3 UK Stocks Estimated To Be Trading At Discounts Of Up To 49.6%

The UK stock market has recently experienced some turbulence, with the FTSE 100 index closing lower due to weak trade data from China, highlighting ongoing challenges in global economic recovery. In this environment, identifying undervalued stocks can be particularly appealing as investors seek opportunities that may offer potential value despite broader market pressures.

Let’s take a closer look at a couple of our picks from the screened companies.

Overview: CAB Payments Holdings Limited, with a market cap of £219.85 million, offers foreign exchange and cross-border payment services to banks, fintech companies, supranationals, and governments both in the United Kingdom and internationally.

Operations: The company’s revenue is primarily derived from providing foreign exchange and cross-border payment services, totaling £86.08 million.

Estimated Discount To Fair Value: 24%

CAB Payments Holdings is trading at £0.87, significantly below its estimated future cash flow value of £1.14, indicating potential undervaluation based on discounted cash flow analysis. Despite recent volatility and insider selling, CAB’s earnings are projected to grow 24.74% annually over the next three years, outpacing the UK market average growth rate of 11.9%. Recent strategic partnerships and regulatory approvals further bolster its operational capabilities and potential for future growth in emerging markets.

LSE:CABP Discounted Cash Flow as at Apr 2026

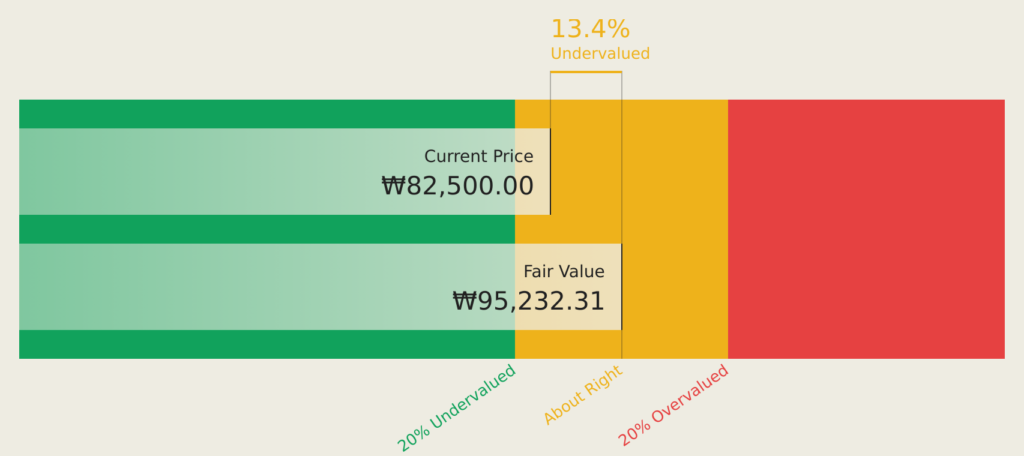

Overview: M&G plc, with a market cap of £6.93 billion, offers investment and savings products to both institutional clients and individual policyholders in the UK and internationally through its subsidiaries.

Operations: The company’s revenue is primarily derived from its Asset Management segment, contributing £4.59 billion, and its Life (including Wealth) segment, which adds £899 million.

Estimated Discount To Fair Value: 46.2%

M&G is trading at £2.91, considerably below its estimated future cash flow value of £5.4, highlighting potential undervaluation. Despite a dividend yield of 7.05% that isn’t fully covered by earnings, M&G’s profitability has improved with net income reaching £302 million in 2025 from a loss the previous year. The recent acquisition of a 15% stake by Dai-ichi Life Holdings could enhance strategic positioning, while forecasted annual earnings growth of over 31% suggests robust financial prospects ahead.

