JPMorgan’s bearish stance on the US dollar is being challenged by the significant threat of oil prices potentially breaking through $100.

According to Zhitong Finance, the foreign exchange strategy team at JPMorgan, a Wall Street financial giant, stated that as military conflicts between the United States-Israel and Iran continue to escalate, causing significant disruptions to crude oil and LNG transportation across the Middle East, the ongoing impact of rising oil prices poses the greatest threat to the institution’s forecast that the US dollar will weaken significantly this year. For major Wall Street firms like JPMorgan that hold bearish views on the US dollar, their rationale for shorting the dollar is facing a major challenge due to rising oil prices — if oil prices continue to increase and surpass $100, the logic behind shorting the dollar could collapse entirely.

For months, JPMorgan has maintained a bearish stance on the US dollar while favoring so-called high-beta currencies such as the Australian dollar and the Mexican peso — currencies that are particularly sensitive to global risk sentiment. JPMorgan strategists Meera Chandan, Octavia Popescu, and Patrick Locke wrote on Monday that this position was originally based on the assumption that the likelihood of an unprecedented price disturbance in the commodities market was low; however, they now indicate that this view is gradually losing validity.

Following airstrikes by the United States and Israel on Iran over the weekend, international oil prices — including Brent crude and WTI crude — recorded their largest gains in four years; as Iran retaliates, this conflict is triggering significant ripple effects across the Middle East and Gulf nations. US President Donald Trump stated that the bombing campaign against Iran might last for several weeks.

Following airstrikes by the United States and Israel on Iran over the weekend, international oil prices — including Brent crude and WTI crude — recorded their largest gains in four years; as Iran retaliates, this conflict is triggering significant ripple effects across the Middle East and Gulf nations. US President Donald Trump stated that the bombing campaign against Iran might last for several weeks.

The JPMorgan strategy team wrote: ‘The escalation of military conflict between the US/Israel and Iran marks a significant risk to regional stability, with pricing trends and reactions in the foreign exchange market primarily reflected through the energy price channel.’ They anticipate that higher energy prices will drive a substantial rise in inflation, thereby boosting the US dollar and pressuring other sovereign currencies, including the euro and the yen.

Once the risk in Hormuz pushes oil prices into triple digits, the triple pressures of inflation, interest rates, and consumption will not only render the old playbook of ‘bottom-fishing in US stocks’ completely ineffective but also expose highly leveraged bets against the dollar to massive losses.

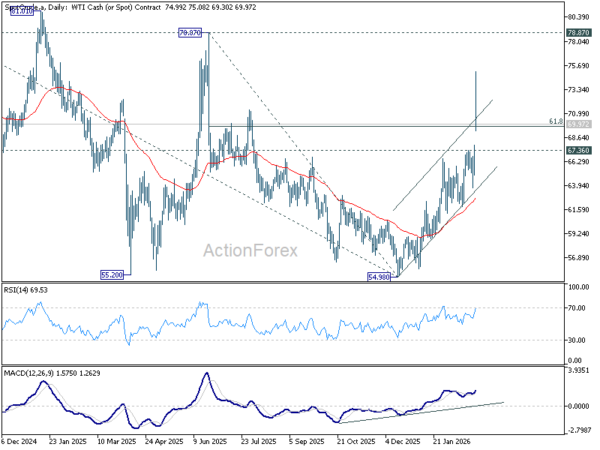

Although a rise in oil prices to $100 is not yet the consensus forecast among oil analysts, it has become a significant potential risk that stock market bulls are considering. If energy costs continue to soar, they will not only threaten consumer spending growth but may also reignite inflation and push interest rates higher again — a market reasoning scenario that unfolded in real-time in the financial markets on Monday: The classic safe-haven asset — US Treasuries — failed to play their traditional role during this period of heightened geopolitical tension, with yields surging sharply due to fears of renewed inflation and the possibility of the Federal Reserve shifting towards rate hikes amid high prices. West Texas Intermediate (WTI) crude prices rose by as much as 12% to $75.33 per barrel before trimming half of the gains, trading near $71. Meanwhile, Brent crude surged 7.4% on Monday, closing at $77.85 per barrel.

