Report Overview

The Global Banking Mini Apps Platform Market generated USD 2.3 billion in 2024 and is predicted to register growth from USD 2.9 billion in 2025 to about USD 20.8 billion by 2034, recording a CAGR of 24.4% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 35.3% share, holding USD 0.8 Billion revenue.

The banking mini apps platform market focuses on lightweight apps that sit inside a main banking or super app and handle specific tasks like payments, savings, lending, or insurance. These platforms let banks and fintechs offer multiple focused services in a single interface, instead of pushing users to download many separate applications.

With around 1.75 billion digital banking accounts globally and over 76% of US customers using mobile banking, mini app platforms are becoming a key way to keep users engaged while keeping apps lean and easy to navigate. Growth is driven by rising use of super apps that bundle services such as banking, shopping, mobility, and lifestyle, especially in Asia, Africa, and Latin America.

A core driver is embedded finance, where financial tools like wallets, cards, and lending are built inside non-bank platforms, supported by open banking APIs and banking as a service. Embedded banking transactions already count billions of contactless payments each year in markets like the UK, while banks that embrace digital platforms report operating cost reductions of 20% to 40%, making modular mini app architectures attractive.

Top Market Takeaways

- Platform solutions dominated the market with a 77.4% share, driven by rising demand for integrated mini-app ecosystems inside banking environments.

- On-premises deployment accounted for 62.6%, reflecting strong preference for data control and security within financial institutions.

- Retail banking led with 40.5%, supported by high adoption of mini-apps for payments, onboarding, and personalized services.

- Banks remained the primary end-users with 38.5% share, as institutions expand their digital service portfolios.

- North America captured 35.3% of global revenue, supported by strong digital banking penetration.

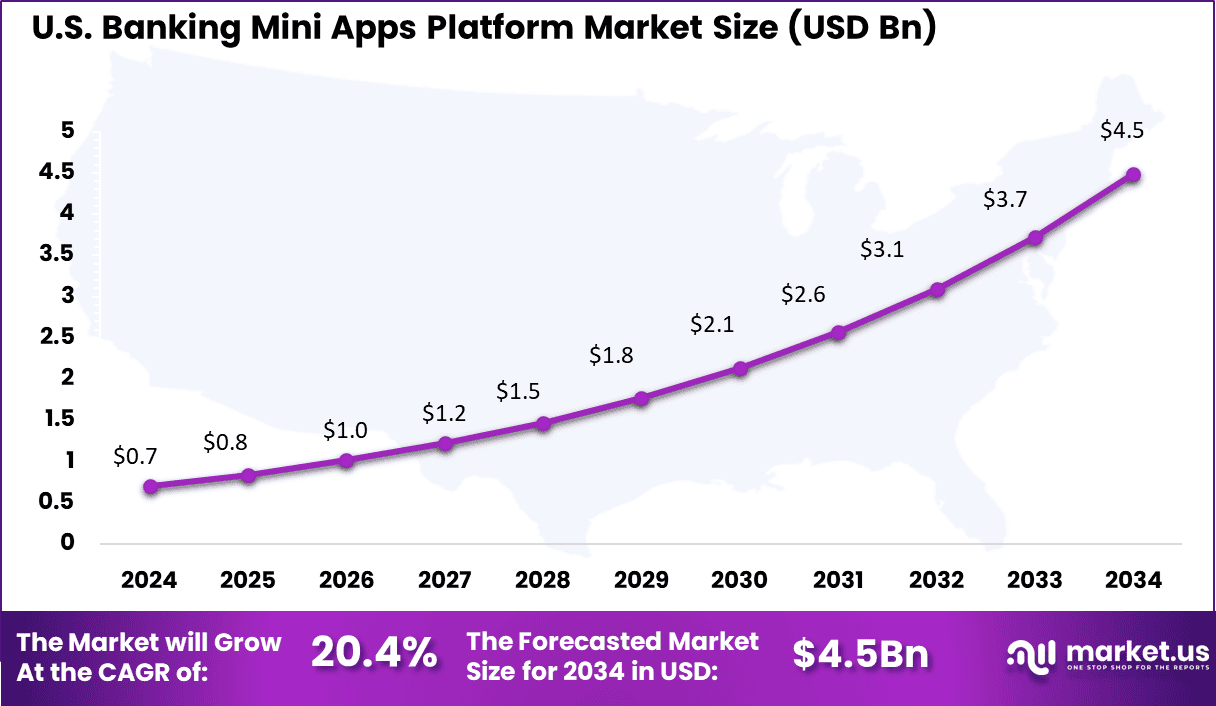

- The U.S. market reached USD 0.70 billion, growing at a 20.4% CAGR, driven by active adoption of embedded mini-app frameworks across major banking platforms.

