The inauguration of Donald Trump as US President in January 2025 dominated financial markets, delivering both uncertainty and volatility. While equity markets and the US dollar surged following his election win in November, the early days of Trump’s second term have proven unpredictable, causing notable shifts in the foreign exchange (FX) landscape.

Download our Global FX Outlook for February to stay ahead of market shifts and help your business manage currency risks.

A shift in market expectations

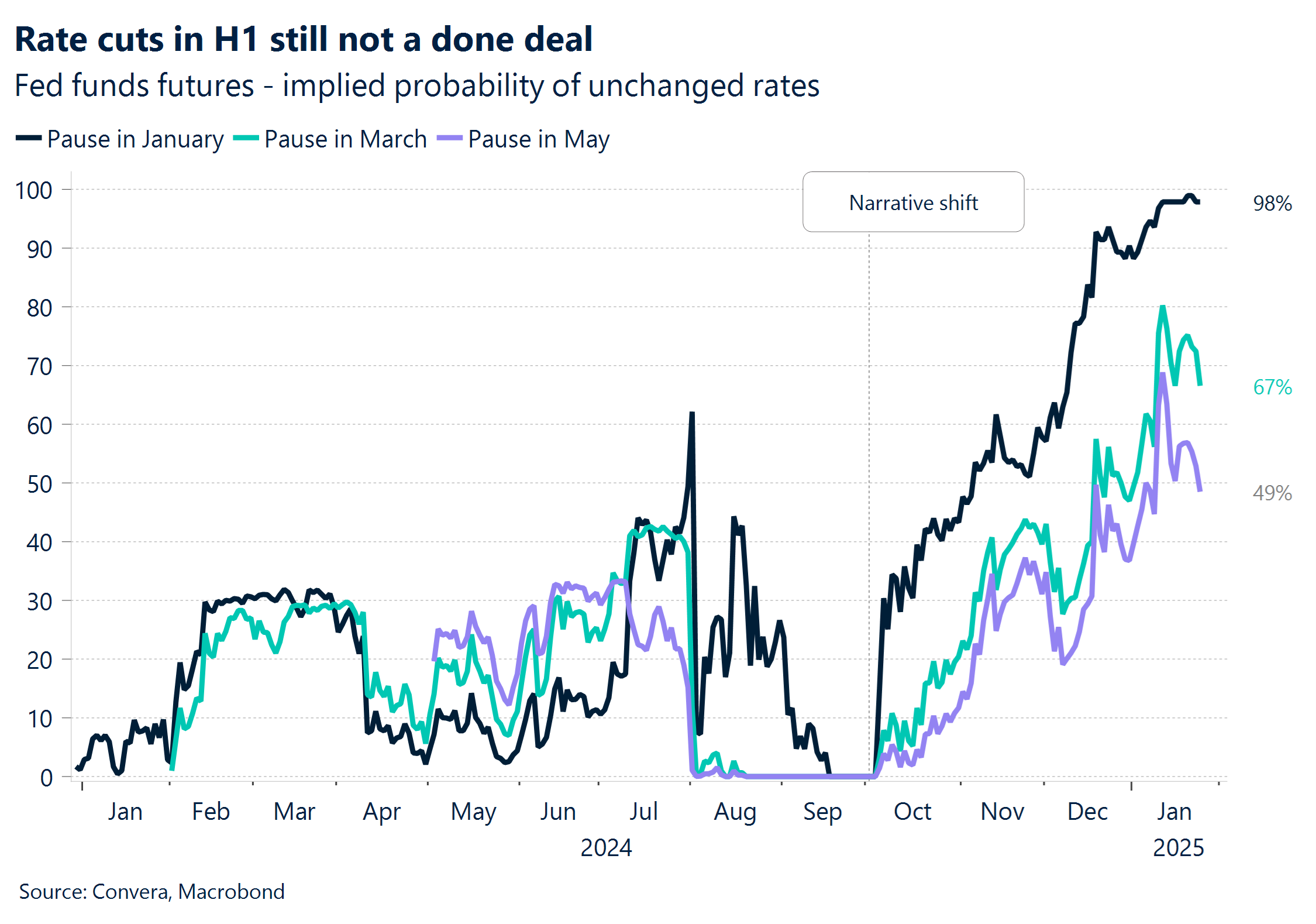

At the beginning of 2024, traders were pricing in the possibility of over six Fed rate cuts for the year. Now, with inflation pressures persisting and the potential for higher US tariffs under President Donald Trump, expectations for monetary easing have been tempered.

Leading up to President Trump’s inauguration, global equity markets experienced steady gains, and the US dollar appreciated by more than 6.0% as investors anticipated pro-growth policies. However, the new administration quickly tempered expectations. While Trump refrained from immediately imposing aggressive new tariffs, he announced a study into “destructive” trade policies and currency manipulation.

