If you are wondering whether Patterson-UTI Energy is attractively priced at its recent levels, this article walks through what the current share price might mean for you as an investor.

The stock recently closed at US$10.05, with returns of 55.3% year to date and 84.2% over the past year. Shorter term moves show a 5.3% decline over 7 days and a 2.3% decline over 30 days.

Recent coverage has focused on Patterson-UTI Energy’s position in the US energy services space and how market sentiment toward drilling and completion activity is affecting related companies. This context helps frame why the stock has delivered strong 1 year returns alongside more mixed 3 year and 5 year performance figures of a 6.2% decline and 71.1% respectively.

Right now, the company scores a 5 out of 6 on Simply Wall St’s valuation checks. Next up is a closer look at what different valuation approaches say about the share price today and how an even richer view of value comes together at the end of this article.

A Discounted Cash Flow model takes estimates of a company’s future cash flows and discounts them back to today’s dollars. It aims to show what those future streams are worth in today’s terms.

For Patterson-UTI Energy, the latest twelve month free cash flow is about $327.9 million. Analysts provide explicit forecasts out to 2028, where free cash flow is projected at $411.0 million. Beyond that, Simply Wall St extrapolates cash flows out to 2035 using the 2 Stage Free Cash Flow to Equity approach, with all figures kept in dollars.

Adding these discounted cash flows together produces an estimated intrinsic value of about $25.66 per share. Compared with the recent share price of $10.05, the DCF output suggests the stock trades at a 60.8% discount to this intrinsic estimate. This indicates a materially undervalued price based on these cash flow assumptions.

For companies where earnings can be uneven, the P/S ratio is often a useful yardstick because it compares the share price with the revenue the business is already generating, rather than profits that can swing with one off items or accounting choices.

Investors usually accept a higher or lower P/S depending on what they expect for future growth and how risky they believe those cash flows are. Faster expected growth or lower perceived risk can justify a higher “normal” multiple, while slower growth or higher risk usually points to a lower one.

Patterson-UTI Energy currently trades on a P/S of 0.79x, compared with the Energy Services industry average of 1.32x and a peer group average of 1.92x. Simply Wall St’s Fair Ratio for Patterson-UTI Energy is 0.86x, which is its view of what a suitable P/S might be after factoring in elements such as earnings growth, profit margins, industry, market value and key risks.

This Fair Ratio aims to be more tailored than a simple peer or industry comparison because it adjusts for the company’s own profile rather than assuming all Energy Services stocks should trade on similar multiples. With the actual P/S at 0.79x versus a Fair Ratio of 0.86x, the shares screen as moderately undervalued on this measure.

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives bring your view of Patterson-UTI Energy together in one place by letting you write a simple story about the business, link that story to a financial forecast for revenue, earnings and margins, and then see the fair value that falls out of those assumptions.

On Simply Wall St’s Community page, Narratives are an easy tool that many investors already use, so you can quickly compare your own fair value with others, see how that stacks up against the current share price, and use the gap between Fair Value and Price to help inform whether Patterson-UTI Energy looks more like a buy, a hold, or a sell for your situation.

Because Narratives are refreshed when new information such as earnings, news or updated analyst targets comes through, you can watch how more optimistic Patterson-UTI Energy views that point to fair values around US$11.00 sit alongside more cautious views closer to US$6.25 to US$7.00, and decide which story best matches your expectations and risk tolerance.

For Patterson-UTI Energy, however, we will make it really easy for you with previews of two leading Patterson-UTI Energy Narratives:

🐂 Patterson-UTI Energy Bull Case

Fair value in this bullish narrative: US$11.00 per share

Implied undervaluation versus the recent US$10.05 price: about 8.6%

Revenue growth assumption: 5.37% annual decline

Assumes earnings recover from a current loss position to US$150.5 million by around 2029, helped by margin gains from automation, digital platforms and natural gas powered equipment.

Builds in the view that acquisitions like NexTier and Ulterra, plus disciplined capital allocation, support higher earnings, industry consolidation opportunities and expanded international exposure.

Recognises risks from the transition to renewable energy, regulatory pressure, high ongoing capital needs, customer concentration and integration challenges that could constrain long term profitability.

🐻 Patterson-UTI Energy Bear Case

Fair value in this more cautious narrative: about US$8.84 per share

Implied overvaluation versus the recent US$10.05 price: about 13.7%

Revenue growth assumption: very large annual decline, driven by the modelled rate of about 60%

Frames Patterson-UTI Energy around an analyst consensus style view where revenue contracts, profit margins are lower and a higher future P/E multiple around 27.9x does a lot of work in the fair value.

Highlights that softer drilling and completion activity, high capital requirements and rising competition in advanced technology could limit how much pricing power and margin improvement the company can sustain.

Flags customer concentration, energy transition headwinds and regulatory pressure as structural risks that could reduce the size of the addressable market and weigh on long term earnings potential.