Quick Facts

Platform and Adoption Statistics

- Around 50% of institutions are exploring super app experiences for SMEs.

- About 25% of institutions have already started bundling multiple services into unified platforms.

- SME users show strong interest in apps that aggregate accounts from different financial providers for a complete financial view.

Market and User Statistics

- Digital payments made up 99.8% of all transaction volume in India in the first half of 2025.

- Gen Z (64%) and Millennials (60%) rely heavily on mobile banking as their main channel.

- Neobanks generated $39.5 billion in revenue in 2024, with NuBank leading at 114 million users.

- Cryptocurrency app downloads rose 133%, reaching 400 million in the first three quarters of 2024.

User Experience and Feature Statistics

- Banking apps maintain strong retention with an 85% 30-day retention rate and a 78% 90-day retention rate.

- Apps rated 4 stars or higher are 89% more likely to be downloaded.

- Users want improved search and filtering tools for transaction histories.

- Security remains critical, with demand for secure APIs, SSO, and strong authentication in mini-app environments.

By Component: Platform

In 2024, the platform segment held 77.4% share in the banking mini apps platform market. Platforms form the backbone of banking mini apps, handling core functions like building, deploying, and managing lightweight apps within banking ecosystems. They let banks roll out new features quickly based on customer input and changing needs.

This setup supports modular tools that integrate smoothly with existing systems for better service delivery.Banks rely on these platforms to create user-friendly experiences, such as single-purpose apps for quick tasks like payments or account checks. The focus stays on flexibility, allowing updates without full system overhauls. Overall, platforms drive efficiency by enabling rapid testing and refinement of digital offerings.

By Deployment Mode: On-Premises

In 2024, the on-premises segment accounted for 62.6% share in the banking mini apps platform market. On-premises setups give banks full control over their mini apps infrastructure, keeping data and operations in-house for security and compliance. This approach suits institutions with strict rules on data location and custom needs.

It avoids reliance on external providers, ensuring steady performance during peak times. Many banks choose this mode to tailor systems exactly to their workflows, with in-house teams handling maintenance and tweaks. Hybrid options blend it with cloud for less critical tasks, balancing control and agility. The result is reliable handling of sensitive operations without third-party risks.

By Application: Retail Banking

In 2024, the retail banking application segment captured 40.5% share in the banking mini apps platform market. Retail banking leads in mini apps use, focusing on everyday consumer needs like balance checks, transfers, and bill pays through simple mobile interfaces. Customers expect seamless access anytime, and these apps deliver with features like personalized alerts and quick onboarding. This keeps users engaged without full app downloads.

Apps here emphasize convenience for individuals and families, including budgeting tools and shared accounts. They turn banking into a daily companion by embedding finance into mobile habits. Banks gain loyalty through tailored journeys that fit modern lifestyles.

By End-User: Banks

In 2024, banks as end-users represented 38.5% share in the banking mini apps platform market. Banks as primary users build mini apps to modernize services, embedding them in their own platforms for direct customer reach. This internal focus speeds up innovation while meeting regulatory standards. It strengthens core operations like payments and account management.

These end-users prioritize apps that boost engagement and cut costs through self-service options. Control over the full stack lets them customize for specific markets. The shift enhances competitiveness in a digital-first world.

US Market Size

In 2024, the U.S. market for banking mini apps platforms reached USD 0.70 Bn with a CAGR of 20.4%. The U.S. stands out with mature digital banking habits, where mobile apps handle most daily transactions. Strong networks and user trust fuel quick uptake of mini apps for tasks like payments and alerts.

In 2024, North America held 35.3% share in the banking mini apps platform market. North America drives mini apps growth with high smartphone use and demand for anytime banking. Tech-savvy users push for connected experiences via open APIs and mobile-first designs. Regions like the U.S. see strong adoption due to advanced infrastructure.

Digital trends here favor personalization and instant services, with banks linking accounts to third-party tools. Cities with young populations lead in mobile transactions. This environment supports fast evolution of lightweight banking solutions.

Emerging Trends

Banks now build mini apps right into their main platforms to offer quick services like payments and loans without extra downloads. This setup lets users handle everything in one place, from checking balances to getting advice on spending. Cloud options make it easy to roll out updates fast, keeping services fresh as customer needs change.

Open banking rules push platforms to connect with outside apps for better tools, such as budgeting or insurance checks. Retail users lead this shift, wanting smooth experiences across devices. Asia sees the biggest jump, with mobile-first crowds driving super app ideas that mix finance and daily tasks.

