Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

Realty Income (O) continues to attract attention as a large, diversified net lease REIT, with a market value of about US$56.8b and a reported portfolio exceeding 15,500 properties across the U.S., U.K., and Europe.

With annual revenue of US$5.76b and net income of US$1.06b, the stock’s recent month return of about a 9% decline contrasts with a positive total return over the past 3 months and 1 year. This difference is prompting closer scrutiny of current pricing.

See our latest analysis for Realty Income.

At a share price of US$61.15, Realty Income’s short term picture is mixed, with a 1 month share price decline of 8.73% but a 1 year total shareholder return of 11.89% indicating momentum has been building over a longer period.

If this kind of steady income story appeals, it can be helpful to widen your search beyond a single REIT and scan for other income oriented ideas using 12 dividend fortresses

With Realty Income trading at US$61.15 and data implying a sizable intrinsic discount, plus a value score of 2, the key question is clear: is the stock underappreciated today, or is the market already pricing in future growth?

According to the most followed narrative from andre_santos, Realty Income’s fair value of $70.93 sits above the last close at $61.15, implying a valuation gap that income focused investors are watching closely.

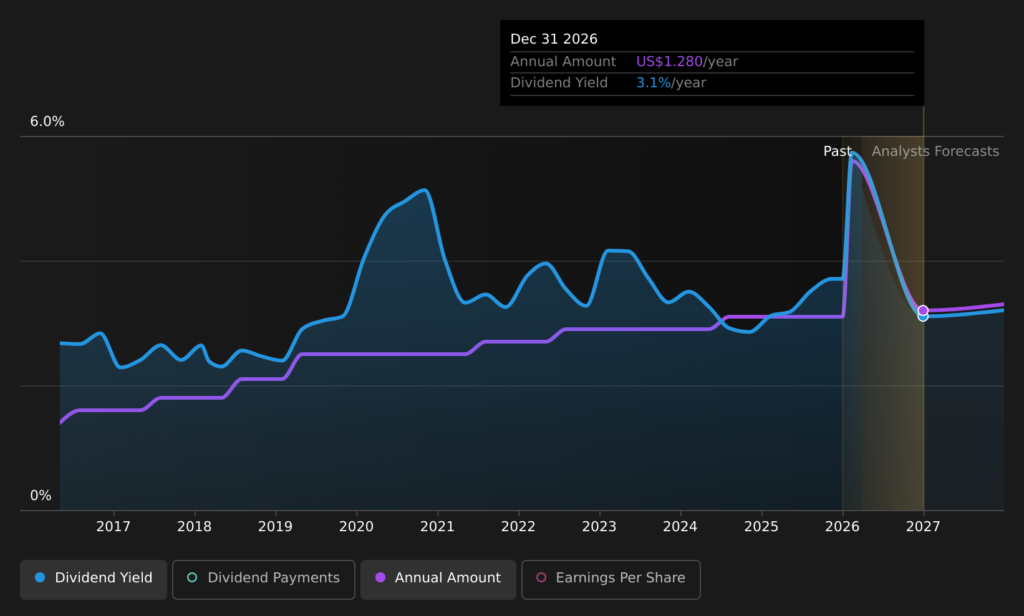

📈 Realty Income is a reliable dividend payer. It”s true that its growing its dividend at a rate a little below or at the economy growth rate ~3%, but its low uncertainty makes this company a safe bet for every dividend investor.

📉 The fact that the volatility and risk on the west, where its revenues are exposed, have been increasing may put pressure on the stream of revenues.

Want to see what sits behind that $70.93 figure? The narrative leans on steady cash generation, modest revenue expansion and disciplined dividend growth assumptions that are anything but casual.

Result: Fair Value of $70.93 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, investors still need to watch for rising funding costs and any sustained hit to tenant health, which could pressure cash flows and challenge the current valuation gap.

Find out about the key risks to this Realty Income narrative.

There is a different message when you look at Realty Income’s P/E ratio. At 53.9x, it sits well above the US Retail REITs industry average of 27x, the peer average of 28.1x, and an estimated fair ratio of 37.1x. This elevates valuation risk if sentiment cools.