1 Glorious Growth Stock, Down 81%, You Might Regret Not Buying on the Dip in March

Duolingo(NASDAQ: DUOL) operates the world’s largest digital language-education platform. Unfortunately, that hasn’t kept its stock from plummeting by 82% from its mid-2025 all-time high. The drop is primarily tied to two reasons:

Investors are worried that artificial intelligence (AI) will disrupt its business.

Management plans to target faster user growth, which is likely to affect sales and profits.

I think those concerns are overwrought. Regarding the first issue, Duolingo has actually proven that AI can be a tailwind for its business, rather than a serious threat. As for the second, while the shift in its business strategy could temporarily result in slower revenue and earnings growth, the company believes it can almost double its daily active users (DAUs) between now and 2028.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

If I’m right, the sharp decline in Duolingo stock presents a great long-term buying opportunity, especially because the stock is trading at the cheapest valuations it has ever been since going public in 2021.

Image source: Getty Images.

Duolingo takes a mobile-first approach to education, so it can provide interactive and highly engaging lessons to anybody with a smartphone or tablet computer. Its platform had 52.7 million DAUs at the end of 2025, which was a 30% increase from the year-ago period, so its strategy is clearly resonating.

The company monetizes its platform by showing ads to free users, and by offering a series of subscription options for eager learners who want to accelerate their progress by unlocking extra features. A record 12.2 million users were paying for a subscription at the end of 2025, a figure that was up 28% year over year.

AI has been a major drawing card for subscribers. In 2024, Duolingo launched a feature called Video Call, which enables users to practice their foreign-language speaking skills with a digital avatar named Lily, and it’s only available to users who pay for Super Duolingo or Duolingo Max subscriptions.

Subscribers who choose the more expensive Max subscription option also gain access to other AI features like Roleplay, which challenges them to solve different problems through a chatbot-style interface to improve their conversational skills.

Duolingo plans to integrate AI into the free learning experience, too, as part of its broader goal to attract more users. Most free lessons are completed by typing or tapping answers, but the company wants to make spoken language a more prominent medium, which is only now possible thanks to AI.

In 2025, Duolingo generated a record $1.04 billion in revenue, a 39% increase from the prior year. The company also had a record year at the bottom line, producing $414.1 million in net income based on generally accepted accounting principles (GAAP), an amount that was up by an eye-popping 367%.

But as mentioned above, investors worry that those blistering growth rates are now on the chopping block as monetization becomes a secondary priority to user growth. Management believes investing more aggressively in acquiring users will lead to much better financial results in the long run, which makes sense because the platform will have more prospects to convert into paying subscribers. Plus, a larger user base will make Duolingo’s “position as the leading education app in the world” more defensible and harder to disrupt.

On a positive note, Duolingo is a capital-light business, and its soaring 2025 profit suggests it has plenty of room to invest more money in growth. In fact, the company spent just $125.7 million on marketing last year, a mere 20% of its total operating costs.

Boosting marketing spending would be a surefire way to supercharge user growth. By 2028, management believes Duolingo could be serving 100 million DAUs, which would be almost double the 52.7 million it serves today.

Following the 82% sell-off from last year’s all-time high, Duolingo stock has landed at a very attractive valuation. Its price-to-sales (P/S) ratio is now just 4.8, which is not only the cheapest level since going public, but also a whopping 70% discount to its average of 16.3.

Moreover, based on Duolingo’s 2025 earnings of $8.31 per share, its stock now trades at a price-to-earnings (P/E) ratio of just 12.1. For some perspective, that’s half the P/E of the S&P 500, which is 24.6 as I write this.

With that said, Duolingo’s earnings could take a hit during 2026 as part of management’s strategy shift, so its P/E might actually be higher later this year even if its stock doesn’t produce any upside. Wall Street’s consensus estimate (provided by Yahoo! Finance) suggests the company’s 2026 earnings will shrink to $7.23 per share, but that places its stock at a forward P/E of 13.9, which is still extremely attractive.

Although prospective shareholders might have to endure a period of slower revenue and earnings growth, they appear to be getting a fantastic price for Duolingo stock right now. If the company does reach 100 million DAUs by 2028, and investors look back on this moment, they might be very glad they bought the stock today.

