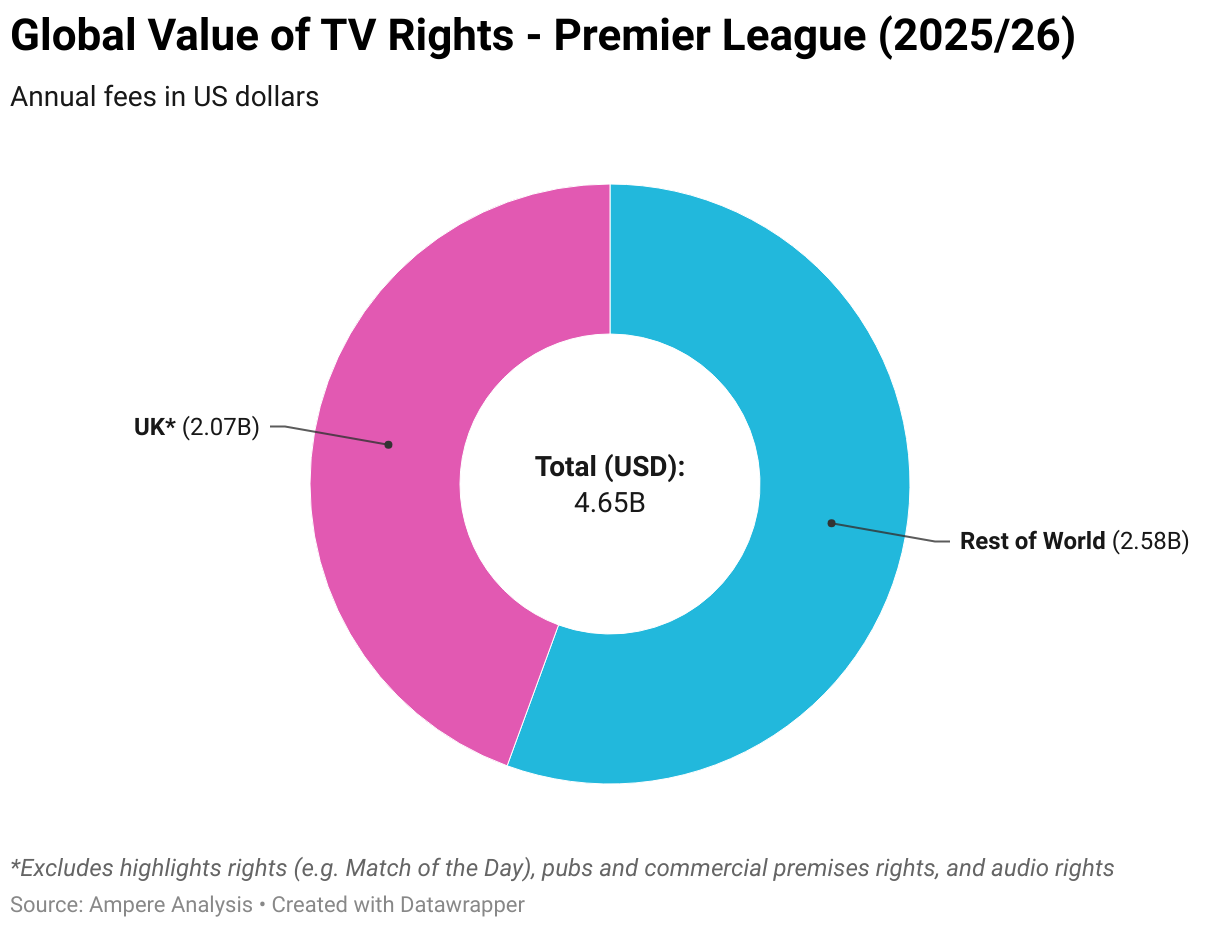

The Premier League is unique among major sporting properties in that it generates more revenue from its international broadcast deals than its domestic arrangements. This situation has frequently led to suggestions that it should launch its own global streaming service.

The league has shown little appetite in changing what has been a hugely successful model in favour of the fantasy economics that support the idea of ‘Premflix’.

However, it has spent the past few years fine tuning a technological and commercial framework that could support a direct-to-consumer (DTC) service in specific instances.

Now, it’s ready to go live with ‘Premier League +’, a new streaming offering that will bring together all of its content and enable direct relationships with fans for the first time.

But why now and what does this mean for both global soccer and global broadcasting?

What is Premier League + and where will it be available?

Premier League+ will broadcast all 380 matches from English soccer’s top-flight in Singapore from the start of the 2026/27 campaign. This coverage will be supported by a range of additional content, including magazine shows, highlights and archive footage, a combination which the league hopes will be irresistible for fans.

