LONDON, Nov 24 (Reuters) – What matters in U.S. and global markets today

U.S. stocks look set to build on Friday’s jump with investor hopes resting on a Fed rate cut materialising in December, but the question is how much further prices can bounce?

Sign up here.

Today’s Market Minute

- The United States and Ukraine were set to continue work on Monday on a plan to end the war with Russia after agreeing to modify an earlier proposal that was widely seen as too favorable to Moscow. The two sides said in a joint statement they had drafted a “refined peace framework.”

- BHP should move on from Anglo American and focus on its growth strategy, investors said on Monday, after the Australian company’s last-minute appeal to the London-listed firm that is nearing a $60 billion tie-up with Canada’s Teck Resources.

- U.S. President Donald Trump’s Department of Government Efficiency has disbanded with eight months left to its mandate, ending an initiative launched with fanfare as a symbol of Trump’s pledge to slash the government’s size but which critics say delivered few measurable savings.

- Oil prices eased on hopes for a U.S.-brokered Ukraine ceasefire, but diesel spreads remain stubbornly high as the war keeps global supplies squeezed with little sign of relief, writes Energy Columnist Ron Bousso.

- The weak COP30 statement that omitted any mention of fossil fuels was probably the best outcome that could have been realistically expected of the climate summit, argues ROI Asia commodities columnist Clyde Russell.

Will the Fed come to stock markets’ rescue?

U.S. stocks look set to build on Friday’s jump with all investor hopes resting on a Fed rate cut materialising in December, but the question is how much further they can bounce?

Traders now see a roughly 60% chance that the Fed will cut rates in December, up from around 40% on Thursday.

Yet those futures, which had been up around 1% earlier, have already cut their gains well before the U.S. open. Both indexes are still set for their biggest monthly drops since March, with the Nasdaq still down over 6%.

Besides the concerns around AI valuations that drove that selloff in the first place, optimism around a Fed cut doesn’t change that October and November’s payroll data — key to rates expectations — will only be released after the bank’s December meeting.

U.S. markets will also have to digest retail sales, producer price and jobless claims data this week.

They looked subdued otherwise, with the dollar down 0.2% against a basket of currencies, while Treasury yields were largely steady after sizeable drops last week.

Markets remain on alert for intervention in the Yen by Japanese authorities, who tend to move in quiet periods with lower liquidity. The yen edged lower against the dollar on Monday, nearing last week’s 10-month lows.

European defense stocks, while sitting on huge gains this year, continued to slide on Monday, dropping to their lowest since August.

Geopolitics aside, the big focus is on Britain’s much anticipated Wednesday budget, when finance minister Rachel Reeves will have to convince investors that she can deliver credible belt-tightening plans after U-turning on plans to raise income tax levels.

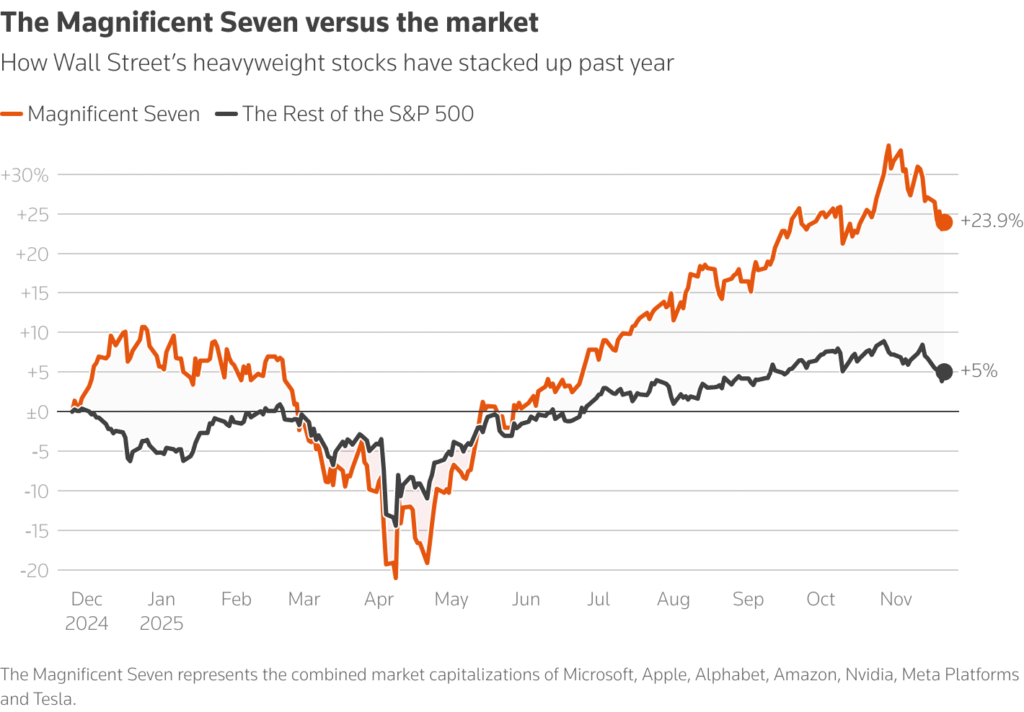

Chart of the day

U.S. equity markets have a long way to come back after last week, still sitting on heavy losses in November that have set them up for their worst monthly performance since March, when tariff worries rattled markets ahead of the big intra-month swing in April.

Today’s events to watch

* Two-year U.S. Treasury auction offering $69 billion

* U.S. corporate earnings include Agilent Technologies, Symbotic Inc, Keysight Technologies, Woodward Inc, Zoom

By Yoruk Bahceli; Editing by Anna Szymanski

Our Standards: The Thomson Reuters Trust Principles., opens new tab

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.