Before you buy stock in Duolingo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Duolingo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $522,791!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,132,678!*

Now, it’s worth noting Stock Advisor’s total average return is 952% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Duolingo. The Motley Fool has a disclosure policy.

If the US-Israel war rages on, the repercussions for investors could continue for years. Richard Haass, former president of the Council on Foreign Relations, told Yahoo Finance’s Opening Bid that the days of ignoring global conflict are over. He specifically dismantled the theory that markets will return to a normal baseline. “When you had oil

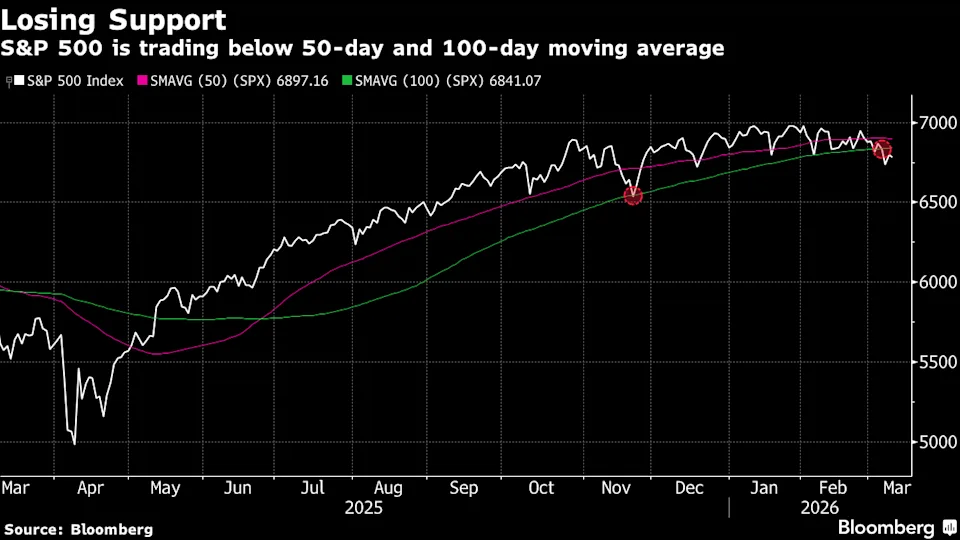

(Bloomberg) — Wall Street traders are poring over charts to determine how much further the S&P 500 Index might fall as war in the Middle East rages on, with technical analysts noting early signs of bearish momentum. The S&P 500 fell 0.2% on Tuesday, dropping further below both its 50- and 100-day moving averages. Breaching

Lamb Weston Holdings, Inc. (NYSE:LW) is one of the stocks Jim Cramer discussed amid the reshuffling of the S&P 500. Cramer highlighted the major decline in the stock over the past couple of years, as he said: Third, Lamb Weston sells frozen potatoes. They dominate that entire business. The company was spun off by Conagra

Top News Highlights Before the market opened on Wednesday, U.S. stock index futures for the three major indices collectively declined after the release of February’s CPI data. As of the time of writing, Dow Jones futures were down 0.32%, Nasdaq futures fell 0.16%, and S&P 500 futures dropped 0.18%. $Star Tech Stocks (LIST2518.US)$Most stocks rose

Key Points It’s hard to wrap your head around the amount of money that’s being spent on AI-related computing resources. To fund these investments, even companies in top financial shape have entered into unique and complex deals. No one has any clue what the eventual payout of the unprecedented AI investment boom will be. Over

No trend has been more responsible for powering the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite to new heights than the evolution of artificial intelligence (AI). Empowering software and systems with the tools to make split-second decisions without human oversight is a game changer with multitrillion-dollar global implications. While a long list of