Both narratives use reasonable building blocks, but they land in very different places on fair value and future cash generation. The key for you is to decide which assumptions on revenue, margins, capital spend and risk feel closer to how you think Patterson-UTI Energy may perform, then see how that lines up against today’s share price and your own time horizon and risk tolerance.

To go deeper into these storylines, compare the detailed assumptions, and see how other investors are framing their expectations, it is worth reviewing the full set of community views on Patterson-UTI Energy through See what the community is saying about Patterson-UTI Energy

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Usually, the playbook for when an asset drops 46% from its peak is to stop buying it. Strategy (MSTR 0.17%) — formerly known as MicroStrategy — missed that memo, and the company now holds 766,970 Bitcoin (BTC 2.64%) after purchasing another 4,871 BTC in the first week of April alone, despite the cryptocurrency’s price of $68,536

The first quarter of 2026 has been rough on artificial intelligence (AI) stocks … or has it? On the one hand, share prices of some of the biggest AI stocks, after years of explosive growth, are actually down so far this year. Nvidia (NVDA +2.59%), for example, is down nearly 5% year to date. Today’s

For most of President Donald Trump’s tenure in the White House, the stock market has excelled. The widely followed Dow Jones Industrial Average (^DJI 0.56%), benchmark S&P 500 (^GSPC 0.11%), and technology-dominated Nasdaq Composite (^IXIC +0.35%) surged 57%, 70%, and 142%, respectively, during his first term, and were all up by double digits through year

With tens of millions of funded accounts, Robinhood is one of the most popular online brokerages for retail investors. Each month, the company posts the top 10 most-owned stocks on the platform. This list is updated monthly and usually includes large tech and artificial intelligence stocks found in the “Magnificent Seven.” Due to the sell-off

In recent days, Willdan Group has come under scrutiny as new analysis suggested its shares are trading above intrinsic value, alongside reports that insiders sold about US$500,000 of stock over the past three months. This combination of perceived overvaluation and insider selling adds a layer of caution to an otherwise solid operational picture, raising fresh

I feel like it’s time for a confession, so here it is: Not every stock that I love is a winner right now. But I tend to fall hard for companies that I know are solid and will rebound when the time is right. Case in point: During the COVID-19 pandemic, travel restrictions meant nobody

President Trump watches the stock market. If you want proof, all you have to do is look through his social media posts. Or you can watch his 2026 State of the Union message, where he proclaimed, “The stock market is at 53 all-time record highs since the election.” The president has seemed in the past

From the attention they received after President Donald Trump issued executive orders to secure the nation’s supply of critical minerals to the interest that rare-earth stocks like MP Materials (MP +2.49%) and USA Rare Earth (USAR 3.41%) received after the government announced equity investments in them, it’s clear that rare-earth stocks are having their day

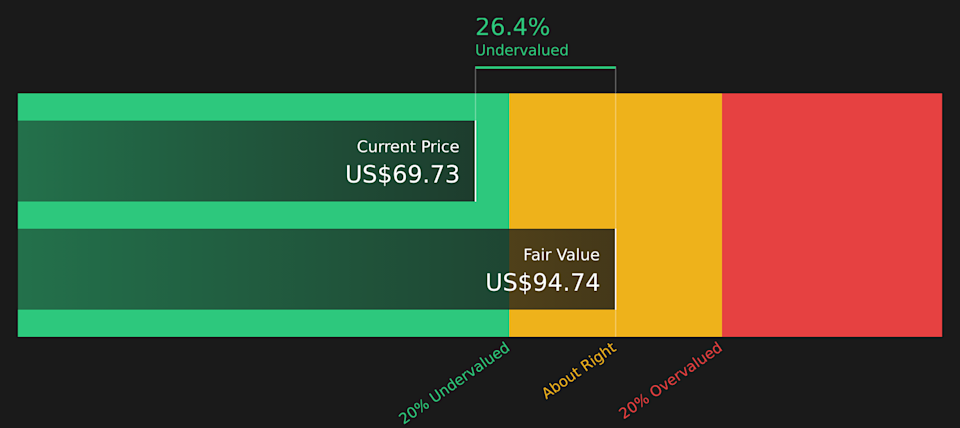

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide. If you are wondering whether Archer-Daniels-Midland (ADM) is still offering value at today’s levels, this breakdown will help you see what the current share price really reflects. The stock last closed at US$69.73, with

A Palantir sign displayed on an office building by Poetra_RH via Shutterstock Retail trader darling and AI-led data analytics company Palantir’s (PLTR) stock should have been an expected beneficiary of the U.S./Israel and Iran war in the Middle East. Thanks to its advanced suite of products that aid decision-making and its proximity to the U.S.

