1 Brilliant Growth Stock to Buy Before It Joins Nvidia in the $4 Trillion Club

While the number can change from day to day, there are currently 12 companies with a market cap of $1 trillion or more, but only one is a member of the prestigious $4 trillion club: Nvidia. The company supplies the graphics processing units (GPUs) that kick-started the artificial intelligence (AI) revolution, but some investors are looking ahead to see what comes next.

The stock market has pulled back thanks to geopolitical uncertainty, and some are wary of big tech’s spending plans, but I remain convinced that Amazon(NASDAQ: AMZN) is poised to join Nvidia in this prestigious club in the years to come.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Macroeconomic fears aside, Amazon has laid a solid foundation for growth that will serve the company — and investors — well for years to come. Given its multipronged growth strategy, I would submit that Amazon will join the $4 trillion fraternity sooner rather than later.

Image source: Getty Images.

Soccer fans will no doubt be familiar with the term hat trick, which is when a player scores three goals in a single game. Likewise, Amazon has scored three successful major business units that are among the strongest in their respective industries. Furthermore, these complementary businesses tend to fuel each other’s growth, providing the company with a solid foundation for the future.

The foundation of Amazon’s business empire is the company’s e-commerce segment. Its expansive product offerings, extensive system of warehouses and fulfillment centers, and its vast delivery network give the company an unparalleled competitive advantage. This helped Amazon become the world’s largest online seller, then the world’s largest retailer — recently surpassing Walmart. Furthermore, Amazon Prime encourages users to buy more to get the most from their annual membership.

Let’s not forget Amazon Web Services (AWS), the company’s cloud computing segment, which provides businesses with on-demand computing power, content delivery, and data storage. Amazon pioneered the cloud infrastructure business, and it remains the industry leader.

Finally, there’s Amazon’s fast-growing advertising business. Growth is being driven by online product search, Prime Video, live sports programming, and the company’s recent addition of ads to Prime Video.

In the fourth quarter, Amazon’s revenue grew 14% year over year, an impressive growth rate for a company of its size. Each of its largest business segments contributed to the growth. E-commerce revenue grew 12%, while AWS grew 24% — its fastest rate of growth in 13 quarters. Digital advertising also had a strong showing, up 23%.

Investors clearly have AI fatigue, but it’s important to remember that Amazon has been successfully deploying these algorithms for years to support its growth — long before AI went viral. The company’s product recommendations, inventory forecasting, and delivery routing are just a few of the ways Amazon uses AI to boost its revenue and improve efficiency.

Amazon announced plans to spend $200 billion on capex over the coming year, citing strong demand for AWS. Some investors headed for the exits, but that could be a costly mistake, as Amazon is “monetizing capacity as fast as we can install it.” Put another way, the company is building out AWS cloud capacity for demand that’s already there, so it’s clearly the right move.

Amazon has a market cap of roughly $2.3 trillion (as of this writing), so it will need to grow its stock price by about 76% to reach $4 trillion. The company is expected to generate revenue of $808 billion in 2026, according to Wall Street, giving it a forward price-to-sales (P/S) ratio of less than 3. Assuming its P/S remains constant, Amazon would need revenue of roughly $1 trillion annually to support a $4 trillion market cap.

Not surprisingly, Wall Street currently expects Amazon to generate revenue of more than $1 trillion in 2028. If that forecast is accurate, Amazon could surpass a $4 trillion market cap in early 2029, if not sooner. That said, Amazon’s long track record of success and the consistency with which it defies Wall Street’s projections suggest it could reach that benchmark sooner.

Finally, at roughly 29 times earnings, Amazon stock is near its lowest valuation in nearly five years. This gives savvy investors the opportunity to pick up shares of an industry leader and a triple threat at a discounted price.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $460,126!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,732!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $532,066!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you joinStock Advisor, and there may not be another chance like this anytime soon.

Danny Vena, CPA has positions in Amazon and Nvidia. The Motley Fool has positions in and recommends Amazon, Nvidia, and Walmart. The Motley Fool has a disclosure policy.

Brent crude oil rose by 1.2% to over $110 per barrel but had fluctuated multiple times between gains and losses earlier; U.S. stock index futures dropped by 0.4%; Asian stock markets trimmed early gains to a rise of 0.5%, led by tech stocks; Bitcoin fell more than 2% to around $68,800, erasing all the gains

Today’s Change (-2.16%) $-7.79 Current Price $352.80 Key Data Points Market Cap $1.3T Day’s Range $346.64 – $367.70 52wk Range $217.80 – $498.83 Volume 4M Avg Vol 61M Gross Margin 18.03% Tesla (TSLA 2.16%), electric vehicles and energy storage maker, closed Monday at $352.82, down 2.15%. The stock moved lower after bearish analyst commentary and

Thanks largely to a glowing analyst update on a longtime computer storage industry peer, Sandisk (SNDK +3.28%) stock had quite a fine trading session on Monday. The sympathy rally saw Sandisk’s equity rise by more than 3%, on a day when the S&P 500 index could only muster a 0.4% advancement. Soaring storage That Sandisk

