On Monday this week (March 2), influenced by the escalation of the situation in the Middle East, the US dollar opened stronger, with intraday gains expanding at one point. As of now, the increase has narrowed to approximately 0.5%. Compared to the market risk aversion sentiment triggered by the tensions in the Strait of Hormuz, this reaction remains relatively restrained. Investors’ core concerns have shifted from the ‘duration of the conflict’ to whether ‘shipping through the Strait of Hormuz can be restored,’ as well as whether Trump’s previous statement of a ‘four-week military operation’ will lead to further escalation.

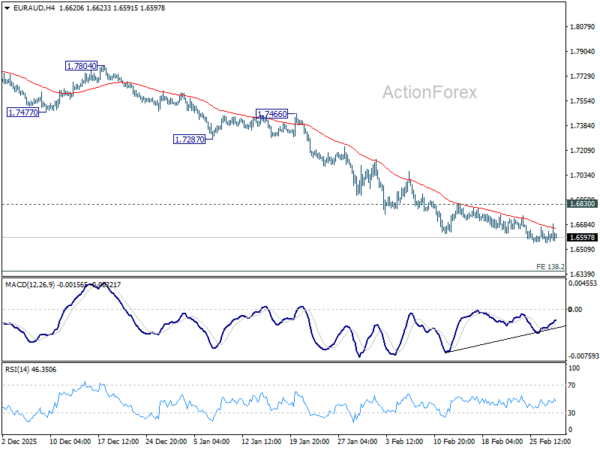

The market is weighing two scenarios: if Trump controls the duration of military actions as expected and shipping through the Strait of Hormuz gradually resumes, Brent crude oil prices are likely to stabilize in the range of $75-80 per barrel; if the conflict escalates, leading to a prolonged blockade of the strait, oil prices may quickly exceed $90 per barrel, thereby pushing up US inflation and forcing the Federal Reserve to adjust its interest rate cut schedule. The latter scenario would directly impact the eurozone and the euro, which heavily rely on oil imports, with the euro-to-dollar exchange rate already falling 0.3% during the Asian early trading session.

Investors are closely watching the Federal Reserve meeting scheduled for over two weeks from now, focusing on its adjustment of risk priorities. Previously, Fed Governor Milan repeatedly emphasized the need for a 100-basis-point interest rate cut (i.e., four cuts) by 2026, favoring earlier implementation. This stance is primarily based on the current weak inflationary pressure in the United States, lacking strong price-driving factors. However, the oil price fluctuations caused by the situation in the Middle East may prompt the Fed to reassess inflation risks versus economic support needs, adjusting the timing and magnitude of rate cuts.

Before last weekend, the prevailing market view was that, amid slowing inflation and a stabilizing labor market, the Fed was poised to resume interest rate cuts around June, making the medium-term outlook for the US dollar bearish. Following the US Supreme Court’s tariff ruling, a reduction in the average tariff rate is expected to further suppress prices. Companies cutting costs by lowering product pricing while raising transportation and insurance service fees also explains why US inflation growth has fallen short of expectations.

Before last weekend, the prevailing market view was that, amid slowing inflation and a stabilizing labor market, the Fed was poised to resume interest rate cuts around June, making the medium-term outlook for the US dollar bearish. Following the US Supreme Court’s tariff ruling, a reduction in the average tariff rate is expected to further suppress prices. Companies cutting costs by lowering product pricing while raising transportation and insurance service fees also explains why US inflation growth has fallen short of expectations.

