I’m not going to hold myself out as an expert on investing. But I believe I have some helpful advice for at least some investors, thanks to working at The Motley Fool for more than a decade, my prior related business experience (which involved meeting with top management, sometimes at publicly traded companies), and graduate school courses on topics such as analyzing financial statements.

The good news is that if you’re willing to put in the effort to continuously improve your investing, you have a good shot at beating the market over the long term.

I’ll call my tips “rules,” but they’re not hard-and-fast rules. Below are seven of them, counting each subportion of Rule 1 as one.

Image source: Getty Images.

Rule 1: NEVER forget that you’re mainly betting on the jockey

When making investment decisions, many investors don’t seem to place nearly enough importance on a company’s top management team. Not adequately assessing the quality of a company’s top management team before you invest is often a huge mistake, especially in the technology space, because it rapidly evolves.

Who do I mean by “top management team?” Mainly the company’s CEO and CFO, though in some industries, the chief operating officer (COO) and chief technology officer (CTO) can be nearly as important.

Ascertaining the “quality” (capability and integrity) of a top management team involves a fair amount of subjectivity. To some degree, this skill can be learned and improved.

I own Nvidia (NVDA 4.43%) stock and closely follow the leading maker of artificial intelligence (AI) chips and infrastructure. Co-founder and CEO Jensen Huang and CFO Colette Kress are huge reasons I bought the stock.

Today’s Change

(-4.43%) $-8.20

Current Price

$176.69

Key Data Points

Market Cap

$4.3T

Day’s Range

$176.56 – $182.58

52wk Range

$86.62 – $212.19

Volume

11M

Avg Vol

174M

Gross Margin

71.07%

Dividend Yield

0.02%

They run a tight ship, as I could tell from my first couple of quarterly earnings calls, which are excellent. The calls start on time, Kress gives a terrific overview of the quarter and guidance, and neither Huang nor Kress dodges questions, as is pretty typical on other companies’ earnings calls. I’m not easily impressed, but I’m impressed by both of them.

Moreover, there have been no “accounting issues” under Kress’s leadership of the finance team, according to my research. Kress has been CFO since 2013.

Below are some specific ways to gauge the quality of a top management team.

Rule 1A: Favor stocks of founder-led companies

Studies show that founder-led companies tend to outperform the market over the long term. Indeed, there is some evidence that this advantage persists even after the founder leaves the CEO role.

With this in mind, some top tech companies that are currently run by one of their founders include:

- Nvidia (Huang)

- Palantir Technologies (PLTR +0.92%), an AI-powered data analytics company, is led by co-founder Alex Karp.

I’m also going to call out Netflix (NFLX +14.03%). While a founder no longer leads the video-streaming leader, it has a relatively recent history of being founder-led, and one of its co-founders is chairman of the board. Co-founder Marc Randolph was CEO from 1997 to 1999, followed by co-founder Reed Hastings from 1999 to 2023. Hastings now serves as the board’s chairman.

Today’s Change

(14.03%) $11.87

Current Price

$96.45

Key Data Points

Market Cap

$406B

Day’s Range

$90.58 – $96.74

52wk Range

$75.01 – $134.12

Volume

7.3M

Avg Vol

50M

Gross Margin

48.59%

Rule 1B: Be wary of companies with instances of “accounting issues”

Should one minor instance of “accounting issues” keep you from investing in a stock? No, not in my opinion. We’re all human, and people make mistakes. One company I’d put in this category is Symbotic, a robotics company focused on automation for facilities such as fulfillment centers. A little over a year ago, the company had to restate some results. I sense that the accounting errors (which were not egregious, in my view) were inadvertent and due to the transition in the CFO role during a period of rapid growth.

But once a company has multiple instances of accounting issues or a single one attributed to fraud (or seemingly attributed to fraud), I’d shun its stock. To make sound investment decisions, you need to be able to trust that you’re getting accurate data from management.

Accounting issues can broadly be divided into two categories — those that were accidental and those that were intentional to make the company’s results look better. We can think of the former as carelessness, perhaps caused by a lack of adequate financial staff, and think of the latter as fraud. Indeed, fraud is worse, but carelessness is also cause for concern.