LSE:MNG Discounted Cash Flow as at Apr 2026

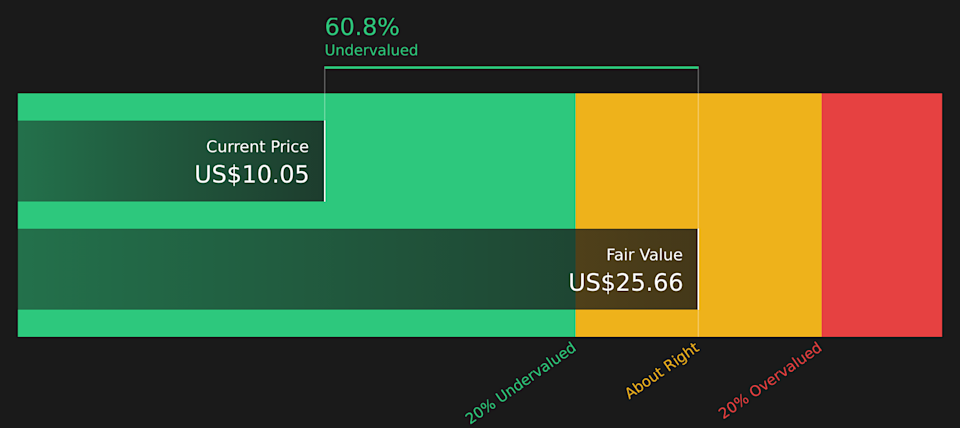

Overview: RHI Magnesita N.V. is a company that develops, produces, sells, installs, and maintains refractory products and systems for industrial high-temperature processes globally, with a market cap of approximately £1.25 billion.

Operations: The company’s revenue segments are distributed across several regions, with €441 million from India, €80 million from Minerals, €727 million from Europe & CIS, €536 million from Latin America, €863 million from North America, €377 million from China & East Asia, and €342 million from the Middle East, Türkiye & Africa.

Estimated Discount To Fair Value: 49.6%

RHI Magnesita is trading at £26.45, significantly below its estimated future cash flow value of £52.43, indicating potential undervaluation. Despite a high debt level and declining profit margins from 4.1% to 2.6%, earnings are forecasted to grow substantially at 26.2% annually over the next three years, outpacing the UK market’s growth rate of 11.9%. The company is also pursuing strategic acquisitions without expecting significant cash outflows in 2026, potentially bolstering long-term growth prospects.

LSE:RHIM Discounted Cash Flow as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LSE:CABP LSE:MNG and LSE:RHIM.

This article was originally published by Simply Wall St.

The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 index closing lower due to weak trade data from China, highlighting the interconnectedness of global economies. For investors seeking opportunities outside of large-cap stocks, penny stocks—despite their somewhat outdated name—can still present valuable prospects. By focusing on companies with strong financial foundations

The “Magnificent Seven” tech stocks have been major drivers of growth in the U.S. stock market for the past several years. What if you could own all seven stocks in a single tech ETF? You can. The Roundhill Magnificent Seven ETF (NYSEMKT: MAGS) gives you one-stop shopping for seven of the most prominent tech stocks.

As global markets react to easing geopolitical tensions, investor sentiment in Asia has been buoyed by optimism around potential de-escalation and economic resilience. In this environment, identifying undervalued stocks becomes crucial, as they may offer opportunities for growth amid broader market recoveries. Top 10 Undervalued Stocks Based On Cash Flows In Asia Name Current Price

The Australian stock market is experiencing a turbulent period, with geopolitical tensions impacting investor sentiment and causing fluctuations in major indices. In such uncertain times, investors often look to alternative opportunities for potential growth. Penny stocks, despite their outdated name, continue to represent a promising investment area by offering access to smaller or newer companies

Market Closed – Nasdaq Copenhagen 11:20:00 2026-04-10 am EDT 5-day change 1st Jan Change 95.40 DKK -0.62% -1.65% -11.26% Published on 04/12/2026 at 10:18 pm EDT Publicnow Danish English Published: 2026-04-12 14:04:10 CEST RTX – Changes in company’s own shares Share buy-back programme 12.4.2026 14:04:10 CEST | RTX | Changes in company’s own shares Nørresundby,

Most investors focus on trying to find the market’s next big winners. It may be the more exciting way to approach your investing strategy, but in most cases it’s not the most successful. The better way to build wealth over time is usually building your portfolio brick by brick. By steadily and consistently putting money

