Middle East Investment Opportunities Featuring 3 Promising Small Caps

As major Gulf markets climb, buoyed by optimism surrounding U.S.-Iran negotiations, investors are increasingly looking towards the Middle East for promising opportunities. In this dynamic environment, identifying small-cap stocks with strong fundamentals and growth potential can offer compelling investment prospects.

Name

Debt To Equity

Revenue Growth

Earnings Growth

Health Rating

Al Wathba National Insurance Company PJSC

10.35%

8.65%

-7.40%

★★★★★★

C. Mer Industries

70.13%

13.00%

68.68%

★★★★★★

Nofoth Food Products

NA

20.62%

23.75%

★★★★★★

Payton Industries

NA

1.92%

13.55%

★★★★★★

Saudi Azm for Communication and Information Technology

Here we highlight a subset of our preferred stocks from the screener.

Simply Wall St Value Rating: ★★★★★★

Overview: Middle East Pharmaceutical Industries Company focuses on the research, development, manufacture, and marketing of generic medicines and pharmaceutical preparations in Saudi Arabia and internationally, with a market cap of SAR2.08 billion.

Operations: The company’s primary revenue streams are derived from private customers, contributing SAR310.04 million, followed by public customers at SAR93.43 million and export customers at SAR57.02 million.

Middle East Pharmaceutical Industries, a promising player in the region, has shown robust financial health with its debt to equity ratio improving from 24.8% to 15.2% over five years and a net debt to equity of just 7%, which is satisfactory. Its earnings growth of 21.5% outpaced the industry average of 8.5%, highlighting its competitive edge. The company’s recent annual report revealed sales reaching SAR 460 million, up from SAR 394 million the previous year, while net income increased to SAR 97 million from SAR 79 million, demonstrating strong profitability and shareholder value enhancement through dividend distributions totaling SAR 26.4 million for late-2025.

SASE:4016 Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bank of Jerusalem Ltd. is a commercial bank offering various banking services in Israel with a market capitalization of ₪1.55 billion.

Operations: The bank’s revenue streams are primarily driven by the Household segment at ₪273.20 million and Housing Loans at ₪212.50 million, with significant contributions from Financial Management activities totaling ₪92.80 million. The Small and Tiny Business segment related to Construction and Real-Estate adds another ₪131.60 million to the revenue mix, while Medium and Large Business in the same sector contributes an additional ₪51 million.

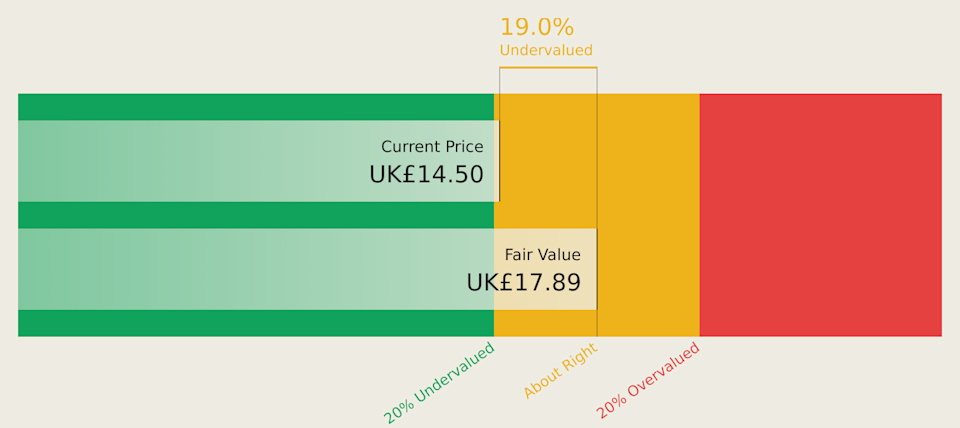

Boasting total assets of ₪23.1 billion and equity of ₪1.6 billion, the Bank of Jerusalem stands out with its robust financial health. Its liabilities are primarily low-risk, with 85% funded by customer deposits, offering a stable foundation compared to external borrowing. Despite insufficient data on bad loan allowances, the bank’s earnings grew impressively by 25.9% over the past year, significantly outpacing the industry average of 4%. Trading at 9.3% below estimated fair value suggests potential for investors seeking undervalued opportunities within this small-cap entity in Israel’s banking sector.