The platform will be operated in partnership with Singaporean telecommunications giant StarHub, which fended off competition from Singtel to sign a six-year media rights deal with the Premier League in 2022.

The Premier League has not confirmed pricing, nor has it explained how marketing and production costs and subscription revenue will be shared between the competition and StarHub.

Why is Premier League + launching now?

Going DTC in a limited fashion is a move the Premier League has considered making for several years. It believes that in some markets, it has sufficient brand awareness and consumer demand to go it alone and forego working with a broadcast partner that would assume the risk, marketing obligations, and technological considerations.

Indeed, the Premier League almost went DTC in Singapore back in 2019 for those reasons as well as the fact that the country is relatively wealthy, has high IPTV adoption, and advanced connectivity.

However, two major developments in the past seven years have made going DTC more attractive. The first is that pay-TV platforms, especially those with telecommunications divisions, see their ability to aggregate as more important than offering exclusivity.

StarHub already sublicences some Premier League rights to free-to-air (FTA) service Mediacorp and sees retaining access to the Premier League, along with sharing some of the financial rewards and reducing some of its upfront costs, as the most important consideration.

The second is that, from 2026, the Premier League is taking production in-house, ending its joint venture with IMG and assuming responsibilities for all live coverage, studio-based content and other programming.

This shift means the Premier League has more immediate control over production and broadcast relationships, greater freedom to implement new broadcast technologies and content formats and can tailor its offering to individual markets. All of these benefits are hugely important when it comes to launching a DTC service.

Will Premier League + be coming to other markets?

Singapore is the ideal test bed for Premier League +, and the league has made no secret of its wish to scale the model to other markets in the future. However, any other territory must meet the same technological and commercial pre-requisites.

Going DTC is hard. It relies on significant investments in technology, marketing and customer service without any guarantees it will deliver more revenue than a traditional rights sale. It’s a lot of effort and risk to take for a property and is why traditional media rights agreements are so popular.

In some countries, the sums will never add up. In the US and the Nordics, for example, the Premier League is just too important to NBC and Viaplay’s business that they are willing to pay far more in rights fees than what could be generated via DTC. Meanwhile, in others, there may be an absence of sufficient connectivity or a culture of paying for content.

But if the Premier League can prove the concept in Singapore, then it will feel emboldened to expand, either alone or with a partner, in other countries. Additionally, if it has a proven tech stack and business model, Premier League + will act as a useful bargaining chip when negotiating with partners where it still wants a traditional rights fee relationship.

Will Premier League + launch in the UK?

No. This will never happen unless the Premier League decides to make Premier League + a single global streaming service, a development which would require a dramatic upheaval in the global media market.

The logic behind ‘Premflix’ was that cutting out the middle man and targeting a global audience would allow the Premier League to offer a consumer-friendly competitive price point that would attract tens of millions of subscribers and ultimately generate more revenues for the Premier League’s 20 clubs.

