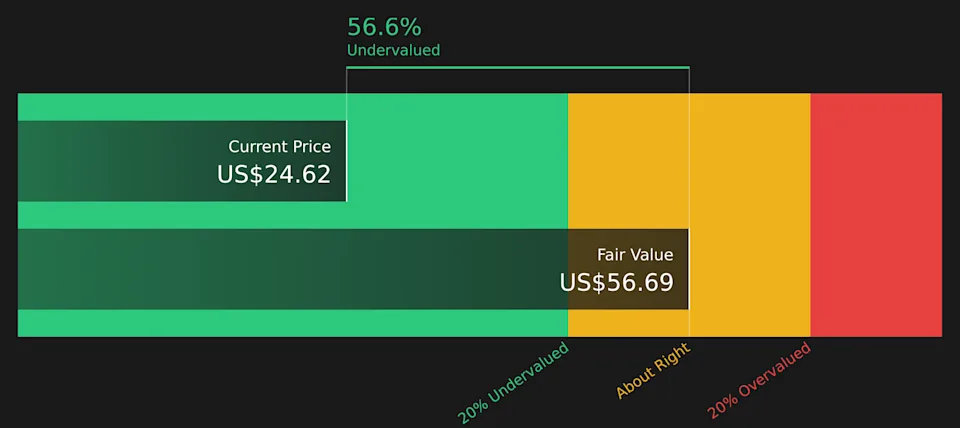

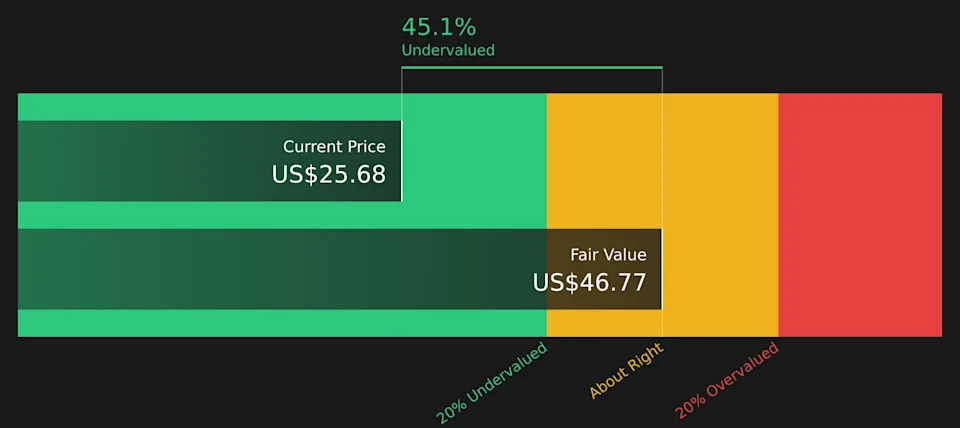

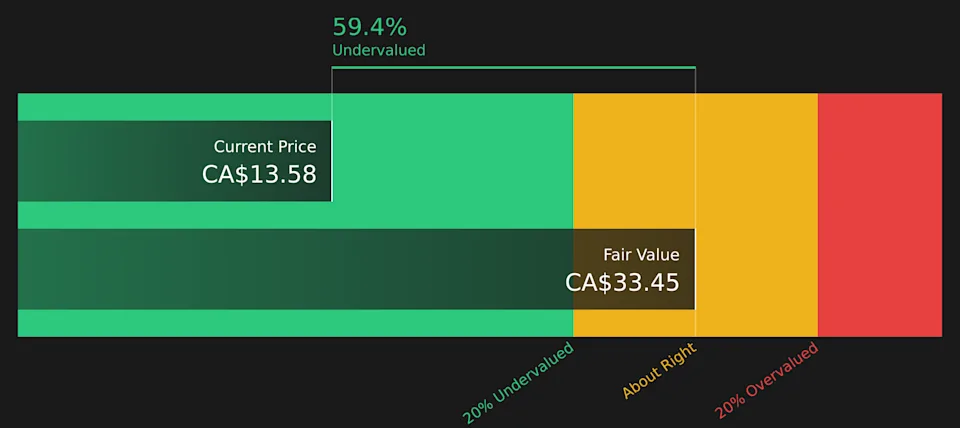

Even before factoring in Monday’s monster surge in oil and gas stocks, the energy sector was already up 24.2% year to date compared to just 0.5% for the S&P 500 (^GSPC 1.33%). Sectorwide underperformance in 2025, paired with rising oil prices and now geopolitical tensions in Iran, are fueling the rally.

But investors may be surprised to learn that energy stocks account for only 3.5% of the S&P 500, whereas Nvidia (NVDA 2.94%) alone makes up 6.9%. That means Nvidia is worth more than the combined value of ExxonMobil (XOM +0.34%), Chevron (CVX +0.05%), and the other 20 or so energy stocks that are S&P 500 components.

Here’s why Nvidia deserves to make up such a large portion of the U.S. stock market, how to think about energy within the context of the broader market, and why energy stocks are still relatively cheap.

Image source: Getty Images.