The US dollar responded by easing, mirroring moves seen during his first term, while trade-sensitive currencies such as the Australian dollar (AUD) and the euro (EUR) rebounded. Later in the month, Trump reignited tariff threats, reinforcing the ongoing volatility in global markets.

As it stands, markets anticipate just one Fed rate cut in 2025—a stark contrast from the aggressive easing cycle many had hoped for last year. The recalibration of expectations signals a cautious approach from policymakers who must now balance macroeconomic resilience against inflationary risks.

Key FX market movements

In the wake of these political and economic developments, major currency pairs experienced significant fluctuations:

- U.S. dollar (USD): After reaching two-year highs, the USD index fell 2.9%, marking its largest pullback since September, as concerns over extreme trade measures faded.

- Euro (EUR): Following steep post-election losses, the EUR/USD rebounded strongly, posting its biggest weekly rise in over a year (up 2.1%) and breaking above 1.0500 for the first time in six weeks.

- British pound (GBP): The pound suffered sharp declines since October, falling 8.4% against the USD, but staged a late-month recovery from two-year lows.

- Australian dollar (AUD): The AUD ranked last among G10 currencies since October, weighed down by tariff concerns, China’s economic slowdown, and potential Reserve Bank of Australia (RBA) policy shifts. AUD/USD fell to levels last seen in 2020.

Key market themes to watch in foreign exchange

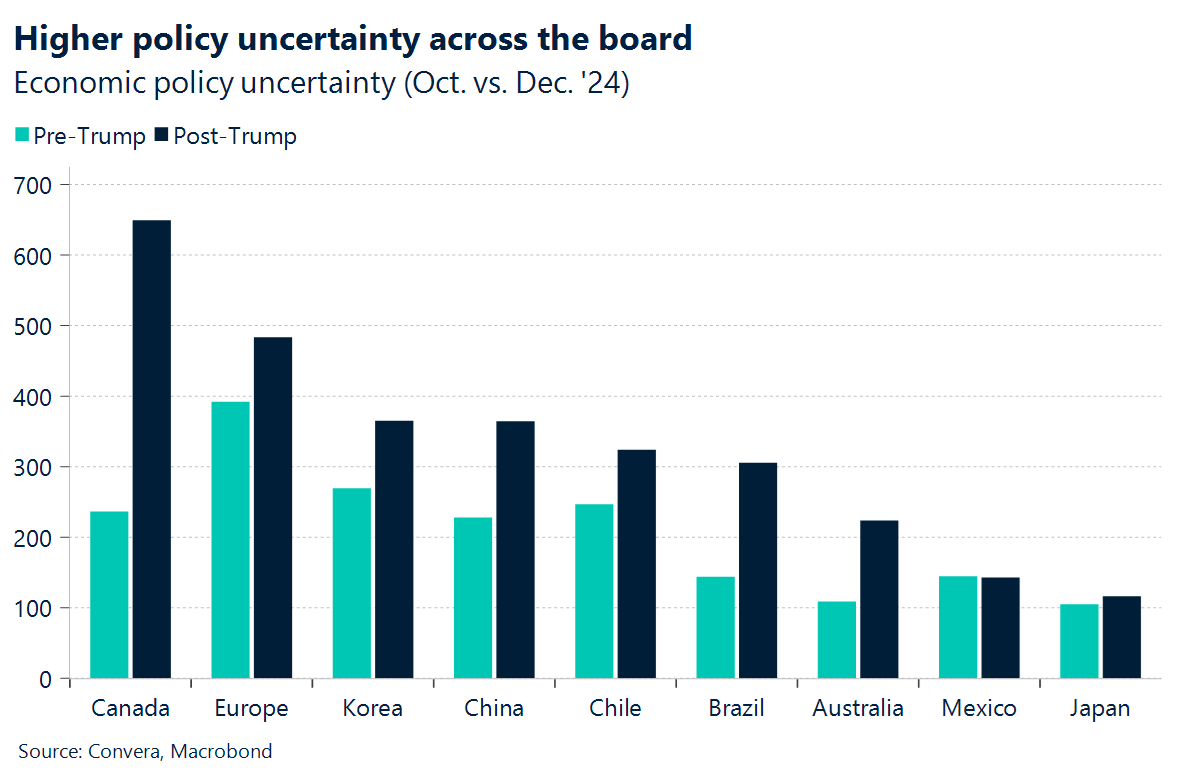

Global uncertainty remains high, with shifting policies and trade tensions driving market volatility. Since Donald Trump’s election, policy unpredictability has surged, reshaping alliances and economic strategies. Investors now navigate an environment where sudden shifts and geopolitical tensions are the norm. Europe, caught between the US and China, faces additional uncertainty, compounded by weak government mandates in its largest economies.

