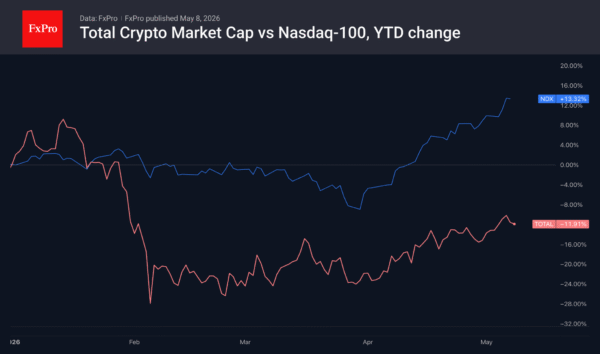

- Equities maintain a “risk-on” rally, defying the market disconnect from elevated oil prices and rising interest rate expectations.

- The US market faces a pivotal week with the final Powell-led CPI report expected on Tuesday, ahead of the Fed Chair handover to Kevin Warsh on May 15.

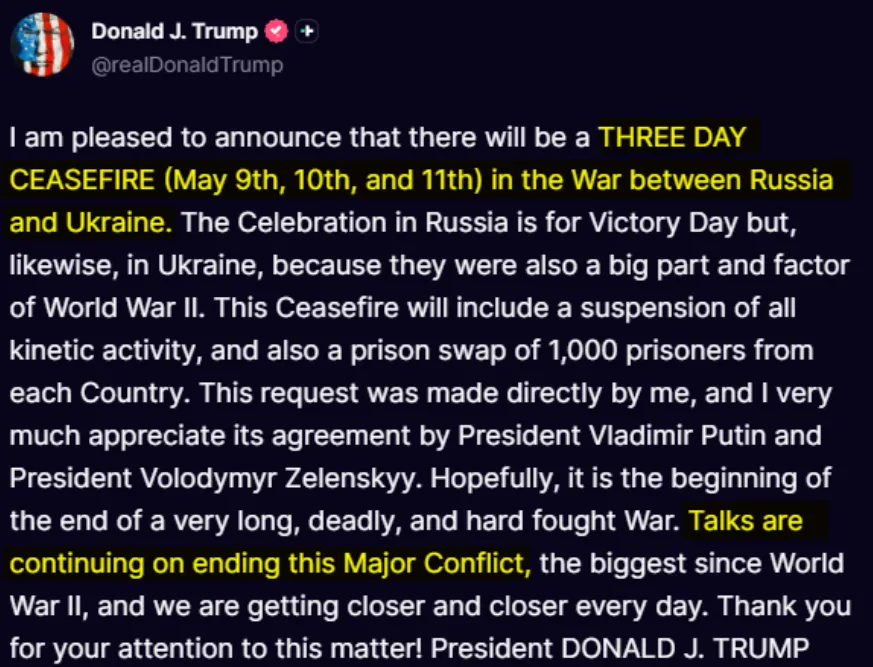

- Geopolitical tensions remain high following US/Iran strikes, though a 3-day Russia-Ukraine ceasefire was announced.

- The US Dollar Index (DXY) is showing a bearish technical breakdown, with a cooler CPI likely to lead to a move toward the 96.901 support level.

Week in Review: Equities Defy Gravity as Oil and Rates Realign

The start of May has left market participants with more questions than answers. In a striking display of resilience or perhaps denial, US stock markets have surged to fresh highs, seemingly shrugging off the geopolitical tensions that briefly rattled indices mid-war.

However, this “risk-on” euphoria sits in uncomfortable contrast with the reality of the energy market. Oil prices have refused to retreat to pre-conflict levels, and interest rate expectations are being recalibrated higher across the board.

The disconnect is clear: can equities continue to climb while the cost of capital and energy remain elevated?

Geopolitical Developments

Markets continue to hang on every word of US President Donald Trump and the ongoing situation in the Middle East. Markets are rightly on edge heading into the weekend given the tit-for-tat strikes between Iran and the US on Thursday and Friday, May 7 and 8 respectively. Any significant developments over the weekend could drive early week volatility and price action.

Late on Friday, President Trump announced a 3 day ceasefire between Russia-Ukraine for the 9th, 10th and 11th of May.

Source: TruthSocial

Week Ahead: Central Bank Divergence and Inflation Storms Loom Large

As we look toward the week starting May 10, the focus remains on geopolitical nut markets, which are also debating whether central banks will follow the market’s hawkish lead or if a reality check is overdue.

This makes for interesting viewing and will likely lead to significant market movement.

US: The Fed’s Final Changing of the Guard

The coming week is a momentous one for the Federal Reserve. Not only do we face critical data points, but we also mark a transition in leadership. Jerome Powell is set to conclude his tenure as Fed Chair, with Kevin Warsh scheduled to take the reins on Friday, May 15.

On the data front, Tuesday’s Inflation report is the headliner. We are bracing for a second consecutive 0.9% MoM print at the headline level, largely fueled by the surge in gasoline and diesel prices. While the core reading is expected at a more modest 0.3%, the annual rate could push up to 2.7%. The Fed has recently made a concerted effort to talk up rate expectations, ditching their previous easing bias as the US economy continues to hold up better than its peers. However, with labor supply growth effectively stalled due to collapsing net migration (projected at near zero this year), the “hot” jobs numbers we’ve seen may be less a sign of strength and more a symptom of a tightening supply constraint.