Despite its volatility and occasional bear markets, the U.S. stock market remains one of the best long-term wealth-creation tools for everyday investors. It represents the potential, growth, and possibilities of the global economy in a way that nothing else really does. What’s interesting is that it often rewards those who do the least with it.

Got story updates? Submit your updates here. › An extreme close-up of the intricate machinery powering the stock market’s complex financial ecosystem, reflecting the technical analysis and data-driven insights that guide investment decisions.Boston Today The article provides an in-depth analysis of the current stock market trends, focusing on the performance of major Indian stock indices

Nvidia (NVDA +2.59%) and Broadcom (AVGO +4.69%) are two of the top AI computing companies to invest in right now. Each of their stocks has done incredibly well over the past few years, with Nvidia up 36% since the start of 2025 and Broadcom up over 50%. Each stock has risen so much over the

The market is, completely understandably, focused on artificial intelligence (AI) hyperscalers to determine whether there’s an AI bubble brewing. Those concerns are magnified by the share price performance of the leading hyperscaler companies in 2026 (see chart). The two that stand out the most are Oracle (NYSE: ORCL) and Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), and

Stock market volatility is the new norm, Goldman Sachs says, and it’s not as simple as markets being upset by geopolitical turmoil like the Iran war. Loading audio narration… The conflict in the Middle East has fueled the recent spike in equity volatility, Goldman says, but the firm’s macro strategy research team sees an ongoing

Dow Inc. (NYSE:DOW) is among the stocks Jim Cramer reviewed while discussing the Iran ceasefire that triggered a relief rally. Cramer explained why stocks like Dow are benefiting, as he commented: LyondellBasell and Dow, commodity chemical makers, they’re benefiting from the man-made petrochemical shortage caused by the war… you know what? I’m not so sure

Nvidia (NVDA +2.59%) remains the leader in the artificial intelligence (AI) industry thanks to its market-leading advanced chips that are ideal for training AI models, as well as its CUDA software platform that unlocks the power of its chips and makes it hard for competitors to lure developers away, which has given Nvidia a competitive

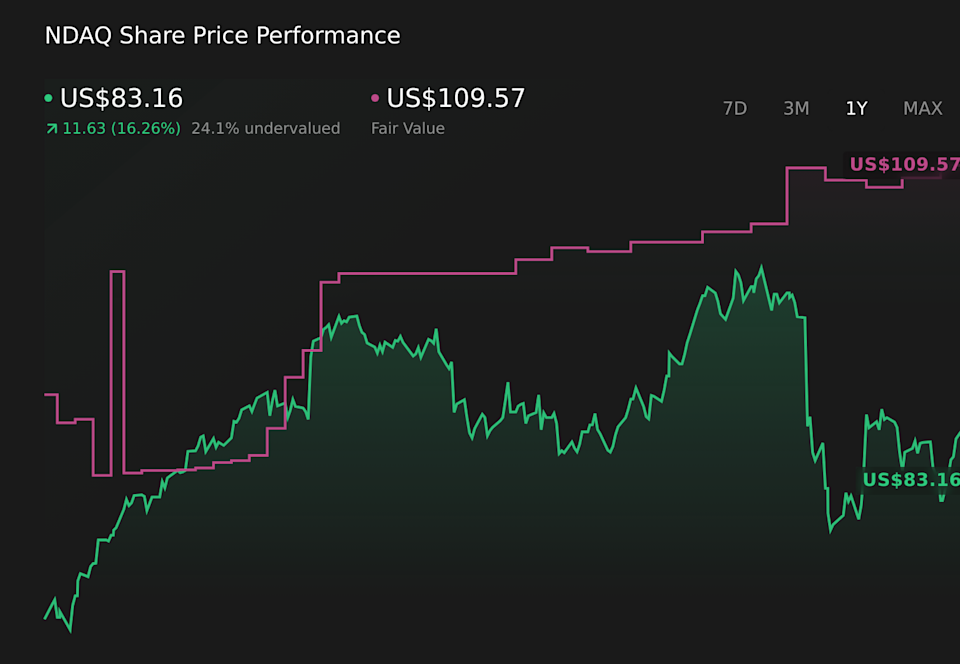

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE. Nasdaq’s latest fair value estimate has been nudged from US$109.57 to US$106.87, a shift of about US$3 per share that signals a more finely tuned

Bread Financial Holdings, Inc. (NYSE:BFH) is among the stocks Jim Cramer reviewed while discussing the Iran ceasefire that triggered a relief rally. Cramer said that the company has a “real niche,” as he stated: There’s a real business here. This company is the financing engine behind a lot of branded credit card programs that consumers

Every share of the SPDR S&P 500 ETF Trust (NYSEMKT: SPY) you own, and every Treasury bond in your retirement account, exist inside a market that foreign investors have filled with more than $35 trillion in capital. That figure, from the U.S. Treasury’s most recent annual survey published in June 2025, is up from roughly