Oftentimes, investors can’t distinguish between fraud and carelessness. And it’s challenging for the Securities & Exchange Commission (SEC) to prove fraud, so a fair amount of accounting fraud likely goes undetected or, at least, unpunished, in my opinion.

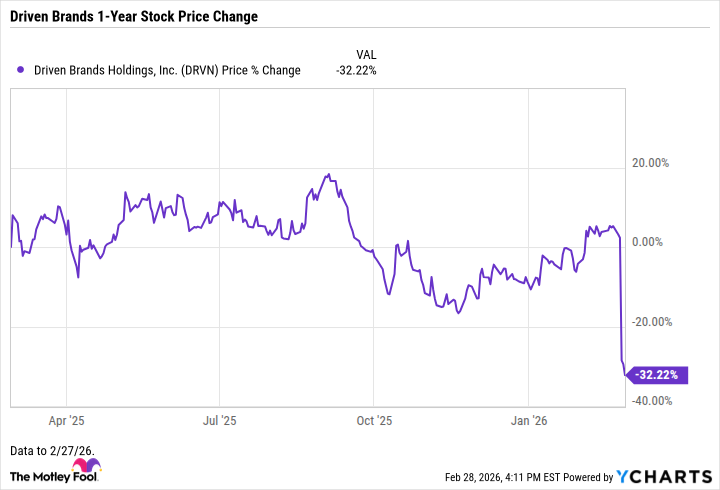

Just last week, the market showed the fury investors will often unleash when a company announces it will be restating its results, especially for a significant period. Shares of Driven Brands, the largest automotive services company in North America, plunged more than 30% following such a disclosure.

Data by YCharts.

The takeaway? Do a search, something like this, as part of your screening process before buying a stock: “[Company name] accounting issues restate financial results.”

Rule 1C: Favor stocks where insiders have considerable ownership

When a CEO and other top management team members, along with other insiders, own a significant number of shares of their company’s stock, their interests are more likely to align with those of shareholders. Nvidia passes this guideline with flying colors.

Rule 1D: Favor stocks of tech companies led by someone with a significant tech background

In general, I want to see tech companies led by people with a strong technical background. I want to see people with degrees in engineering, computer science, physics, or the like leading companies that operate in highly technical fields.

Nvidia’s Jensen Huang, arguably the best tech CEO in recent years, is my poster boy again here. Huang founded Nvidia in 1993, after earning a master’s degree in electrical engineering from Stanford and working as a microprocessor designer at chipmaker Advanced Micro Devices (AMD), now Nvidia’s primary rival.

Could someone with only a business or other non-technical background fully understand how to design a microprocessor, a category that includes Nvidia’s graphics processing units (GPUs)? It’s doubtful, in my opinion. I believe Huang and his company have a competitive advantage over rivals run by people who aren’t as intimately familiar with the technical work their staff perform.

Rule 2: Do not buy stocks in companies that you’d be ashamed to own or work for

I know this guideline might sound too idealistic for some people, but there is a reason beyond idealism for this “rule.” Oftentimes, poor or questionable judgment or behavior by a top management team will catch up with a company and its stock. Like a good mystery novel, there are usually “clues” before a stock plunges.

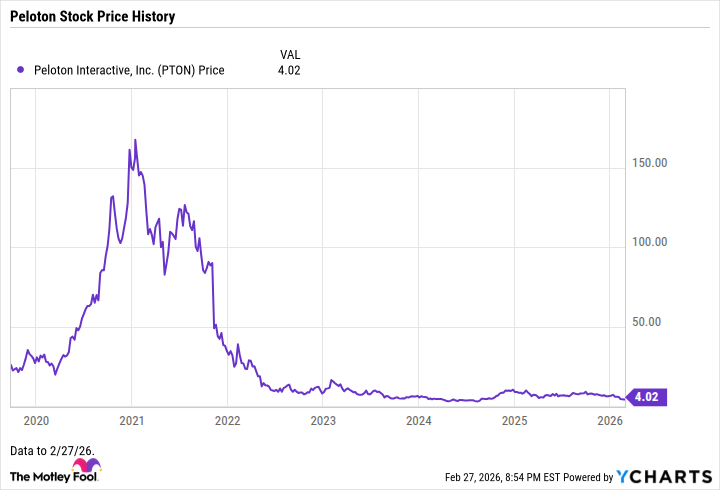

Several examples in this category come to mind. I’ll use connected-fitness company Peloton Interactive (PTON 1.59%), which was flying high during the early stages of the pandemic and has since come crashing down to Earth.