TASE:JBNK Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★★★

Overview: SofWave Medical Ltd. develops, produces, markets, and distributes non-invasive medical technology for skin firming and rejuvenation, tissue renewal, and treatment of muscle aging internationally with a market cap of ₪1.45 billion.

Operations: SofWave Medical generates revenue through the sale of its non-invasive medical technology products across various international markets. The company focuses on controlling costs to optimize its financial performance, with particular attention to maintaining a competitive net profit margin.

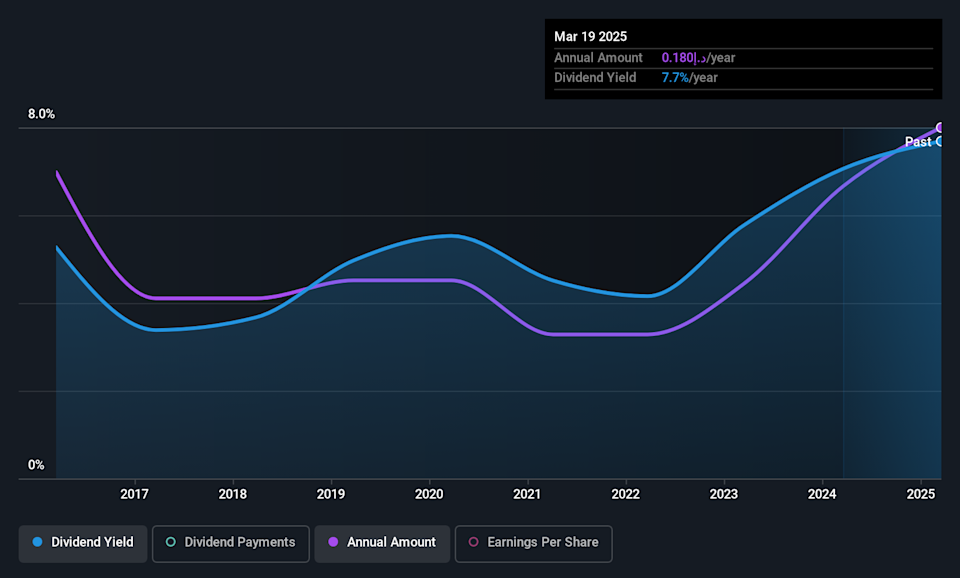

SofWave Medical, a nimble player in the medical equipment industry, has recently turned profitable, marking a significant milestone. The company reported impressive sales of US$87.64 million for 2025, up from US$59.65 million the previous year, and achieved a net income of US$5.49 million compared to a net loss of US$4.55 million earlier. With high-quality earnings and trading at 72.8% below its estimated fair value, SofWave appears undervalued despite its recent success story in profitability and growth outpacing the industry average of 2%. Notably debt-free over five years, it seems poised for further expansion without financial constraints.

TASE:SOFW Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SASE:4016 TASE:JBNK and TASE:SOFW.

The stock market doesn’t move in a straight line. Even during strong bull markets, shorter-term corrections are inevitable. Sentiment turns negative, stocks fall, and even great companies get dragged down with the receding tide. But for long-term investors, those moments are not threats — they are opportunities. The key is preparation. You don’t wait for

The price of silver is down from its January highs. Currently, it’s trading around $79, which is nowhere near even $100, let alone its peak of more than $121. The excitement around the precious metal has largely cooled off in recent months as the market has shown greater stability. The iShares Silver Trust (NYSEMKT: SLV),

Investors don’t normally look to insurance stocks to beat the market. Sure, there are some tech-focused insurance stocks with high-growth potential, but the old insurance giants don’t typically appear on the radar of growth investors. But these value stocks do offer the stability and strength to outlast riskier stocks and beat the market over the

The stock market has never been very predictable. If it were, a lot more people would make a lot more money or lose a lot less. However, some indicators have historically been more reliable than others. And although the stock market and the economy aren’t directly tied together, some market signals have hinted at what’s

