-

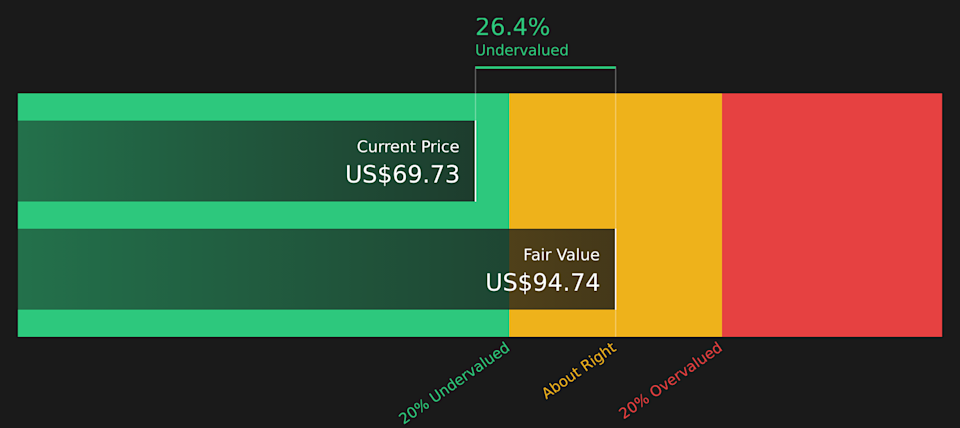

In recent days, Willdan Group has come under scrutiny as new analysis suggested its shares are trading above intrinsic value, alongside reports that insiders sold about US$500,000 of stock over the past three months.

-

This combination of perceived overvaluation and insider selling adds a layer of caution to an otherwise solid operational picture, raising fresh questions about how much optimism is already reflected in the current valuation.

-

Next, we’ll examine how concerns about overvaluation and insider selling might reshape Willdan Group’s investment narrative and risk profile.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

To own Willdan Group, you generally need to believe in sustained demand for energy efficiency and grid modernization work with multi year contracts underpinning revenue visibility. The recent concerns about overvaluation and roughly US$500,000 of insider selling do not appear to alter the near term catalyst of executing a growing backlog, but they may sharpen focus on valuation risk and the possibility of a price correction if expectations tighten.

One recent development that matters here is the initiation of coverage by Wedbush with a buy rating and a US$110 price target, coming shortly before the stock was flagged as trading well above intrinsic value. That contrast between a supportive analyst view and fresh overvaluation concerns could influence how you weigh the upside from new contracts and acquisitions against the risk that the market has already priced in a lot of good news.

Yet even with strong contract momentum, investors should be aware that insider selling and questions about intrinsic value could interact with Willdan’s reliance on policy driven energy projects…

Read the full narrative on Willdan Group (it’s free!)

Willdan Group’s narrative projects $867.2 million revenue and $76.9 million earnings by 2028.

Uncover how Willdan Group’s forecasts yield a $145.00 fair value, a 85% upside to its current price.

Some of the lowest estimate analysts were already more cautious, assuming revenue of about US$874.0 million and earnings near US$82.2 million by 2028, and your view on whether automation erodes Willdan’s consulting edge or reinforces demand for its expertise will shape how you interpret the recent insider selling and overvaluation flags compared with these more pessimistic expectations.

Explore 5 other fair value estimates on Willdan Group – why the stock might be worth as much as 85% more than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include WLDN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com