The Bloomberg Dollar Spot Index rose by 0.8% in Monday’s trading session, reaching a five-week high and moving higher alongside US Treasury yields. The euro (EUR/USD) fell nearly 1% to $1.1695, while the yen dropped more than 1% to 157.71 yen per dollar, its weakest level in three weeks.

Following President Trump’s announcement of an ongoing military campaign against Iran with no end in sight for at least four weeks, and as hostilities extend beyond Iran and Israel to other Middle Eastern economies—such as Iran launching drone and missile attacks on critical U.S. infrastructure in Dubai, Abu Dhabi, Bahrain, and Kuwait, while Lebanon initiates another round of rocket attacks on Israeli territory—the unpredictable geopolitical turbulence in the Middle East and its ripple effects on rising oil prices have given fund managers new reasons to sell risk assets like equities en masse, shifting toward traditional safe-haven assets such as gold, the U.S. dollar, and commodities like crude oil, which are expected to benefit significantly from the crisis in the short term.

JPMorgan pointed out that four distinct trends related to the divergence between energy importers and exporters have emerged in the currency market:

As the US has become a net oil exporter, the US dollar will benefit against all currencies, and JPMorgan emphasized that ‘any further moves to unwind short positions in the dollar could provide additional tactical support for the currency.’

Currencies of other oil-exporting countries, such as the Norwegian krone, as well as broader commodity-linked currencies, will also receive support.

Currencies of oil-importing countries, such as the euro, Polish zloty, Czech koruna, and Hungarian forint, may experience the largest declines, followed by key sovereign currencies in Asia.

Safe-haven currencies will diverge, with the yen under pressure, the Swiss franc potentially performing relatively well, and gold emerging as a clear net beneficiary.

The quagmire of Iraq or the ‘Venezuela model’?

The question facing the market now is: Is this a long-term regime change operation, similar to the kind of political struggle and quagmire that followed the U.S. invasion of Iraq in 2003? Or is it a short-term geopolitical shock akin to Venezuela, aimed at pressuring Iran’s remaining leadership into an agreement? If diplomacy resumes quickly and Iran avoids attacking core energy infrastructure and shipping in the Middle East, initial risk-off sentiment is likely to fade. If the conflict persists and drags energy production and export infrastructure into the fray, markets will need to reprice for an environment of higher oil prices, interest rates, and currency volatility, while the stock market could pay a heavy price for stagflationary trends.” said Michael Ball, macro strategist at Bloomberg Strategists.

Crude oil and LNG (liquefied natural gas) shipping through the Strait of Hormuz has nearly come to a halt, while a major refinery in Saudi Arabia experienced a production disruption, causing a severe supply-side shock to energy markets and prompting a sharp rise in crude oil prices. If the Strait of Hormuz remains closed to oil and gas transportation for an extended period, some Wall Street analysts have already incorporated the $100 oil price level into their financial market forecasting models.

The JPMorgan foreign exchange strategy team advises traders to unwind or close long positions in the euro. They noted that if energy prices continue to rise, the euro could fall to the $1.10 to $1.13 range, near levels seen a year ago, although this is not their base case. The strategists wrote that they would look for opportunities to re-establish long positions in the euro once there is more clarity in the crude oil market.

Nevertheless, these foreign exchange strategists from JPMorgan continue to maintain short positions on the U.S. dollar against sovereign currencies like the Australian dollar and Norwegian krone, as these currencies are ‘well-positioned to benefit from potential trends of higher energy prices, relative trade conditions, and underlying economic growth trends’; however, they have tightened the stop-loss levels on these positions to protect accumulated gains.