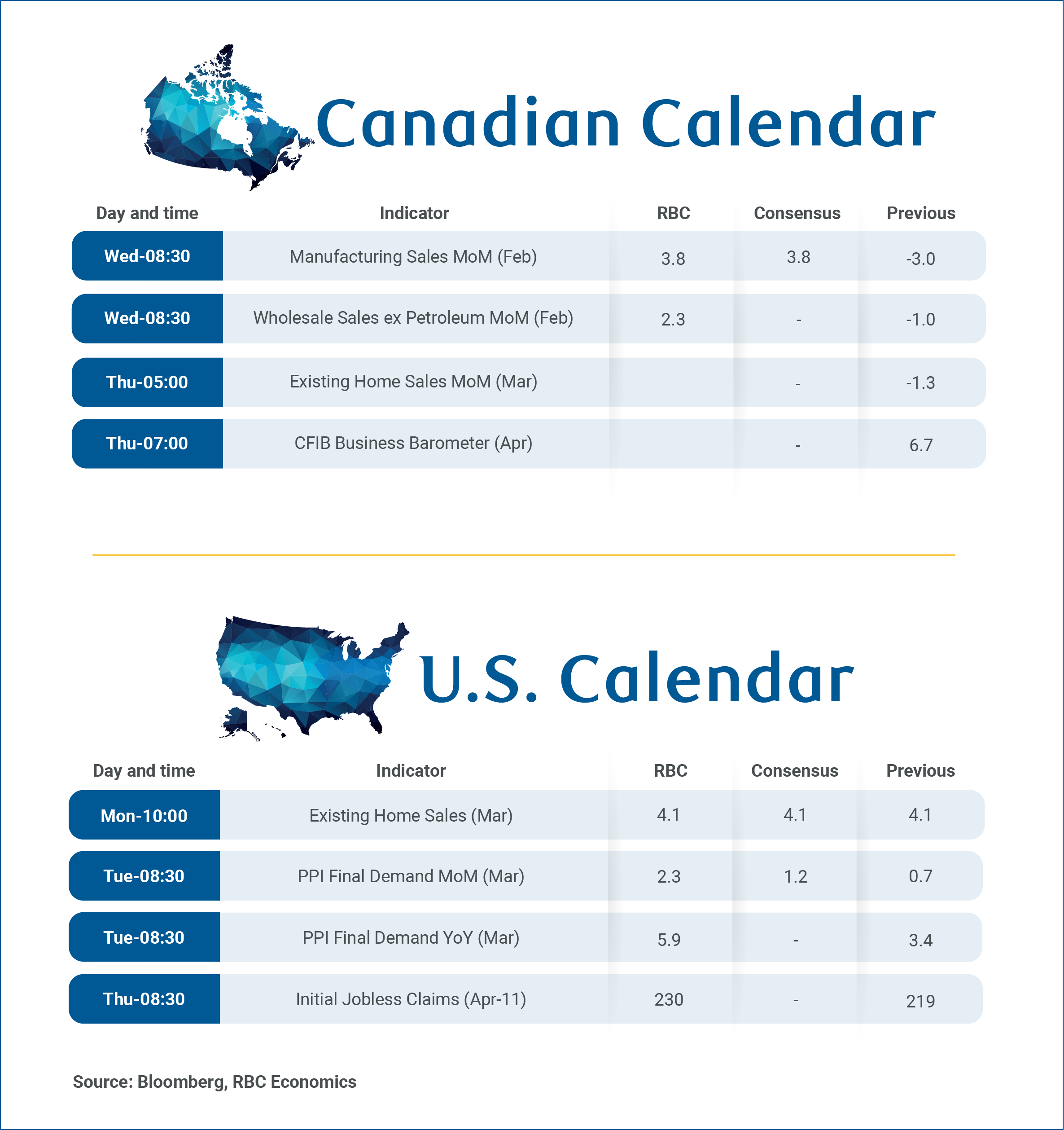

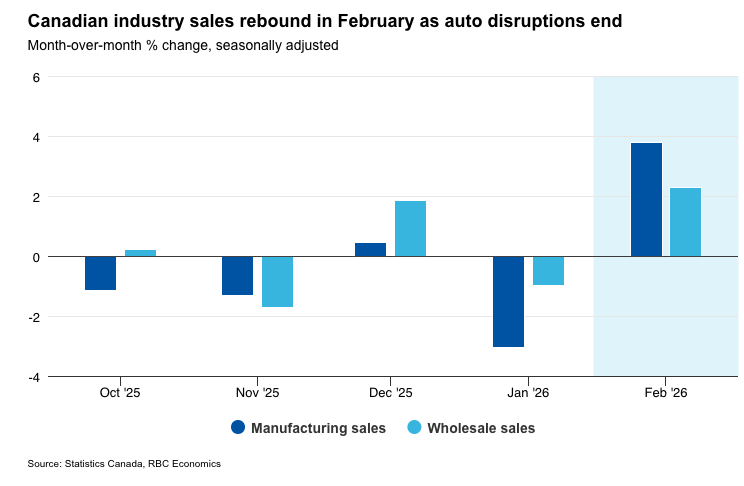

It’s a relatively quiet week for Canadian data releases with attention focused on February’s manufacturing and wholesale trade reports on Wednesday.

Advance estimates from Statistics Canada pointed to rebounds in both wholesale sales (excluding petroleum and agricultural products) up 2.3%, while manufacturing sales jumped 3.8% in February, supported by higher sales in the transportation subsector and manufactured food products.

Both releases are consistent with earlier reports that disruptions to auto production late last year and early 2026 were temporary. Earlier disruptions were tied to semiconductor shortages at some plants, and the latest disruptions in January due to longer-than-usual winter retooling to produce new models at some plants.

The anticipated rebound in manufacturing and wholesales points to firmer goods sector momentum heading into February, following a softer start to the year. Together with earlier data, these releases reinforce the view that underlying economic activity is gradually improving after a modest gain in January.

Housing’s slow start to the spring

On the services side of the economy, home resales remains under pressure with mixed early market reports for March following four straight declines in resales nationally since October 2025.

Early reports showed higher sales in some markets (including Toronto), but declines continued in Vancouver. Home prices also continued to edge lower in British Columbia, Alberta, and Ontario, but rose in Quebec, parts of the Prairies, and Atlantic Canada.

Overall, real gross domestic product edged up by 0.1% in January with early estimates pointing to continued expansion in February, supporting a pickup in growth through Q1.

On balance, current data are tracking broadly in line with our base case forecast for moderate Q1 growth with momentum building, despite ongoing sector-specific volatility.