Nvidia (NVDA 2.94%), Alphabet, Apple, Microsoft, Amazon, Meta Platforms (META 2.33%), and Tesla — collectively known as the “Magnificent Seven” — have produced monster gains for long-term investors. But all seven stocks have lost value so far in 2026 — and that should merit some attention from investors on the lookout for opportunities.

Nvidia and Meta Platforms — in particular — are compelling valued based on a key metric. Here’s why both growth stocks are selling off, and some context to help you decide which one could be the better buy for you in March.

Image source: Getty Images.

Why forward P/E matters

The price-to-earnings (P/E) ratio is one of the most popular metrics for evaluating stocks. And for good reason, as it’s simply the price of the stock divided by earnings per share.

Companies with clear ways to deploy capital effectively deserve premium valuations. A company like Coca-Cola can expand into new markets and acquire or develop new beverage lines. But it doesn’t have nearly as many levers to pull to accelerate earnings growth compared to a company like Amazon — which plays in so many different end markets.

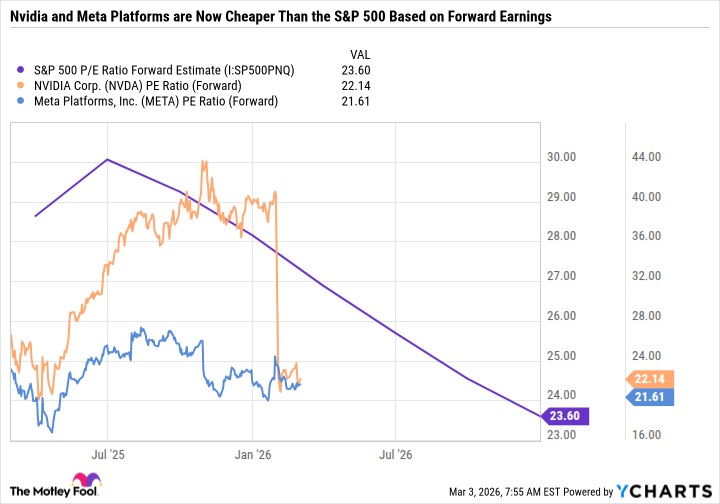

The forward P/E ratio rewards companies by dividing the stock price by analyst consensus earnings estimates for the next year. For example, Nvidia has a 37.2 P/E compared to 29.6 for the S&P 500, but just a 22.1 forward P/E compared to 23.6 for the S&P 500. Similarly, Meta Platforms is also slightly cheaper than the S&P 500 based on forward earnings.

S&P 500 P/E Ratio Forward Estimate data by YCharts

Granted, forward P/E can inflate a stock’s value if a company misses on earnings. And investors who are buying stocks and planning to hold them over the long term likely care more about a company’s earnings over several years, if not decades, rather than what they are today.

A top AI infrastructure play

Nvidia is by far the best Magnificent Seven stock for investors who believe the company can sustain earnings growth even close to its current rate. For its fiscal 2026 — which was the 12 months ended Jan. 25, 2026 — the company grew revenue by 65% and diluted earnings per share by 59.5%. Nvidia’s valuation is still reasonable, even though its stock price has soared, because the company has grown its earnings rapidly.

However, just a handful of cloud providers and hyperscalers are driving a little over half of Nvidia’s data center revenue — which makes up just under 90% of its sales. If one or two key customers pull back on spending, Nvidia’s growth rate will fall. But given its volatility, Nvidia would still be a steal at current levels if it could grow earnings by, say, 20% to 30% per year.

Today’s Change

(-2.94%) $-5.39

Current Price

$177.95

Key Data Points

Market Cap

$4.3T

Day’s Range

$176.83 – $182.75

52wk Range

$86.62 – $212.19

Volume

6M

Avg Vol

177M

Gross Margin

71.07%

Dividend Yield

0.02%

The long-term opportunity is even more appealing, as prominent innovations position Nvidia to go beyond the data center and be a leader in agentic artificial intelligence (AI) and physical AI (general robotics and self-driving cars). If Nvidia can diversify its customer base and reduce its dependence on data center revenue, it should be less prone to a cyclical pullback in hyperscaler spending.

The AI snowball

Meta is the best buy for investors looking for companies that are already capitalizing on their AI investments. Its business model is significantly different from other top hyperscalers (and key Nvidia customers) like Amazon, Microsoft, and Alphabet, which are investing in data center infrastructure to meet demand for cloud and AI services, even if it takes a sledgehammer to free cash flow (FCF).

The social media titan is one of the best examples of a company rapidly monetizing AI rather than building AI infrastructure and hoping customers see a return on their AI spending. AI is improving Meta’s family of apps (Instagram, Facebook, Messenger, and WhatsApp) for users, creators, and advertisers.

Meta uses AI to connect users with content and ads that align with their interests. AI drives Meta’s open-source Large Language Model Meta AI (Llama) — which powers Meta AI assistants. Meta’s Reality Labs division, which includes augmented and virtual reality products and metaverse projects, is also investing in AI-powered hardware.

Today’s Change

(-2.33%) $-15.42

Current Price

$645.15

Key Data Points

Market Cap

$1.6T

Day’s Range

$636.23 – $649.45

52wk Range

$479.80 – $796.25

Volume

928K

Avg Vol

15M

Gross Margin

82.00%

Dividend Yield

0.33%

Perhaps Meta’s greatest advantage is that it can afford to aggressively spend because the family of apps is so profitable. In many ways, Meta is an AI snowball. AI investments improve the family of apps business, accelerating high-margin growth and boosting FCF, which can be used on projects that may take several years to turn profitable or fail entirely.

All told, Nvidia and Meta are high-conviction buys for investors who believe the potential rewards of these companies far outweigh the discussed risks. The cheaper both stocks become, the more risk is being taken off the table for long-term investors.