3 Asian Stocks Estimated To Be Trading At Discounts Of Up To 44.2%

As Asian markets navigate the complexities of rising global energy prices and geopolitical tensions, investors are closely monitoring opportunities that may arise from these volatile conditions. In such an environment, identifying undervalued stocks can be key to capitalizing on potential market inefficiencies, particularly those trading at significant discounts relative to their intrinsic value.

Let’s uncover some gems from our specialized screener.

Overview: Guming Holdings Limited is an investment holding company that operates as a freshly made beverage company in the People’s Republic of China, with a market cap of HK$67.64 billion.

Operations: Revenue Segments (in millions of CN¥):

Estimated Discount To Fair Value: 28.9%

Guming Holdings is trading at 28.9% below its estimated fair value, with shares priced at HK$28.44 compared to a future cash flow value of HK$40. The company reported significant earnings growth of 110.3% last year, and future earnings are forecasted to grow faster than the Hong Kong market at 13.8% annually. Recent inclusion in the FTSE All-World Index and a proposed dividend payment further highlight its potential as an undervalued stock based on cash flows in Asia.

SEHK:1364 Discounted Cash Flow as at Apr 2026

Overview: Keymed Biosciences Inc. is a biotechnology company focused on discovering and developing biological therapies for autoimmune and oncology conditions in Mainland China and internationally, with a market cap of HK$19.74 billion.

Operations: Keymed Biosciences Inc. generates revenue through its activities in the discovery and development of biological therapies targeting autoimmune and oncology conditions both in Mainland China and globally.

Estimated Discount To Fair Value: 44.2%

Keymed Biosciences is trading at HK$67, significantly below its estimated future cash flow value of HK$120.15, indicating it may be undervalued. Analysts agree on a potential 31.5% stock price increase. Despite reporting a net loss of CNY 522.64 million for 2025, revenue grew to CNY 716.31 million from CNY 428.12 million the previous year. A recent milestone payment of US$45 million from AstraZeneca supports its financial position and growth prospects in Asia’s biotech sector.

SEHK:2162 Discounted Cash Flow as at Apr 2026

Overview: Zhejiang Taotao Vehicles Co., Ltd. is involved in the research, development, production, and sale of motorcycles, electric vehicles, and ATVs both in China and internationally with a market cap of CN¥25.29 billion.

Operations: The company’s revenue is derived from its activities in the research, development, production, and sale of motorcycles, electric vehicles, and ATVs across domestic and international markets.

Estimated Discount To Fair Value: 40.6%

Zhejiang Taotao Vehicles is trading at CNY 231.9, significantly below its estimated future cash flow value of CNY 390.55, indicating potential undervaluation. The company reported a substantial increase in net income to CNY 816.32 million for 2025 from the previous year, with earnings per share nearly doubling. Despite slower projected profit growth compared to the market, revenue is expected to grow robustly at 23.3% annually, outpacing market averages.

SZSE:301345 Discounted Cash Flow as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:1364 SEHK:2162 and SZSE:301345.

This article was originally published by Simply Wall St.

Airline stocks fell collectively. As of press time, China Eastern Airlines (00670) dropped 4.6%, trading at HKD 3.73; China Southern Airlines (01055) fell 4.02%, trading at HKD 4.06. According to Zhitong Finance, airline stocks fell collectively. As of press time, China Eastern Airlines (00670) dropped 4.6%, trading at HKD 3.73; China Southern Airlines (01055) fell

Although EchoStar (NASDAQ: SATS) wasn’t exactly a stock market star on Wednesday, it did quite well on the market. Investors bid it up by 3% that day, thanks to news from a company the satellite specialist has had plenty of dealings with over the years. That company has significant star power all on its own.

Nvidia (NASDAQ: NVDA) has made many big moves in recent years, from launching the most powerful artificial intelligence (AI) chips and systems to becoming the first company to reach $4 trillion in market capitalization. The tech giant wisely identified the potential AI opportunity about a decade ago and set its sights on dominating the market.