Data by YCharts.

In May 2021, Peloton’s founder and former CEO not only aggressively pushed back against a federal agency’s recommendation to recall its treadmills but also did so in a tone best described as indignation. Mind you, by that time, these machines had injured at least 70 people, some very seriously, and had caused the death of one child.

Would I have been proud to own a Peloton machine (a connected stationary bike or treadmill) or to work for Peloton after this incident? Certainly not. Sticking to my “rule” here would have involved selling the stock if I had owned it after witnessing not just poor but very poor judgment by the then-CEO. This would have been a smart move, as you can glean from the above chart.

(Yes, Peloton was and still is a recommendation in at least one Motley Fool subscription newsletter, as the disclosure below shows. And while The Motley Fool’s analysts have an excellent long-term track record, not every pick will be a winner. I could be proven wrong, but I do not think Peloton stock will ever come close to approaching its all-time high.)

Rule 3: Listen to earnings conference calls

It pays to listen to quarterly or earnings calls or at least read or scan the transcripts, in my opinion. This is more true with some companies than others. In some cases, you will learn information that most investors, at least non-institutional investors, do not know.

Rule 4: Pay much attention to cash flows

In my view, the biggest mistake everyday investors make with respect to quantitative metrics is paying insufficient attention to a company’s cash flows. Institutional investors, however, are very attuned to cash flows. Cash flows are of two main types:

- Operating cash flow — This is the cash a company generates from running its business. It’s sometimes called cash from operations.

- Free cash flow (FCF) — FCF is derived from subtracting capital expenditures (often called capex) from operating cash flow. Capex involves spending on “property, plant, and equipment,” a category under “investing activities” on a company’s Cash Flow Statement. (Companies that pay dividends use their FCF to pay their dividends.)

Always keep in mind that net income — or “earnings” — is merely an accounting metric. It often differs, sometimes considerably, from a company’s cash flows. Cash flows can vary over the short term for all sorts of good reasons, but over the long term, they are more meaningful than net income, in my view. Cash generation is the real McCoy of profitability.

