- In March 2026, Tarsus Pharmaceuticals announced that its partner Grand Pharmaceutical Group secured National Medical Products Administration approval in China for TP-03 (XDEMVY) to treat Demodex blepharitis, triggering a US$15,000,000 milestone payment to Tarsus and confirming TP-03 as the first approved therapy addressing the disease’s root cause in Greater China.

- This approval not only validates TP-03’s clinical and regulatory profile outside the U.S., but also opens a new revenue stream via milestones and tiered royalties tied to future TP-03 sales and additional regulatory achievements across the Greater China region.

- We’ll now examine how TP-03’s China approval and associated US$15,000,000 milestone might reshape Tarsus Pharmaceuticals’ investment narrative and global growth profile.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

Tarsus Pharmaceuticals Investment Narrative Recap

To own Tarsus today, you need to believe XDEMVY can scale from a single-product U.S. story into a broader, more diversified eye care franchise. The TP-03 approval in China and the US$15,000,000 milestone support that thesis by validating the product globally and modestly strengthening the balance sheet, but they do not remove the near term dependence on U.S. XDEMVY execution or the key risk of high commercial spend against one primary revenue driver.

Among recent developments, the US$200,000,000 debt facility secured in April 2024 stands out in relation to the China news. Together, the new capital and China royalties could give Tarsus more financial flexibility to fund XDEMVY promotion and pipeline programs like TP-04 and TP-05, while investors continue to watch whether prescription growth and gross to net dynamics are sufficient catalysts to offset rising SG&A and concentration risk.

Yet while China’s approval may expand the opportunity, investors should also be aware that…

Read the full narrative on Tarsus Pharmaceuticals (it’s free!)

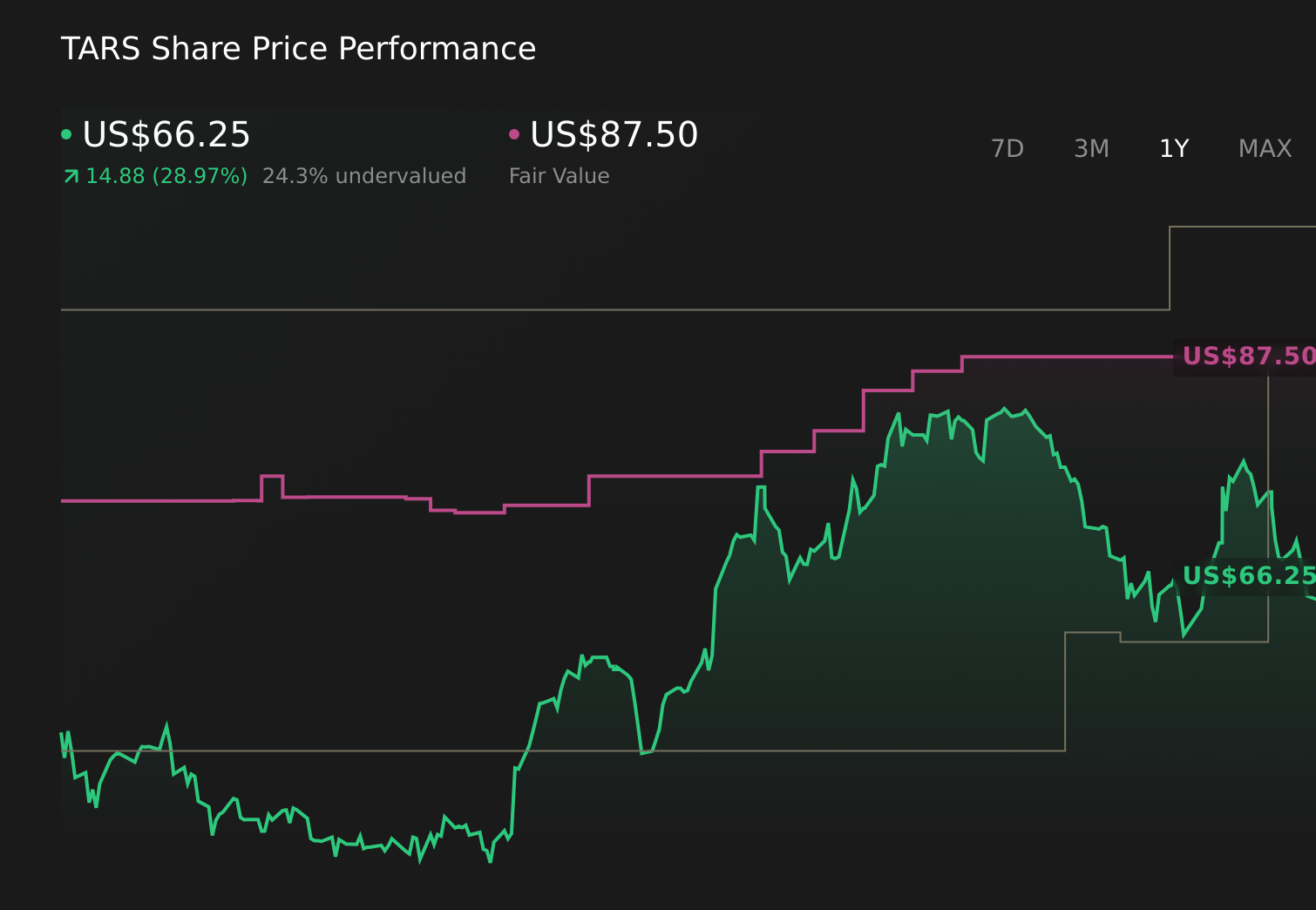

Tarsus Pharmaceuticals’ narrative projects $846.8 million revenue and $237.0 million earnings by 2028. This requires 42.0% yearly revenue growth and a $329.0 million earnings increase from $-92.0 million today.

Uncover how Tarsus Pharmaceuticals’ forecasts yield a $87.50 fair value, a 32% upside to its current price.

Exploring Other Perspectives

While consensus expected about US$988,000,000 of 2029 revenue and US$188,000,000 of earnings, the most cautious analysts warned that heavy dependence on XDEMVY could still backfire, so you should weigh how China’s approval might or might not alter those more pessimistic assumptions.

Explore 4 other fair value estimates on Tarsus Pharmaceuticals – why the stock might be worth just $87.50!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tarsus Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com