating confidence in its financial health and potential for sustained profitability despite an unstable dividend track record.

Overview: LianChuang Electronic Technology Co., Ltd specializes in the research, development, production, and sale of optics and optoelectronics both in China and internationally, with a market cap of CN¥9.06 billion.

Operations: The company generates revenue from its optics and optoelectronics segments, serving both domestic and international markets.

Estimated Discount To Fair Value: 49%