Why the 60/40 portfolio is crushing it — despite market chaos and inflation fears

The 60/40 portfolio brings balance to portfolios — and investors. – Getty Images/iStock

The traditional 60/40 portfolio may not get much respect these days, but it continues to perform.

This is noteworthy because this balanced portfolio has come in for considerable criticism over the past couple of years. It suffered one of its worst years on record in 2022, for example, leading many investors to conclude that there are better ways to reduce portfolio risk than taking 40% of a stock portfolio and investing it in bonds.

Most Read from MarketWatch

Yet the 60/40 portfolio keeps chugging along. While significantly reducing volatility over the 12 months through the end of this year’s first quarter, it still produced a double-digit gain (11.1%, assuming the stock portion was invested in Vanguard Total Stock Market Index ETF VTI and the bond portion in Vanguard Long-Term Treasury Index ETF VGL).

That’s impressive, given that this 12-month period included the nuclear winter of April 2025’s “liberation day” tariffs, last summer’s bombing of Iran, this year’s Iran war outbreak and the near-doubling of oil prices.

Here are three major objections that investors lodge against the 60/40 portfolio — and why they’re misguided:

1. Stock-bond correlations are increasing

Perhaps the most common argument made against the 60/40 portfolio is that the correlation between stocks and bonds has increased dramatically over the past decade. On the surface that seems damning, since as stocks and bonds become more highly correlated, bonds presumably become less effective at reducing volatility.

That’s an incorrect interpretation of the increased correlation, according to Wes Crill, a vice president at Dimensional Fund Advisors. In an interview, he pointed out that the correlation coefficient rises mechanically during periods of heightened volatility — such as what we’ve seen in recent years. But that has little to do with bonds’ diversification potential.

–

A better measure, Crill says, is the ratio of the 60/40 portfolio’s standard deviation to that of an all-stock portfolio. Even though the stock-bond correlation has oscillated widely over the years, this ratio has remained remarkably constant — as you can see from the chart above. In other words, according to Crill, “The proportional reduction in volatility gained through diversification has been largely unrelated to the estimated correlation.”

2. Bonds will perform poorly if inflation worsens

The second major argument lodged against the 60/40 portfolio is that bonds will perform poorly if U.S. inflation worsens. But how do we know inflation will be worse?

Crill argues that it’s important to understand the difference between how bonds react to inflation that is expected (and which therefore is already reflected in bond prices), and their reaction if inflation turns out to deviate from current expectations. If the market currently expects inflation to worsen in coming years, and the market turns out to be right in its expectation, then bonds can still provide a positive real return.

So both investors and financial advisers are guilty of a fundamental confusion when arguing that, because inflation may get worse in coming years, bonds are a poor bet. The inflation threat bonds face isn’t from expected inflation but from unexpected inflation. And by definition unexpected inflation is just that — unexpected.

Crill says there’s no more reason now to avoid the 60/40 portfolio because of concern about what inflation would do to bonds.

3. Better diversification than bonds can be found

The third major argument against bonds in a 60/40 portfolio is that there are superior ways of reducing risk that don’t require forfeiting as much return. Since there are myriad ways of reducing risk besides a 60/40 portfolio, it’s impossible to respond to all of them. But Crill has found from his firm’s research that these alternatives often “add complexity without clear benefit, often increasing fees and reducing transparency while delivering similar underlying exposures.”

As an illustration, Crill pointed to so-called buffered ETFs (also known as defined-outcome or target-outcome ETFs), which provide downside protection in return for forfeiting some of the stock market’s upside potential. One measure of investors’ eagerness to find an alternative to bonds as a portfolio diversifier is the explosive growth in these ETFs’ assets under management— more than $75 billion currently, according to ETF.com, and projected by Cerulli Associates to grow to more than $300 billion by 2030.

–

Despite the considerable hype surrounding these buffered ETFs, Crill has found their risk-reward profile to be substantially similar to the 60/40 portfolio. This is illustrated in the chart above, which plots portfolio return as a function of the S&P 500 SPX. Notice that the risk-reward line for the 60/40 portfolio is almost identical to that of the average buffered ETF. So there’s no reason to deviate from the traditional portfolio that invests 60% in a stock index fund and 40% in a bond index fund.