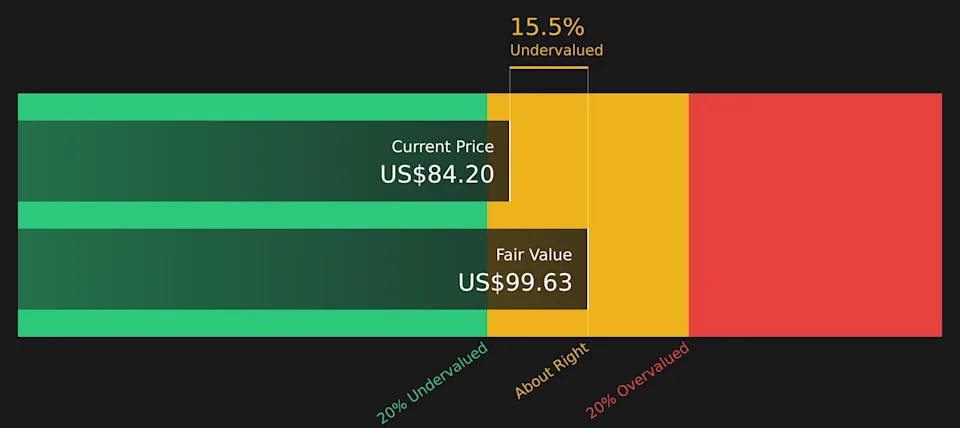

Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St. If you are wondering whether Fortinet’s current share price still offers value, you are not alone, especially with cybersecurity staying front of mind for many investors. Fortinet’s stock closed at US$84.20, with returns of 3.8%

Since 1957, the S&P 500 (^GSPC 0.21%) has returned an average of 184% during bull markets. But the index has only returned 54% since the current bull market began on Oct. 12, 2022, and I doubt it will come anywhere close to the average. In fact, I think the bull market will end in 2026

March 10, 2026, 2:48 p.m. ET Rising gasoline prices and a wobbly stock market are increasing the risk that the U.S.-Israeli war on Iran could hit hard among consumers across the economic spectrum in the United States, undercutting a key prop of economic growth that had been expected to surge this year on the basis

Asian stock markets generally rose today (March 11). Oracle (ORCL.US) raised its annual revenue guidance, driving significant gains in semiconductor stocks across the Asia-Pacific region. Taiwan’s stock market surged over 4%, while South Korea’s and Japan’s markets climbed 3.8% and 2.6%, respectively. The fourth session of the 14th National Committee of the Chinese People’s Political

Shares of financial software maker Intuit (NASDAQ: INTU) have taken a massive beating this year. While the S&P 500‘s year-to-date return is about flat, Intuit stock has plunged. Indeed, shares traded as low as $349 at one point this year. While the stock is now trading well above this low, it’s still down more than

Foodservice packaging supplier Karat Packaging (NASDAQ:KRT) will be announcing earnings results this Thursday afternoon. Here’s what investors should know. Karat Packaging met analysts’ revenue expectations last quarter, reporting revenues of $124.5 million, up 10.4% year on year. It was a slower quarter for the company, with a significant miss of analysts’ EPS estimates. Is Karat

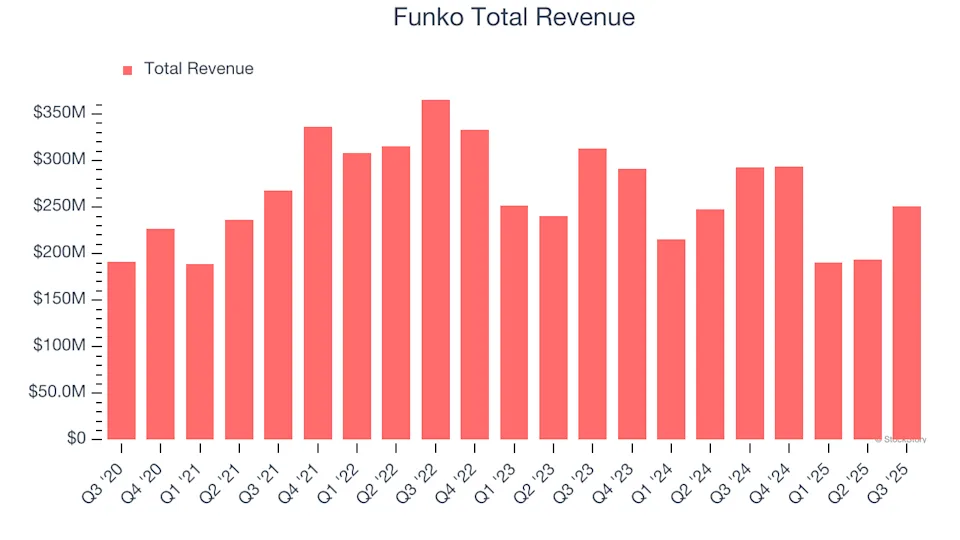

Pop culture collectibles manufacturer Funko (NASDAQ:FNKO) will be reporting earnings this Thursday after market close. Here’s what investors should know. Funko missed analysts’ revenue expectations last quarter, reporting revenues of $250.9 million, down 14.3% year on year. It was a very strong quarter for the company, with a beat of analysts’ EPS estimates and a

