Broadcom (AVGO 1.12%) and Advanced Micro Devices (AMD 2.79%) have been trailing Nvidia in the artificial intelligence (AI) chip market in recent years. Still, both companies are now experiencing a nice uptick in their growth thanks to their growing influence in this market.

As it turns out, both chip designers have outperformed Nvidia stock in the past year. While Broadcom has jumped 69% over this period, AMD has logged stronger gains of 92%. But if you had to choose either AMD or Broadcom for your portfolio right now, which one would be the better bet?

Let’s find out.

Image source: AMD.

The case for Broadcom

Broadcom dominates the custom AI processor market with an estimated share of 60% to 80%. These custom processors, known as application-specific integrated circuits (ASICs), are in terrific demand from hyperscalers and AI companies looking to reduce reliance on Nvidia, achieve significant cost reductions, and speed up performance while keeping power consumption in check.

Market research firm TrendForce expects ASICs to account for 27.8% of AI server chips this year, up from 20.9% in 2025. Broadcom is one of the biggest beneficiaries of the growing ASIC adoption. It reported a 106% year-over-year jump in AI revenue in the first quarter of fiscal 2026 (which ended on Feb. 1).

Today’s Change

(-1.12%) $-3.82

Current Price

$337.75

Key Data Points

Market Cap

$1.6T

Day’s Range

$332.22 – $339.00

52wk Range

$138.10 – $414.61

Volume

661K

Avg Vol

32M

Gross Margin

64.96%

Dividend Yield

0.71%

This outstanding growth was driven by Broadcom’s impressive clientele, which includes Alphabet, Meta Platforms, Anthropic, and OpenAI. Broadcom points out that it has six AI customers in total, and all of them are poised to significantly accelerate the deployment of its custom chips next year. Anthropic, for example, is expected to triple the deployment of Broadcom’s ASICs next year to 3 gigawatts (GW). Similarly, Meta Platforms is estimated to scale the deployment of Broadcom’s processors to multiple gigawatts next year.

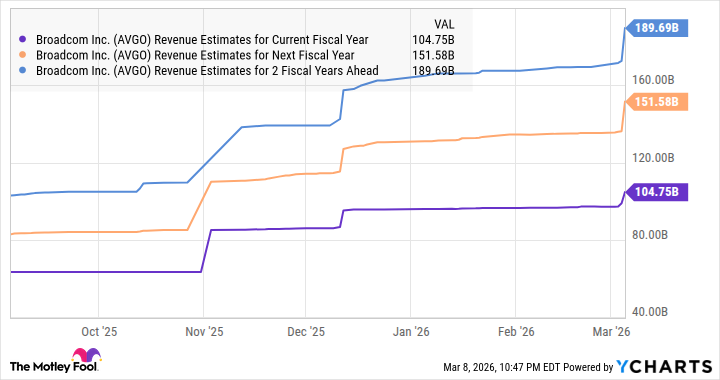

Such impressive customer momentum explains why Broadcom is confident of achieving $100 billion in AI revenue in 2027. That would be a massive increase over the $20 billion in AI revenue it delivered in the previous fiscal year. Not surprisingly, analysts have hiked their growth expectations for Broadcom following its latest report.

AVGO Revenue Estimates for Current Fiscal Year data by YCharts

So, there is a solid chance of this AI stock sustaining its healthy momentum and delivering more upside to investors.

The case for AMD

AMD makes both central processing units (CPUs) and GPUs that are used in computers, data centers, and gaming consoles. The company, however, has been playing second fiddle to Nvidia in the data center GPU market. But CEO Lisa Su is confident the company can achieve a double-digit market share in this space over the next three to five years.

Importantly, AMD’s data center revenue is now growing at a healthy clip, suggesting that it is indeed on track to improve its position in this lucrative market. The company reported $16.6 billion in data center revenue for 2025, up by 32% from the prior year.

Today’s Change

(-2.79%) $-5.71

Current Price

$199.12

Key Data Points

Market Cap

$334B

Day’s Range

$196.68 – $203.62

52wk Range

$76.48 – $267.08

Volume

879K

Avg Vol

36M

Gross Margin

45.99%

AMD credited this solid growth to the growing adoption of its Instinct data center GPUs. Looking ahead, the Instinct processors should continue to drive stronger growth in AMD’s data center business, especially considering that it has secured multibillion-dollar deals with multiple customers. Meta Platforms, for instance, is poised to deploy up to 6 GW of its Instinct GPUs.

This contract could give AMD a massive boost in the long run. Additionally, it already has a deal in place with OpenAI to deploy 6 GW of chips to help the latter build more computing capacity. This deal is poised to kick off in the second half of 2026. Moreover, there are additional catalysts in AMD’s bag, such as the growth of the AI-focused personal computer market and its growing influence in AI server CPUs.

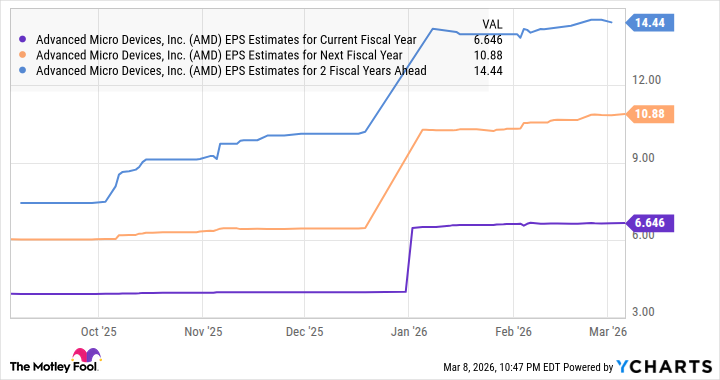

As such, it is easy to see why analysts are forecasting a 59% increase in AMD’s earnings this year to $6.64 per share. The good news is that its bottom-line growth is poised to remain solid over the next two years as well.

AMD EPS Estimates for Current Fiscal Year data by YCharts

The verdict

Both AMD and Broadcom are growing at solid rates, and they are likely to sustain their momentum in the future thanks to the secular growth of the AI chip market. That’s why investors should take a closer look at their valuations before deciding which one of these AI stocks is worth investing in.

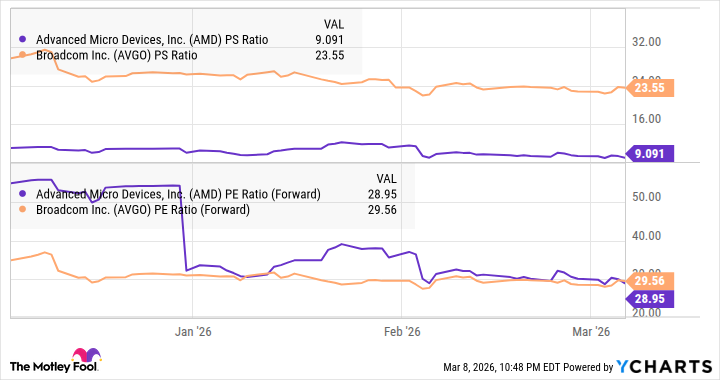

AMD PS Ratio data by YCharts

Though there isn’t much difference between their forward earnings multiples, AMD’s sales multiple of 9 is significantly lower than Broadcom’s 24. Still, the exponential growth that Broadcom could deliver in its AI revenue by next year could help justify the huge premium. As such, investors can’t go much wrong if they invest in either of these semiconductor companies since both of them are positioned to grow impressively in the future.