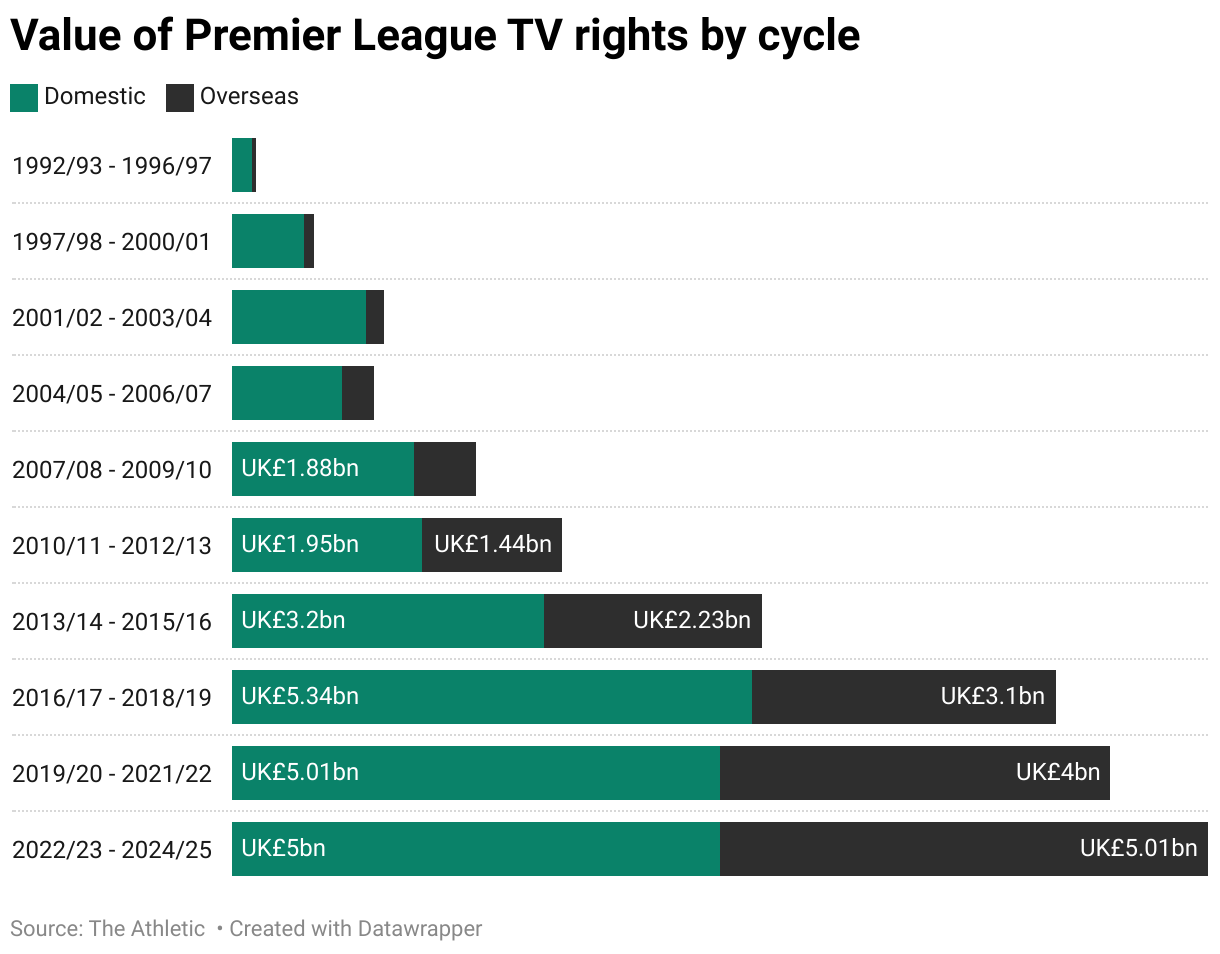

But the Premier League has generated UK£12.25 billion (US$16.41 billion) in broadcast and commercial revenue for the 2025 to 2028 cycle and international media rights income alone is up by 27 per cent. Even when sponsorship revenue is removed from that figure – that’s a huge number of subscribers needed to justify the change in approach.

The very fact this idea was once called ‘Premflix’ exposes it was based on the early experiences of Netflix, which spent billions on content and made its service as cheap as possible to acquire as many subscribers as possible. However, a lack of new expansion opportunities and pressure to turn a profit saw it increase prices and reduce costs, consolidating its early mover advantage.

Netflix remains hugely successful, but those early strategies are no longer applicable and not everyone can emulate its approach. Other multi-genre services have faced similar challenges and sports-specific streaming services have so far struggled to make an impact unless they behave like traditional broadcasters.

High-profile examples of single-property services are almost non-existent and Ligue 1+ has proved to be a cautionary tale.

Even if the Premier League was able to acquire a hundred million subscribers, each paying UK£15 (US$20.09) a month, it would have significant costs to cover, would absorb a lot of risk, and would risk losing customers if it increased prices.

On top of that, limited inventory and narrow scope would mean the Premier League would have even fewer options than Netflix to diversify or expand its offering. Increasing average revenue per user (ARPU) would be a headache, and at any price level, the risk of churn in summer months where there is no live soccer would be ever-present.

What does this mean for the Premier League’s relationship with broadcasters?

For all these reasons, it’s wise to see Premier League + as an evolution of its broadcast strategy that reflects changing economic models and consumption habits in certain markets rather than a radical change in thinking.

Firstly, the fact the league is partnering with StarHub is significant as it indicates a willingness to work with, not against the industry. Indeed, it’s possible that Premier League+ could be sold as a wholesale product that complements or even replaces other coverage – potentially increasing its rights fees by expanding and futureproofing its product.

Ultimately, the Premier League has no desire to upset the status quo. International broadcast revenues continue to rise and although domestic income is broadly flat, the league should see an uptick in its next cycle as it releases more inventory to the market.

Virtually any other organisation outside the US would be envious of this situation.

The Premier League’s success has been built on building strong direct relationships with global broadcasters and this will remain the same for some time to come.