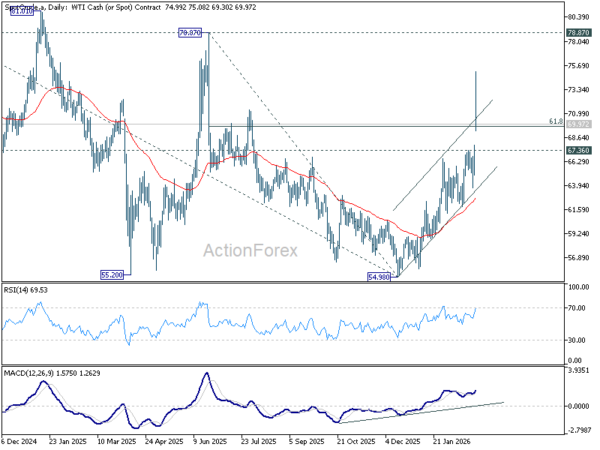

The current market narrative has diverged: On one hand, the sharp short-term spike in oil prices (ICE Brent crude surged 13.04% at the March 2 opening to $82.37 per barrel, with gains narrowing to around 8.3% by the close of the day) has raised concerns about a rebound in inflation, potentially delaying the Fed’s rate-cut cycle temporarily. This expectation benefits US dollar bulls, pressuring the euro-to-dollar exchange rate and some other European currencies — these economies, closer to the conflict zone, face significant pressure from purchasing energy resources at high prices, resulting in notable currency depreciation. On the other hand, calls for interest rate cuts within the Fed persist, with officials like Milan arguing that the current interest rate level is ‘too high and restrictive.’ If oil prices fall and geopolitical risks ease, the rate-cut process could still proceed as originally anticipated, putting downward pressure on the US dollar.

According to Monex Group analysis, if Brent crude oil remains in the $85-95 per barrel range, it will cause a supply shock to Japan, disrupting Saeko Takagi’s economic stimulus plan. In this scenario, Japanese inflation is expected to accelerate by 0.5 percentage points. The slowdown in Japanese inflation during January-February had provided the prime minister with policy space, but sudden changes in the Middle East situation and oil price volatility could alter everything. Affected by this, the USD/JPY exchange rate has risen to 157.47, with an increase of 0.91%, further intensifying the depreciation pressure on the yen.

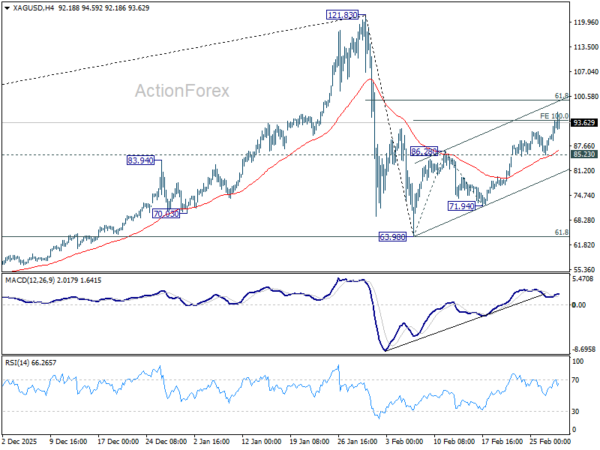

Gold has become one of the main beneficiaries of the recent escalation in the Middle East situation. On March 2, COMEX gold prices surged past $5,409 per ounce, rising over 3%, but by March 3, the spot price of London gold fell to $5,299.13 per ounce, down $87.03 from the previous trading day, representing a 1.62% decline, exhibiting a ‘sharp rise followed by a pullback’ pattern. In February, precious metals recorded their seventh consecutive monthly gain, marking the longest continuous uptrend since 1973. Coupled with geopolitical factors such as the kidnapping of Venezuela’s president and US tariff threats against Europe over Greenland, gold’s safe-haven appeal will continue to attract capital, with upside potential after short-term corrections.

Currently, investors’ reactions to fluctuations in risk premiums remain more pronounced than to fundamental factors: the short-term surge and plunge in oil prices, developments in shipping through the Strait of Hormuz, statements by Fed officials, and progress in the Middle East conflict have all become key variables influencing market movements. In this environment of high volatility and uncertainty, the safe-haven value of gold and the periodic strength of the US dollar will alternately come to the fore, while currencies such as the euro and yen continue to face dual pressures from geopolitics and energy.