Bottom line? If it ain’t broke, don’t fix it.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at

In case you missed it, Wall Street history was made a little over one week ago. The benchmark S&P 500 (^GSPC +0.29%) and growth-stock-dominated Nasdaq Composite (^IXIC +0.89%) both soared to record-closing highs on April 24, with the ageless Dow Jones Industrial Average (^DJI 0.31%) one good day away from joining its peers. Wall Street’s

Image source: Getty Images Getting started in the stock market can be daunting. But for a lot of people, it can be a huge financial opportunity. Over the long term, stocks and shares tend to generate better returns than cash and bonds. And this isn’t an accident. What if share prices crash? For a number

Mohamed El-Erian sees a potentially difficult path ahead for US markets and the economy. Loading audio narration… The top economist and former co-CIO at PIMCO said there are challenges facing American exceptionalism — the idea that US markets and the economy will continuously outperform the rest of the world in returns and economic growth. That’s

Gold has gotten a lot of attention over the past year as a safe haven during volatile stock markets. But the other precious metal, silver, has actually been a better investment. Over the past year, the price of silver has increased 126% to roughly $74.42 as of April 23. Thatʻs a better return than Nvidia

Although Clarivate (CLVT 2.79%) published its latest quarterly earnings report late in the week, it set the tone for the five-day stock trading stretch. The company’s performance in the period was strong enough to propel its shares to a more than 18% increase week-to-date as of early Friday afternoon, according to data compiled by S&P

Premium valuations combine enthusiasm about future growth with crowd psychology. Earnings multiples, for instance, expand when investors are willing to pay more for each dollar of expected profit. Today’s market fits these patterns. Currently, the S&P 500 (^GSPC +0.29%) sports a forward price-to-earnings (P/E) ratio of 20.9 — above its five- and 10-year averages of

Today’s Change (7.31%) $1.26 Current Price $18.50 Key Data Points Market Cap $6.5B Day’s Range $18.17 – $19.50 52wk Range $7.66 – $23.93 Volume 33M Avg Vol 18M Gross Margin -1563.88% Riot Platforms (RIOT +7.31%), a Bitcoin mining and data center operator, closed Friday at $18.50, up 7.31%. The stock moved higher after Q1 results,

Today’s Change (3.26%) $8.84 Current Price $280.19 Key Data Points Market Cap $4.0T Day’s Range $278.37 – $287.21 52wk Range $193.25 – $288.62 Volume 4.5M Avg Vol 45M Gross Margin 47.33% Dividend Yield 0.38% Apple (AAPL +3.26%), a consumer electronics and software giant, closed Friday at $280.25, up 3.28%. The stock moved higher after Apple

Mechanical resonance imaging (MRI) equipment specialist Iradimed (IRMD +4.45%) ended the stock trading week in style on Friday. On the back of a well-received quarterly earnings report, investors traded the company’s shares up by more than 4%. That was robust enough to trounce the 0.3% gain of the bellwether S&P 500 index that trading session.

Today’s Change (4.40%) $0.20 Current Price $4.86 Key Data Points Market Cap $1.7B Day’s Range $4.55 – $5.30 52wk Range $3.84 – $6.50 Volume 48M Avg Vol 26M Gross Margin 14.45% JetBlue Airways (JBLU +4.40%), a low-cost airline, closed Friday at $4.86, up 4.40%. The stock moved higher as traders reacted to news that beleaguered

Today’s Change (-18.33%) $-10.13 Current Price $45.13 Key Data Points Market Cap $40B Day’s Range $41.75 – $47.44 52wk Range $41.75 – $150.59 Volume 53M Avg Vol 10M Gross Margin 23.75% Roblox (RBLX 18.33%), an immersive gaming and experiences platform, closed Friday at $45.14, down 18.31%. The stock moved lower after first-quarter results missed expectations,