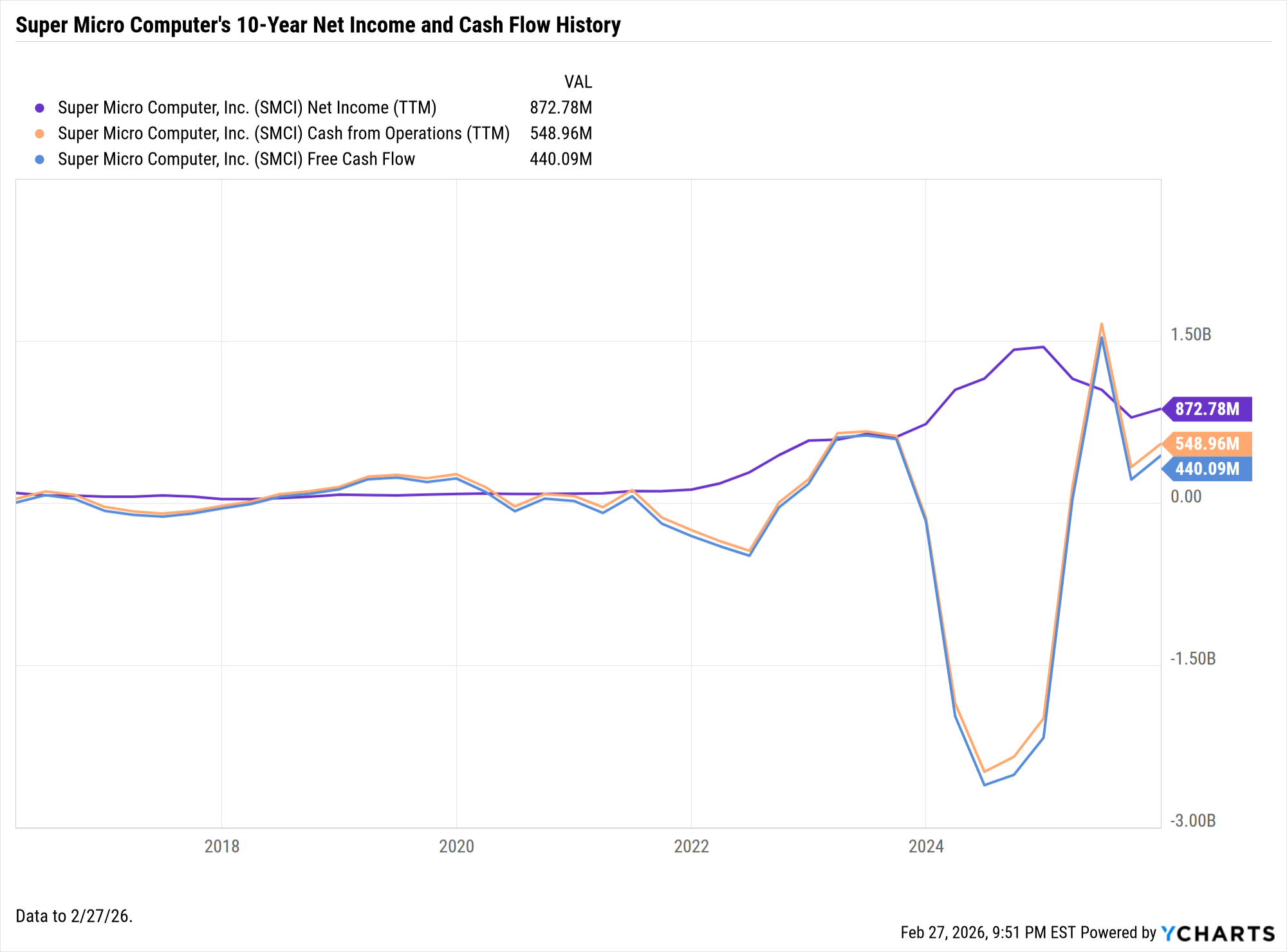

What do you generally not want to see? A company that consistently reports much higher net income than it does cash generated from operations and free cash flow (FCF) over a more than brief period. This might be a sign of accounting “irregularities” or at least what’s called “aggressive accounting.” At any rate, such a scenario means you must investigate further to determine why cash flows are so much less than net income. The Super Micro Computer (SMCI +0.34%) chart below fits this scenario.

Let’s run through some examples.