Growth Factors

Digital shifts make banks drop old systems for flexible mini apps that cut costs and speed up new features. Customers expect on-demand access, so platforms help meet that with simple setups for personal finance tools. Rules supporting open access open doors for banks to team up with tech firms.

Rising smartphone use in growing markets pulls more people into digital banking, where mini apps bridge gaps for those without branches nearby. Focus on retail pulls in everyday users who stay longer with handy services. Strong demand for easy, safe options keeps platforms expanding steadily.

Key Market Segments

By Component

By Deployment Mode

By Application

- Retail Banking

- Corporate Banking

- Investment Banking

- Others

By End-User

- Banks

- Credit Unions

- Fintech Companies

- Others

Regional Analysis and Coverage

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver Analysis

Customer demand for instant banking services fuels growth in mini apps platforms. Users want to pay bills, transfer money, or check loans without leaving their main chat or super apps like WeChat or WhatsApp. Banks gain by embedding services this way, cutting the need for separate downloads that many skip. This keeps users engaged longer on one platform.

Lower costs help too. Building full apps takes time and money, but mini apps use existing frameworks. Banks save on development and updates while reaching young users who prefer light apps. Loyalty rises as people handle all finance in familiar spots, boosting transaction volumes.

Restraint Analysis

Tight rules on data and money handling hold back mini apps rollout. Each country sets strict standards for security and privacy, forcing banks to test every change. Delays pile up from approvals, raising expenses for smaller players who struggle to keep pace.

Legacy systems add friction. Many banks run old tech that does not link well with modern mini apps. Integrating them means big upgrades, which scare off firms with tight budgets. This slows feature launches and leaves gaps versus agile fintech rivals.

Opportunity Analysis

Teams with banks and fintech firms spark new growth paths. Startups bring fresh ideas for tools like quick loans or savings plans that plug into bank systems. Banks expand reach without full overhauls, tapping into partner user bases for more signups.

Open banking rules create more room. Standards let platforms connect third-party services safely, adding value like investment tips or bill splits. Users get one-stop finance hubs, drawing crowds from scattered apps. This mix promises steady revenue from fees and data insights.

Challenge Analysis

Security risks loom large with money data in mini apps. Hackers target weak spots in shared platforms or public logins, leading to breaches that hit trust hard. Banks must layer defenses like encryption and checks, yet keep apps fast for daily use.

Fraud and compliance woes grow too. Real-time threats demand constant monitoring, but false alerts annoy users. Meeting varied global rules drains resources, with fines waiting for slips. Balancing safety and ease stays a daily fight for providers.

Competitive Analysis

HSBC, JPMorgan Chase, Bank of America, Wells Fargo, and Citibank lead the banking mini apps platform market with strong digital ecosystems that embed financial services directly into mobile interfaces. Their platforms support account management, payments, budgeting tools, and personalized insights within compact, fast-loading app modules.

Barclays, Deutsche Bank, BNP Paribas, Santander, UBS, ING Group, Standard Chartered, Goldman Sachs, and Morgan Stanley strengthen the competitive landscape by integrating mini apps for wealth management, lending, insurance, and cross-border transactions. Their solutions support seamless onboarding, automated advisory, and secure in-app workflows.

Royal Bank of Canada, TD Bank Group, BBVA, Societe Generale, ICICI Bank, DBS Bank, and other players expand the market with flexible mini app frameworks tailored for emerging financial services. Their platforms offer micro-investing, savings automation, loyalty features, and hyper-personalized financial journeys. These providers focus on rapid feature deployment, API-driven innovation, and strong mobile UX.

Top Key Players in the Market

- HSBC

- JPMorgan Chase

- Bank of America

- Wells Fargo

- Citibank

- Barclays

- Deutsche Bank

- BNP Paribas

- Santander

- UBS

- ING Group

- Standard Chartered

- Goldman Sachs

- Morgan Stanley

- Royal Bank of Canada

- TD Bank Group

- BBVA

- Societe Generale

- ICICI Bank

- DBS Bank

- Others

Recent Developments

- October, 2025 – HSBC teamed up with Juspay to roll out a full-stack acquiring platform aimed at digital merchants. This move pulls together payments and processing into one smooth system, boosting success rates and reliability for global users.

- September, 2025 – JPMorgan Chase pushed ahead with its Chase digital banking platform by launching in Germany. The rollout offers a simple app-based account with savings tools and quick payments, drawing from its UK success to grab retail customers.