Debris of a NATO air defence system that intercepted a missile launched from Iran is seen in Dortyol, in southern Hatay province, Turkey, March 4, 2026 in this screengrab from video. Ihlas News Agency | Via Reuters Asia-Pacific markets opened lower Monday, as investors weigh a U.S. naval blockade on Iran’s ports after talks between

The negotiations between the United States and Iran began at 11:00 AM local time. After three rounds of talks lasting 21 hours, no agreement was reached between the two sides. This week, the earnings reports of major banks will be the highlight on the schedule.$JPMorgan (JPM.US)$ 、 $Wells Fargo & Co (WFC.US)$ 、 $Bank of

Amazon.com, Inc. (NASDAQ:AMZN) is among the stocks Jim Cramer discussed alongside the tech market divide. Cramer discussed the stock in light of the CEO’s annual letter, as he stated: The annual Amazon letter came out today, written by CEO Andy Jassy, and it reminds you of just how stupendous this company really is. I believe

Iran war developments, PPI data, start of Q1 earnings season will be in focus during the week ahead. Netflix is gearing up for a potential breakout as its Q1 earnings loom. Johnson & Johnson faces a likely stumble with a projected earnings dip in the spotlight. U.S. stocks closed mostly lower on Friday, but the

Sunday, April 12, 2026 4:10 PM Photo: By User:Mlang.Finn – Self-photographed, CC0, https://commons.wikimedia.org/w/index.php?curid=113919559 Zak Thomas-Akoo, Next.io Email, LinkedIn, and more The Finnish government has said a public offering of state-owned gambling monopoly Veikkaus Oy remains a possibility, but would not happen until several prerequisites had been met. As previously reported, Finland will become the latest Nordic

Got story updates? Submit your updates here. › The stock market’s resilience in the face of global crises may mask the long-term implications of each event, as the focus on short-term gains overlooks the broader economic impact.Today in Miami The stock market’s resilience in the face of global crises, from the pandemic to the Iran-Israel

The last 10 years have been an excellent run for the stock market. Despite two bear markets (2020 and 2022) and two nearly bear markets (2018 and 2025), the S&P 500 (^GSPC 0.11%) has produced a total return of 282% over the last decade, a compound annual return of 14.4%. That’s well above the historical

Usually, the playbook for when an asset drops 46% from its peak is to stop buying it. Strategy (MSTR 0.17%) — formerly known as MicroStrategy — missed that memo, and the company now holds 766,970 Bitcoin (BTC 2.64%) after purchasing another 4,871 BTC in the first week of April alone, despite the cryptocurrency’s price of $68,536

The first quarter of 2026 has been rough on artificial intelligence (AI) stocks … or has it? On the one hand, share prices of some of the biggest AI stocks, after years of explosive growth, are actually down so far this year. Nvidia (NVDA +2.59%), for example, is down nearly 5% year to date. Today’s

Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St. If you are wondering whether Patterson-UTI Energy is attractively priced at its recent levels, this article walks through what the current share price might mean for you as an investor. The stock recently closed at

For most of President Donald Trump’s tenure in the White House, the stock market has excelled. The widely followed Dow Jones Industrial Average (^DJI 0.56%), benchmark S&P 500 (^GSPC 0.11%), and technology-dominated Nasdaq Composite (^IXIC +0.35%) surged 57%, 70%, and 142%, respectively, during his first term, and were all up by double digits through year

With tens of millions of funded accounts, Robinhood is one of the most popular online brokerages for retail investors. Each month, the company posts the top 10 most-owned stocks on the platform. This list is updated monthly and usually includes large tech and artificial intelligence stocks found in the “Magnificent Seven.” Due to the sell-off

In recent days, Willdan Group has come under scrutiny as new analysis suggested its shares are trading above intrinsic value, alongside reports that insiders sold about US$500,000 of stock over the past three months. This combination of perceived overvaluation and insider selling adds a layer of caution to an otherwise solid operational picture, raising fresh

I feel like it’s time for a confession, so here it is: Not every stock that I love is a winner right now. But I tend to fall hard for companies that I know are solid and will rebound when the time is right. Case in point: During the COVID-19 pandemic, travel restrictions meant nobody