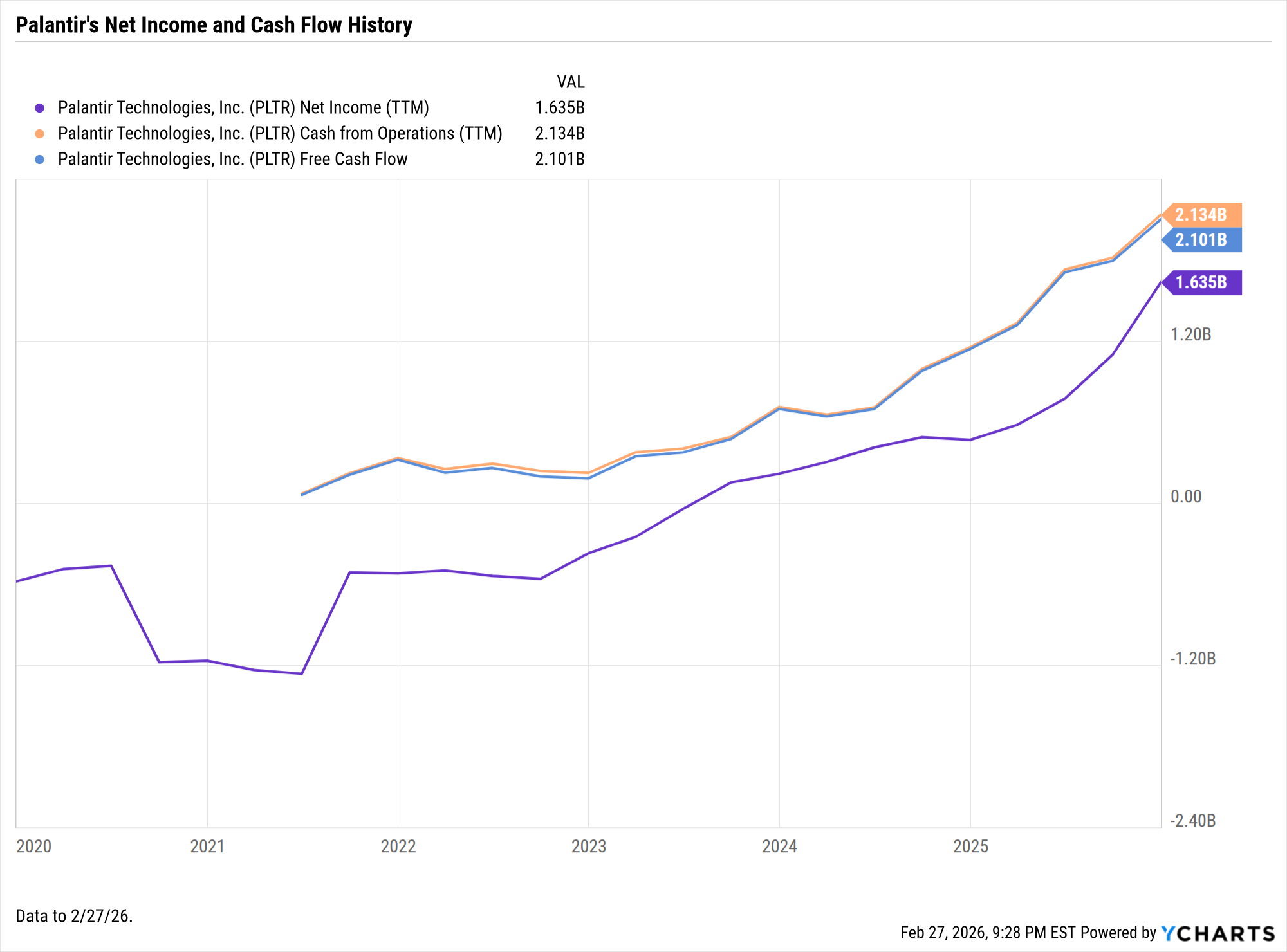

Data by YCharts.