Until recently, the stock market appeared unstoppable. The dynamic Dow Jones Industrial Average (^DJI +0.63%), benchmark S&P 500 (^GSPC +1.02%), and artificial intelligence-inspired Nasdaq Composite (^IXIC +1.23%) had all reached record-closing highs since late October. But mounting uncertainties have investors second-guessing the current bull market. Despite a mammoth rally in equities last week, one of

It often feels as if investors are facing massive uncertainty and volatility on all fronts. Whether it’s worries about high valuations of tech stocks, a possible artificial intelligence (AI) bubble, or ongoing energy price shocks and disruptions from the Iran War, many investors are looking for a safe place to land. The past 16 years

South Korean asset managers are rushing to launch new exchange-traded funds tied to both established and emerging space technology companies, seeking to capture investor enthusiasm ahead of SpaceX’s anticipated initial public offering in June. Analysts caution, though, that any rally after the listing may not fully lift the funds if their exposure to SpaceX is

The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 index experiencing a decline due to weak trade data from China, highlighting concerns over global economic recovery. In such an environment, identifying stocks that may be undervalued becomes crucial for investors looking to capitalize on potential opportunities amidst broader market uncertainties. Name

The Middle Eastern stock markets have recently experienced mixed performances, influenced by geopolitical tensions such as the failed U.S.-Iran peace talks and subsequent maritime blockade. Despite these challenges, opportunities for investors remain, particularly in dividend stocks that can offer attractive yields even amidst market volatility. Name Dividend Yield Dividend Rating Yeni Gimat Gayrimenkul Yatirim Ortakligi

Palantir (NASDAQ: PLTR) stock posted significant gains in Monday’s trading. The tech specialist’s share price ended the day’s trading up 3.3%. The S&P 500 index’s level climbed 1% in the same daily session and the Nasdaq Composite index’s level closed out the day’s trading up 1.2%. The artificial intelligence (AI) software company’s share price had

On a day when President Trump announced a blockade of the Strait of Hormuz in response to failed negotiations for a peace agreement, stocks surprisingly charged higher with the S&P 500 (SNPINDEX: ^GSPC) gaining 1%. Investors seemed to shake off the threat around the blockade and the ongoing saber-rattling between the two countries, and stocks

A cargo ship is loading and unloading foreign trade containers at Qingdao Port in Qingdao City, Shandong Province, China on July 28, 2025. CFOTO | Future Publishing | Getty Images Asia-Pacific markets opened higher Tuesday, amid hopes that a deal between Washington and Tehran was still possible even as the U.S. blockades Iranian shipments in

CNBC’s Jim Cramer said Monday that Wall Street’s resilience in the face of escalating geopolitical tensions shows investors are focusing less on the Iran war itself and more on a key driver of stock valuations: interest rates. “I think I’ve been negligent in bringing up the power of low rates, because it’s the reason the

Traders work on the floor of the New York Stock Exchange (NYSE) before the closing bell in New York City on April 8, 2026. Charly Triballeau | AFP | Getty Images Futures tied to the S&P 500 were near flat on Monday night, following a strong session in which traders shrugged off a breakdown in

Today’s Change (8.06%) $8.22 Current Price $110.22 Key Data Points Market Cap $54B Day’s Range $103.88 – $114.09 52wk Range $33.52 – $187.00 Volume 2.2M Avg Vol 27M Gross Margin 47.77% CoreWeave (CRWV +8.06%), a cloud-based GPU infrastructure provider for AI developers, closed Monday at $110.29, up 8.13%. The stock climbed after a Macquarie upgrade

(Image credit: Getty Images) Stocks hit their session lows early Monday as market participants reacted to news that the U.S. and Iran failed to reach a resolution during high-level talks held over the weekend. All three main indexes were higher by the close, though, with the tech-heavy Nasdaq Composite notching its longest daily win streak

DKosig/iStock via Getty Images “Be careful what you wish for, lest it come true.”—Aesop Why didn’t we do better when value outperformed? For several quarters, we’ve highlighted that market gains have been dominated by momentum and growth. Stocks that were rising kept rising, while laggards fell further behind. This created a historically wide gap in