One of the key pillars of investing is diversification. This means investing in companies across different industries, sizes, and regions around the world. When it comes to different regions, one of the best ways to get exposure is to invest in thousands of them at once through an international exchange-traded fund (ETF). That’s why I’m

Shares of Sandisk (NASDAQ: SNDK) were moving higher today after the maker of flash memory products gained in sympathy with memory chip leader Micron (NASDAQ: MU), which bounced back after a bullish note from Cantor Fitzgerald this morning. That set off something of a relief rally in the memory sector, which had been pounded in

The upgrading of the Greek bourse to the category of developed markets by Morgan Stanley starting in May 2027, with the upcoming MSCI index rebalancing, gave a massive boost to Greek stocks on Wednesday, with the benchmark covering a significant part its recent losses in the last couple of days. The postponement of the upgrading

The firm delivers a new strategy that provides targeted exposure to India’s equity market using a disciplined, factor-based approach MALVERN, Pa., April 01, 2026–(BUSINESS WIRE)–Pacer ETFs (“Pacer”), the leading U.S. issuer in free cash flow ETFs, today announced the launch of the Pacer ActiveAlpha India Quality ETF (Nasdaq: INDQ). The fund, part of Pacer’s Custom

Shares in integrated major energy company Chevron (CVX 5.48%) declined by 4.6% to 11:30 a.m. The stock fell as the price of oil dipped by a couple of percentage points to below $100 a barrel. That was enough to encourage selling from investors buying into stocks like Chevron and other highly liquid energy stocks as

The stock market isn’t off to a good start to 2026. Multiple issues are weighing on stocks today, including the war in Iran, elevated oil prices, and question marks still loom about just how strong the economy really is. Plus, the market has been hot for multiple years now — it may be overdue for

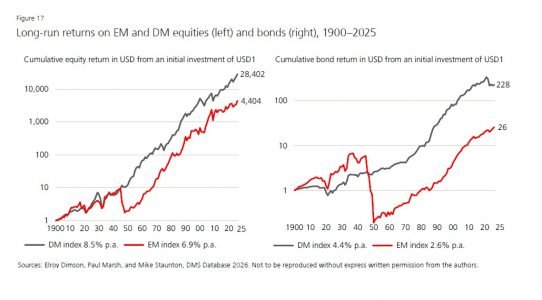

A significant shift can also be observed in the sectors that have dominated global markets. Of the U.S. listed companies in 1900, nearly 80% of their value was concentrated in sectors that are now small or have disappeared, such as railroads, textiles, iron, coal, and steel. Meanwhile, 70% of today’s U.S. companies come from sectors

OpenAI released its groundbreaking artificial intelligence (AI) chatbot, ChatGPT, in November 2022, and by January 2023, it had amassed 100 million users. This was the moment AI went mainstream, and since then, companies operating in this emerging industry have experienced astronomical growth. Nvidia stock, for example, is up tenfold since the start of 2023, while

Image source: Getty Images The stock market feels increasingly volatile right now. News is developing fast, sentiment is shifting quickly, and investors are reacting to every new development. But beneath the surface, something more important is happening. This doesn’t look like a market breaking down — it looks like one that’s changing. Right now, the

If investors are coming up with a list of the best stocks of this century, there’s no doubt that Netflix (NFLX +3.32%) would be in that group. It’s certainly one of the most disruptive businesses on the planet. And the performance of its shares, which have risen a jaw-dropping 22,700% in the past two decades,

Big tech is still pouring billions into the data centers powering artificial intelligence (AI) — and the spending wave doesn’t appear to be peaking anytime soon. Statista projects AI infrastructure investment will climb to $902 billion by 2029, up from $334 billion in 2025. Even after strong runs, some of the market’s biggest AI winners,

Dip-buying has begun in earnest after a rocky few weeks for stocks that saw the S&P 500 fall as much as 9%. One Wall Street strategist says it’s right on cue. Loading audio narration… Stocks ripped on Tuesday on the prospect of cooling tensions between Iran and the US, with the S&P 500 and Nasdaq

Fear is in the air. Sure, the S&P 500 (SNPINDEX: ^GSPC) is holding up pretty well in the face of significant uncertainty. However, implied volatility has risen sharply in recent weeks. Should investors stay away from all stocks with a 10-foot pole? Nope. Here are three dividend stocks you can buy with no hesitation. Will

The London stock market has recently faced downward pressure, with the FTSE 100 and FTSE 250 indices slipping due to weak trade data from China, highlighting ongoing global economic challenges. Despite these broader market conditions, penny stocks—often representing smaller or newer companies—continue to attract interest for their growth potential at more accessible price points. While

Robot concept stocks rose in the afternoon. As of press time, Woan Robotics (06600) surged 17.17% to HKD 107.2; Ubtech Robotics (09880) rose 16.51% to HKD 99.5; Hesai-W (02525) climbed 12.17% to HKD 158.5; and LK Technology (00558) increased by 8.85% to HKD 2.83. According to Zhitong Finance APP, robot concept stocks rose in the