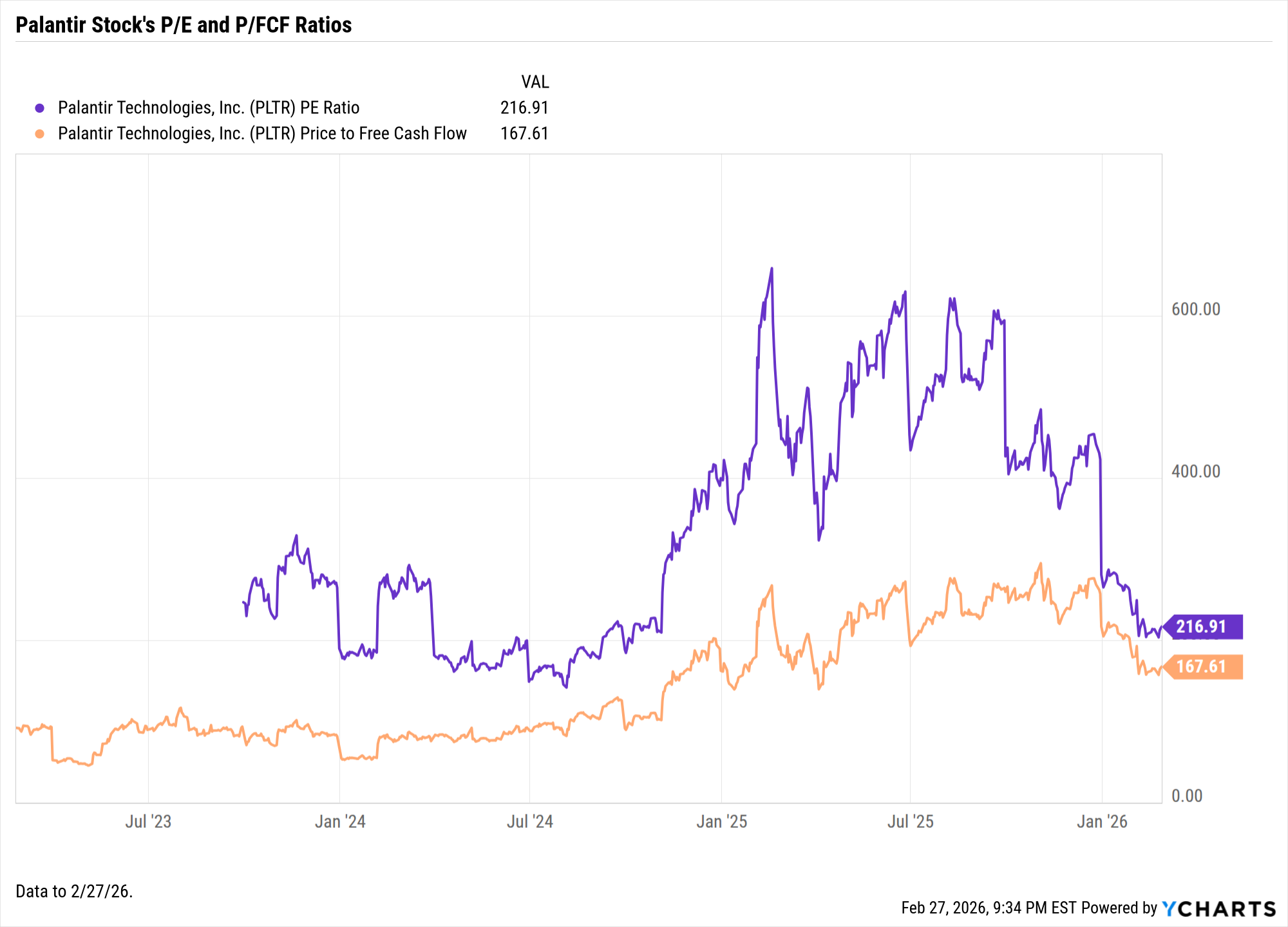

Panatir’s chart above tells us two main things. First, the company’s cash flows — operating cash flow and FCF — have been positive since at least mid-2021, even though its net income — or “earnings” — on a trailing-1-year basis was negative until mid-2023. When a company’s cash flows turn consistently positive, its net income often isn’t far behind. Those who invested in Palantir stock early on, based on its positive cash flows, have been extremely well rewarded.

The second thing this chart tells us is that Palantir’s stock valuation is not as sky-high as many investors believe, because most investors rely on the price-to-earnings (P/E) ratio as their sole valuation metric. The price-to-free cash flow (P/FCF) metric is only about 78% of the P/E ratio. That’s because the trailing-1-year net income is about 78% of the FCF. Below is the chart showing this:

Data by YCharts.

A P/FCF of about 168 is still sky-high, but it’s considerably lower than the P/E of 217.

Now, to Super Micro Computer …

Data by YCharts.

This chart should make you exclaim, “Whoa, what happened during that period starting in late 2023!?”

This is a steroid-upped version of the opposite of the Palantir scenario. Not only were cash flows (both operating and FCF) significantly less than net income for some time, but cash flows were negative while net income was positive.

I guess that many everyday (or “retail”) investors had no idea Supermicro was burning cash while reporting positive net income and earnings per share (EPS) for multiple quarters. I don’t think most investors even glance at a company’s Cash Flow Statement when quarterly results are released, as they should.

Now, this scenario doesn’t necessarily mean Supermicro did anything wrong with respect to its accounting. BUT a scenario like this definitely means investors need to investigate further to identify the reasons for the significant discrepancy between cash flows and net income.

I glanced at Supermicro’s Cash Flow Statements for the period in question. The bulk of the discrepancy was due to the company significantly increasing its working capital and inventory to meet the growing demand for its AI-optimized servers. Accounts receivable (money owed to it by customers for products delivered on credit) also ballooned.

These are adequate reasons, but only if they don’t last too long. It’s better to invest in companies that can use their positive cash flows to fuel their growth, rather than those that need to rely on financing or issuing more stock, which dilutes existing shareholders.

On a related note, Supermicro stock would be a “non-starter” for me anyway. The company and its former CFO were fined by the SEC in 2020 to settle charges of “widespread accounting violations” that the agency said occurred for at least three fiscal years. Moreover, its profit margin is slim and has been shrinking.

The most essential tips in this article?

This is a long article. If you just heed two of the “rules” — No. 1 (paying much more attention to top management quality) and No. 4 (paying attention to cash flows) — I believe you will have an edge over most everyday investors.