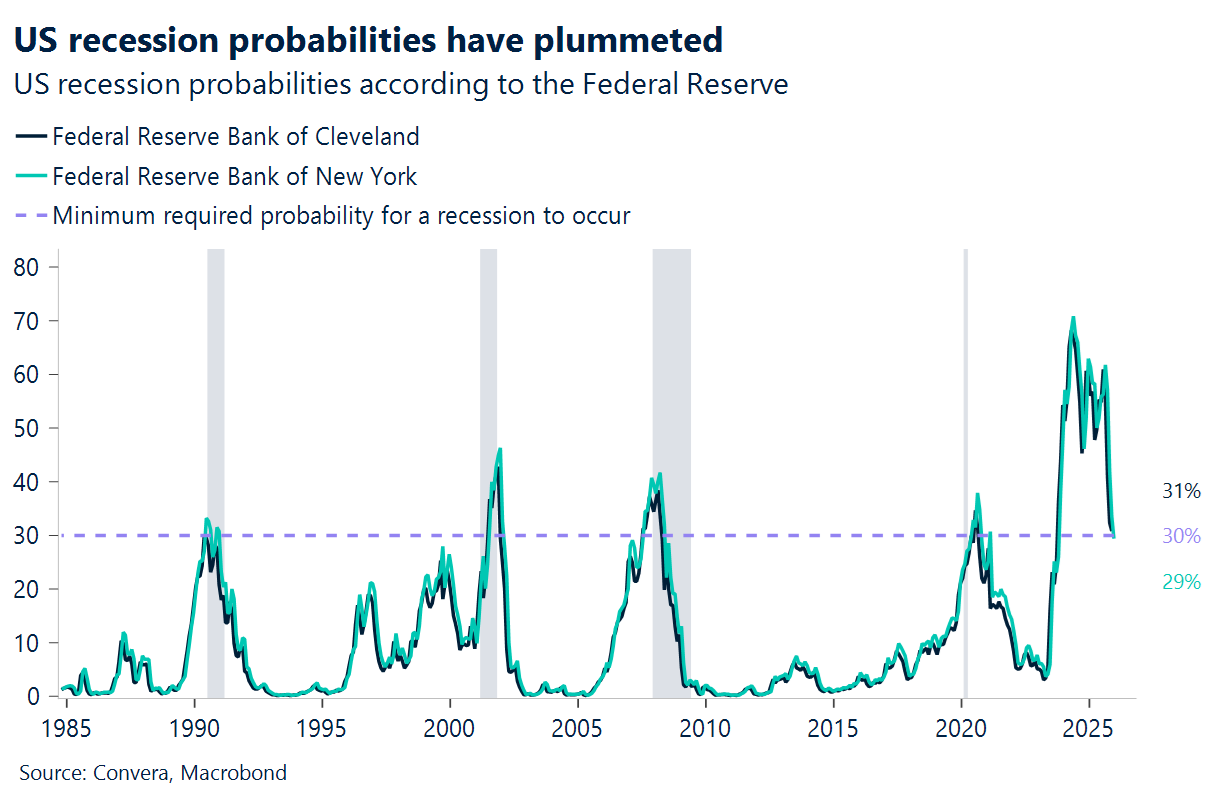

Meanwhile, the US economy continues to defy recession warnings. Despite yield curve inversions, aggressive Fed hikes, and tighter credit conditions, growth has remained resilient. GDP expansion, a strong labor market, and steady consumer spending have postponed any downturn, though risks persist.

In Europe, pessimism may have peaked. Recession fears and geopolitical risks have weighed on sentiment, but market expectations are now so low that even modest economic surprises could spark strong reactions. With growth prospects uncertain, any positive shift in data could drive renewed investor confidence.

Watch an overview of the February outlook

Watch our Market Insights team provide a short summary of the most crucial insights from the February Global FX Outlook and start making informed decisions for your business today.

February’s inflation data: A critical turning point

One of the biggest events shaping the monetary policy debate in early 2025 will be February’s inflation data. As central banks assess their next steps, inflation reports from the US, Eurozone, and UK will set the tone for interest rate decisions.

While the Fed has signaled openness to rate cuts, persistently high inflation in services and wages could stall any aggressive policy moves. Markets will closely watch January’s Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) data to gauge the likelihood of near-term rate cuts.

Both institutions face pressure to ease as growth slows, but sticky inflation remains a hurdle. Any surprises in core inflation data could significantly alter the monetary policy path.

Download the latest Global FX Outlook report now to stay informed on the latest trends in monetary policy and foreign exchange markets.

Want more insights on the topics shaping the future of cross-border payments? Tune in to Converge, with new episodes every Wednesday.

Plus, register for the Daily Market Update to get the latest currency news and FX analysis from our experts directly to your inbox.