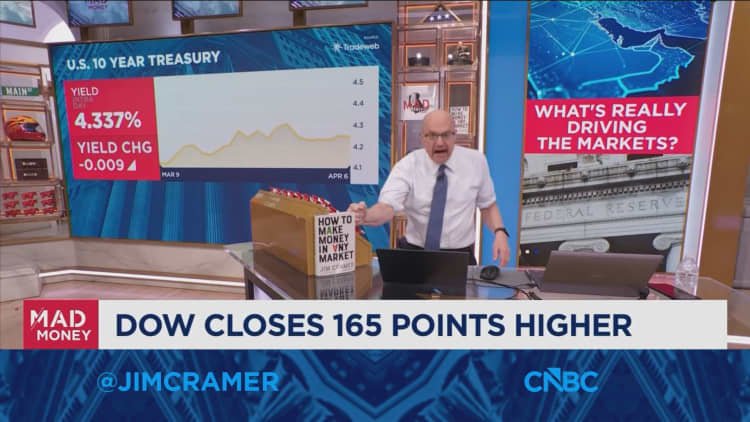

CNBC’s Jim Cramer said investors shouldn’t get comfortable calling a market bottom just yet, because the real driver of this market isn’t geopolitics – its interest rates. On Monday, Cramer noted that the S&P 500 may have bottomed last Monday, March 30, but emphasized that the turning point wasn’t “anything related to stocks themselves,” during

A pedestrian walks past an electronic quotation board displaying the Nikkei 225 stock prices on the Tokyo Stock Exchange in Tokyo on March 23, 2026. Kazuhiro Nogi | Afp | Getty Images Asia-Pacific markets climbed on Tuesday, tracking Wall Street gains, as traders continued to assess Iran war-related developments. U.S. President Donald Trump threatened to target

Healthcare company Biogen (NASDAQ: BIIB) wasn’t looking very healthy on the stock market on Monday. Investors traded out of its shares after learning that the company plans to book a hefty charge in its first quarter, which will directly affect its bottom line. By the end of the day, Biogen’s stock had lost nearly 3%

Does the jobs report make a sound if it falls when the stock market is closed? Investors got an answer to that question on Monday, and it seemed to be “no.” Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical

Today’s Change (6.16%) $0.18 Current Price $3.10 Key Data Points Market Cap $1.7B Day’s Range $2.88 – $3.17 52wk Range $0.84 – $3.17 Volume 39M Avg Vol 27M Gross Margin -1458.78% Kosmos Energy (KOS +6.16%), deepwater Atlantic oil and gas producer, closed Monday at $3.10, up 6.36%. The stock advanced after multiple reports highlighted new

Today’s Change (11.41%) $0.28 Current Price $2.69 Key Data Points Market Cap $3.4B Day’s Range $2.46 – $2.74 52wk Range $0.69 – $4.58 Volume 4.1M Avg Vol 92M Gross Margin -3409.40% Plug Power (PLUG +11.41%), a hydrogen fuel cell systems developer, closed Monday at $2.69, up 11.62%. The stock moved higher after Plug Power secured

Got story updates? Submit your updates here. › Intuitive Machines’ advanced lunar exploration technology faces market volatility, but the company’s long-term prospects remain strong.Houston Today Shares of Intuitive Machines (NASDAQ:LUNR), a Houston-based aerospace company specializing in commercial lunar exploration, fell 4.2% on Monday, trading as low as $22.93. The stock’s decline came amid broader market

There’s little doubt that market volatility can be intimidating. Yet, for those who choose to look at a stock’s long-term return potential, these sharp price movements are somewhat rare opportunities to buy high-quality businesses at attractive prices. Furthermore, market noises force investors to take a step back and fundamentally reassess whether existing growth opportunities are

The United States market has shown impressive strength, rising 3.5% over the last week and climbing 31% over the past year, with earnings projected to grow by 16% annually. In such a robust environment, identifying lesser-known stocks with strong fundamentals and growth potential can offer intriguing opportunities for investors seeking to diversify their portfolios. Name

📌 Top story — scroll down for more updates Bitcoin Surges Toward $70,000 11:10 am — BTC +0.9% Bitcoin (BTC +3.52%) climbed 4% Monday, nearing the $70,000 threshold as geopolitical tensions eased. Reports of potential ceasefire negotiations involving U.S. and Iranian mediators boosted risk appetite across the digital asset space, lifting Ethereum (ETH +5.36%) and

An aerial view of Kowloon, Hong Kong Special Administrative Region Photo: VCG The Hong Kong Stock Exchange (HKEX) market delivered an impressive performance in the first quarter of 2026, with initial public offerings (IPOs) generating HK$110 billion ($13.3 billion) in proceeds, a record high for a single quarter since the second quarter of 2021, according

“During the past year, investors have had to make sense of a great deal of noise and uncertainty, in addition to the human impact of global events. Although we would never want to draw major conclusions from a single year of market data, our analysis is interesting, and this period has served to remind us

The Goldman Sachs Conviction List is a curated list of stocks that the firm’s research team believes are highly likely to outperform the market. It’s a tool for investors to identify stocks with strong growth potential, frequently updated to reflect changes in market conditions and company performance. The list aims to identify stocks where Goldman

American Century Investments, an investment management company, released its fourth-quarter 2025 investor letter for the “American Century Investments Small Cap Value Fund.” A copy of the letter is available to download here. U.S. stocks advanced during the quarter, with large-cap stocks slightly outperforming small-cap stocks, while both groups did better than mid-cap stocks. Across all market

Although several prominent trends have come and gone since the advent of the internet in the mid-1990s, nothing has excited Wall Street and investors quite like the evolution of artificial intelligence (AI). PwC analysts foresee this technology creating more than $15 trillion in global economic value by 2030. While much of the attention has been

Circle Internet (NYSE: CRCL) stock posted strong gains in March’s trading. The cryptocurrency company’s share price managed to climb 14.3% in the month despite the S&P 500 declining 5.1% and the Nasdaq Composite declining 4.8%. Circle stock continued to move higher last month thanks to continued momentum from the encouraging earnings results it reported near