Earnings speak for themselves

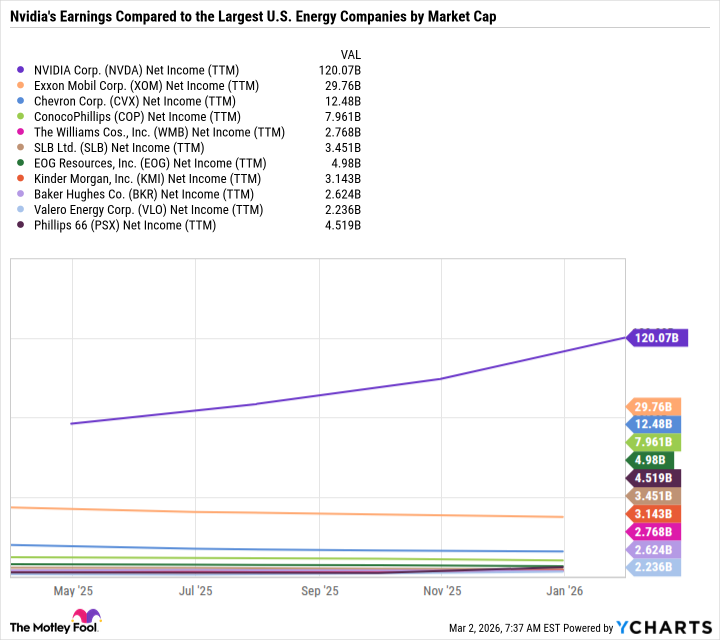

Part of the reason Nvidia is worth so much more than the entire energy sector is valuation. Nvidia sports a 36.1 price-to-earnings (P/E) ratio compared to 22.3 for the State Street Energy Select Sector SPDR ETF (XLE +0.16%), which tracks energy stocks that are components of the S&P 500. But Nvidia is also massively profitable.

Nvidia earned $120 billion in trailing-12-month profit, making it the second-most profitable company in the world behind Alphabet. The chip giant’s trailing-12-month earnings are nearly triple those of ExxonMobil (XOM +0.34%) and Chevron (CVX +0.05%) combined, and significantly higher than the 10 largest holdings in the Energy Select Sector SPDR ETF.

Data by YCharts.

Nvidia is an incredible value

Not only is Nvidia raking in the net income, but it is also converting well over half of its revenue into after-tax net profit. Even the best oil and gas companies can’t compete with those margins.

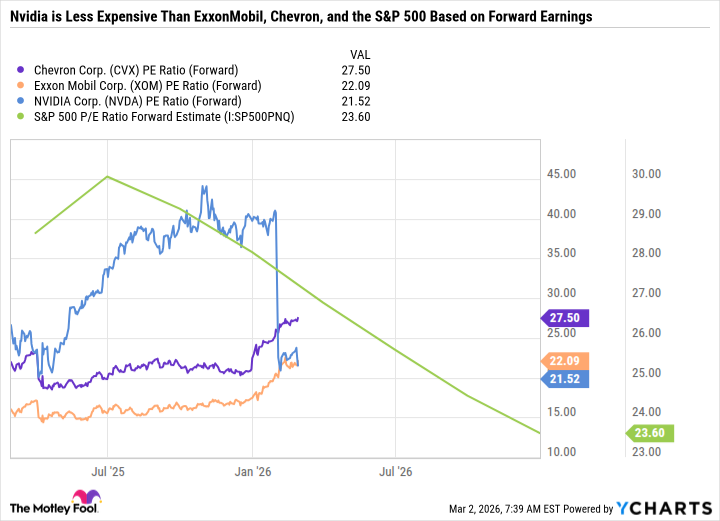

Nvidia is still growing rapidly, with revenue up 65% over the past year. And because Wall Street analysts expect Nvidia’s earnings to continue soaring, its forward P/E ratio is way lower than its trailing P/E. In fact, it’s even lower than the forward P/Es of ExxonMobil, Chevron, and the S&P 500. Meaning that if Nvidia delivers on expectations, it’s arguably a better value than leading U.S. oil majors.

Data by YCharts.

Of course, there are many nuances to basing valuations on forward earnings. Earnings expectations for oil and gas companies will rise if higher oil prices hold. Similarly, Nvidia’s estimates could come down if companies pull back on their artificial intelligence (AI) spending. But that probably won’t happen anytime soon.

There’s value across the market if you know where to look

Comparing the energy sector to Nvidia illustrates that two seemingly contradictory points can both be true.

Energy stocks are arguably still undervalued because they were relatively cheap entering the year, whereas Nvidia’s earnings continue to surge, but its stock price has gone virtually nowhere for seven months, which has brought down its valuation.

Today’s Change

(-2.94%) $-5.39

Current Price

$177.95

Key Data Points

Market Cap

$4.3T

Day’s Range

$176.83 – $182.75

52wk Range

$86.62 – $212.19

Volume

6M

Avg Vol

177M

Gross Margin

71.07%

Dividend Yield

0.02%

As a long-term investor, it can be confusing to see such swift changes in narratives. It wasn’t long ago that megacap growth stocks like Nvidia were powering the S&P 500 to new heights. Now, it’s sectors chock-full of value stocks like energy, materials, and consumer staples that are crushing the S&P 500.

Investors are gravitating toward sectors with hard assets. Producing, transporting, and selling hydrocarbons is far less prone to AI disruption than some software companies. And the market is rewarding that insulation.

Instead of jumping in and out of sectors based on what is red-hot or out of favor, a better strategy is to build your portfolio around companies built to last.

When approaching the energy sector, look for companies with rock-solid balance sheets and diversified and cost-efficient assets rather than a risky company that needs oil prices to soar to do well. ExxonMobil and Chevron certainly fit that high-quality blueprint, as they both can still support the cost of their operations, long-term investments, dividends, and buybacks at far lower oil prices.

What’s more, both ExxonMobil and Chevron have impressive track records of increasing dividends. ExxonMobil has boosted its payout for 43 consecutive years and yields 2.7%, while Chevron has increased its payout for 39 consecutive years and yields 3.8%.

All told, energy stocks remain a compelling value for passive-income investors who believe in sustained demand for oil and gas, even as cleaner alternatives are increasingly adopted. Nvidia is a fantastic buy if you think it can continue playing a leading role in generative AI, and advancements in agentic AI and physical AI.