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE. XPeng (NYSE:XPEV) has been drawing attention after a period of mixed share performance, with a roughly 2.3% move over the past day, a stronger gain

Today’s Change (1.13%) $2.07 Current Price $184.72 Key Data Points Market Cap $4.4T Day’s Range $182.01 – $186.44 52wk Range $86.62 – $212.19 Volume 6.7M Avg Vol 177M Gross Margin 71.07% Dividend Yield 0.02% Nvidia (NVDA +1.13%), a developer of GPUs and AI solutions for gaming, data centers, and autonomous vehicles, closed at $184.77, up

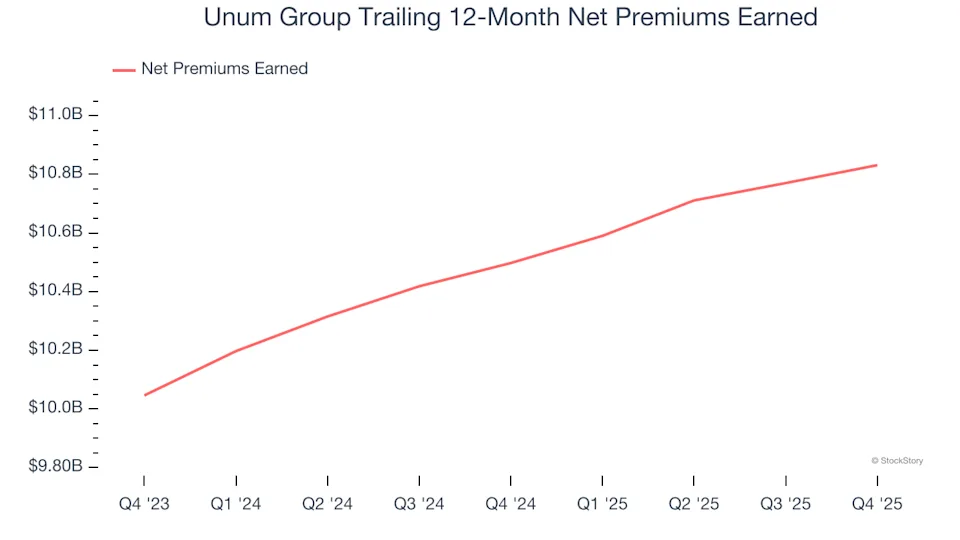

Unum Group has been treading water for the past six months, recording a small loss of 2.4% while holding steady at $71.99. The stock also fell short of the S&P 500’s 3.1% gain during that period. Is now the time to buy Unum Group, or should you be careful about including it in your portfolio?

An analyst initiated coverage of Coeur Mining (CDE +2.93%) on Tuesday, and many investors followed his advice by buying shares of the company. An uptick in gold and silver prices didn’t hurt either. Over the course of the trading day, the company’s stock rose by nearly 3% while the S&P 500 index dipped by 0.2%.

Dipping 1.4% during regular trading hours today, Oracle (ORCL 1.43%) stock is shooting higher during after-hours trading. With the tech company reporting third-quarter 2026 financial results that surpassed analysts’ expectations — and another positive development, investors have found motivation to click the buy button. As of 4:51 p.m. ET, shares of Oracle are up 7.8%

The stock market is full of bargains — the question is which ones are true bargains and which ones are companies that are being sold off for a good reason. I think three that are down a bit from all-time highs yet look like solid investment picks are Nvidia (NVDA +1.13%), Microsoft (MSFT 0.95%), and

Business intelligence platform Domo (NASDAQ:DOMO) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 1.1% year on year to $79.63 million. Its non-GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates. Is now the time to buy Domo? Find out in our full research report. Revenue: $79.63 million