There are a variety of reasons people invest in the stock market. Beyond near-term benefits like making money from growth stocks and even long-term benefits like passive retirement income, investing in the stock market can help you create generational wealth. In general, stocks you can hold forever and pass on to the next generation are

Monarch Casino & Resort, Inc. (NASDAQ:MCRI) was among Jim Cramer’s stock calls on Mad Money recently as he recapped mega-cap tech earnings. When a caller asked about the stock during the lightning round, Cramer said: You know something… I do not know that casino. I have cooled on many of the casino stocks. I think

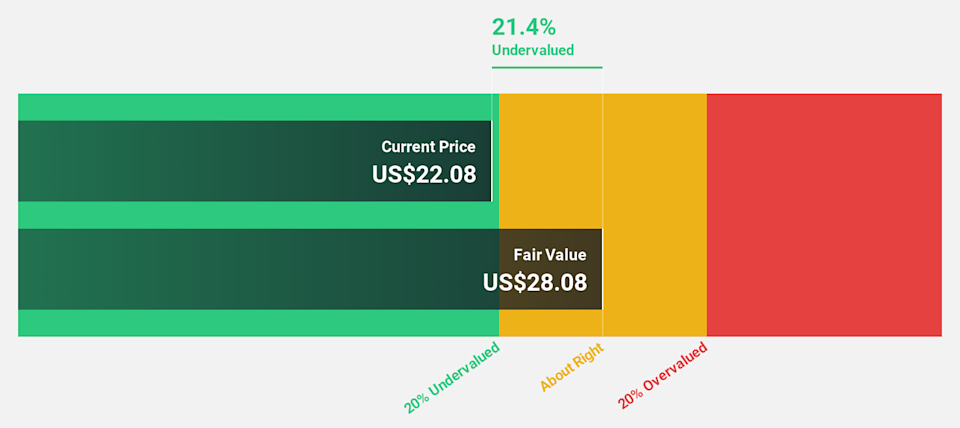

In the last week, the United States market has stayed flat, yet it is up 29% over the past year with earnings forecasted to grow by 16% annually. In such a climate, identifying stocks that are potentially undervalued can present opportunities for investors looking to capitalize on discrepancies between stock prices and their intrinsic values.

Shares of Robinhood Markets (HOOD +2.70%) have fallen 11.8% this week, according to data from S&P Global Market Intelligence. The digital brokerage keeps growing its user base and deposits, but saw a huge decrease in cryptocurrency revenue, which has Wall Street spooked. Here’s why Robinhood stock was falling this week, and whether investors should consider

Year to date, the Nasdaq Composite is outperforming the S&P 500 and the Dow Jones Industrial Average. So you would probably assume that “Magnificent Seven” stocks Nvidia, Alphabet, Apple, Microsoft, Amazon, Meta Platforms, and Tesla would be crushing a stodgy, dividend-paying stalwart like Dow component Coca-Cola (NYSE: KO). Yet, that’s hardly the case. So far this

Even as the S&P 500 continues to set new all-time highs, there are some warning signs emerging. The labor market is showing signs of stagnating, inflation shot much higher in March, and the Iran war is hanging a cloud of uncertainty over everything. Corporate earnings are still likely to show solid growth in the coming quarters,

We are excited to announce that Jonathan Miller, who has long authored the most authoritative report on the residential real estate market, is partnering with The Real Deal. Below, you’ll find his Housing Notes column, which will now run on our site several times a week. In addition, Miller’s quarterly report for New York City, which

📌 Top story — scroll down for more updates Top of the Morning 8:20 am By Alicia AlfiereTeam Rule Breakers Etsy (ETSY 0.75%) stock popped earlier this year on the news that it is selling its second-hand and vintage clothing business, Depop, for $1.2 billion in cash. This could be a good thing for the

Actively managed by PineBridge Investments, the VanEck CLO Opportunities Fund seeks high income and attractive total return through exposure to CLO equity and junior mezzanine debt, building on the success of VanEck’s CLO ETF suite, which includes CLOI for investment grade CLOs and CLOB for mezzanine CLOs. The Fund is an unlisted interval fund with