UK & Europe: A Strange Case of Mispricing

Across the Atlantic, the Bank of England (BoE) and the European Central Bank (ECB) find themselves in different boats, though markets are currently pricing them as if they are in the same storm.

Markets are pricing in a significantly more hawkish path for the UK than the Eurozone—a move that looks overdone. While the UK is energy-dependent, this is not a repeat of the 2022 gas crisis; natural gas prices remain relatively contained compared to the spike in oil. We believe the ECB is actually more likely to deliver on its hawkish rhetoric in June, whereas the BoE may view “not cutting” as enough tightening for now. Watch the Euro and Sterling closely as this pricing discrepancy begins to unwind.

Asia: Inflation Fallout and Trade Tensions

In Asia, the focus is squarely on the fallout from the Middle East through the lens of inflation.

- China: We are looking for trade data on Saturday and inflation data on Monday. Exports are expected to grow by roughly 6.5%, but the real story lies in the PPI, which is accelerating. Markets will be hyper-sensitive to how China handles the impact of higher energy costs and the lingering effects of the “Liberation Day” tariffs.

India: Expect a modest rise in inflation. While gasoline prices remain capped by the government, the second-round effects of oil prices are starting to bleed into food costs, which could test the Reserve Bank of India’s patience.

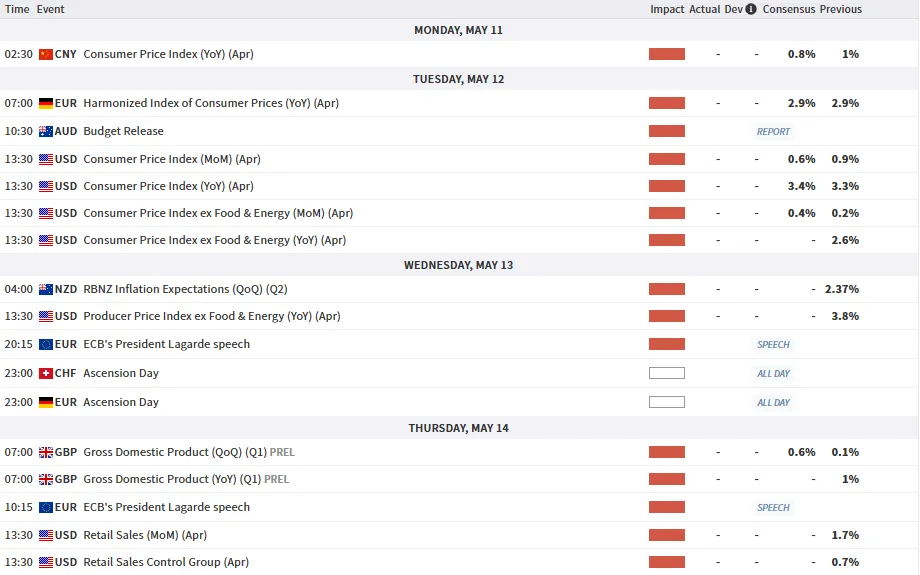

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week – US Dollar Index (DXY)

The US Dollar Index (DXY) finds itself in a precarious position as we head into a pivotal week. Between the transition in Fed leadership and a looming inflation print, the technicals are flashing signs of exhaustion, suggesting the “Dollar King” crown might be slipping.

On the daily timeframe, the indexes break below its ascending channel, signaling a shift in momentum remains intact.

We are currently seeing the DXY trade below key Moving Averages:

The 50-day MA (Yellow) at 98.459 and the 200-day MA (Purple) at 98.538 have converged, effectively acting as a “ceiling” for recent price action.

The fact that price is struggling to reclaim these MAs suggests that the path of least resistance remains to the downside in the near term.

Support Watch: The immediate floor sits at 97.702. A daily close below this level would confirm the Double Top and likely open the trapdoor for a deeper correction toward the 96.901 handle.

Scenarios for the Week Ahead

Given the fundamental backdrop of the final Powell-led CPI print and the handover to Kevin Warsh, I see two primary technical paths:

Scenario 1: The Bearish Confirmation (High Probability)

If Tuesday’s US CPI data comes in cooler than expected—or even just meets estimates—the DXY is likely to break the 97.702 support. This would confirm the Daily Double Top and trigger a move toward 96.901. In this scenario, the convergence of the 50 and 200 SMAs on the daily will remain the ultimate barrier, cementing a medium-term bearish outlook.

Scenario 2: The “Sticky Inflation” Spike (Low Probability)

Should we get a significant beat in inflation (above the 0.9% MoM forecast), we could see a knee-jerk spike in the Dollar. The bulls would need to reclaim and hold above 98.729 on a daily closing basis to invalidate the bearish setup. However, even with a spike, the psychological resistance at 100.00 remains a massive hurdle that would likely attract heavy selling.

US Dollar Index (DXY) Daily Chart, May 8, 2026

Source:TradingView.Com (click to enlarge)

The market is currently betting on a “perfect landing” where growth stays firm despite rising rates. However, with the energy channel remaining hot and central banks diverging, the margin for error is becoming razor-thin. Stay disciplined and watch those support levels.