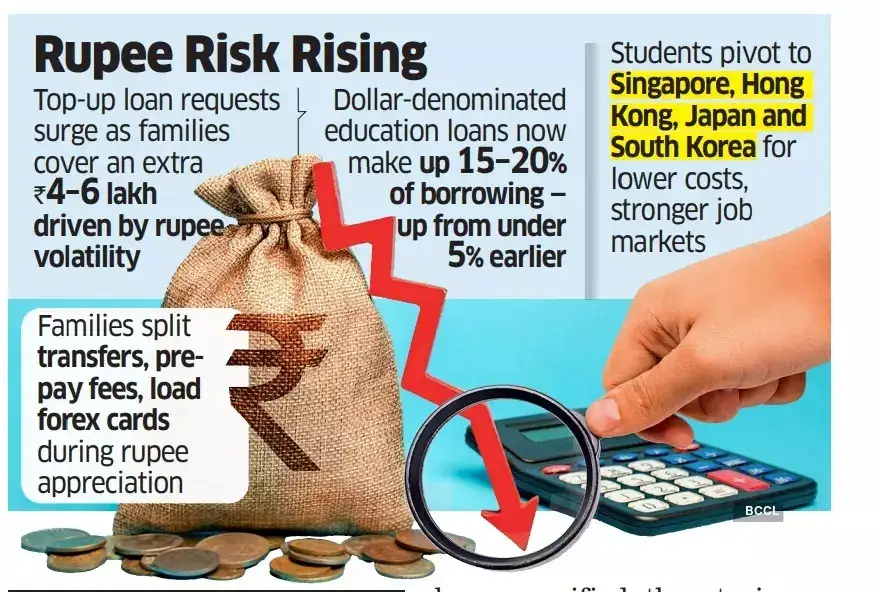

From monitoring daily rate movements for topping up forex cards during periods of rupee appreciation to restructuring remittances, this admissions cycle has turned sophisticated financial planning into a second full-time job for many households, say study abroad experts.

The rupee is down 5.3% against the US dollar this year, while its slide has been even sharper against other key currencies like the pound and euro. This has magnified the strain on education loans—previously approved rupee loans are falling short when converted into foreign currencies and new borrowers are forced to increase loan size to account for the exchange rate.

“We’re seeing education loan amounts increase by 12-15% year-over-year across all major destinations,” said Nikhil Jain, founder of ForeignAdmits. “The biggest change is the surge in top-up loan applications. Students who locked in the loan amounts 6-9 months ago now need an additional `4-6 lakh due to currency movement.”

A clear shift is also underway in how families try to protect themselves against currency fluctuations. An increasing number of these borrowers are taking dollar-denominated loans offered by certain nonbank finance companies.

“We’re seeing 15–20% of new borrowers opting for dollar-denominated loans, up from under 5% two years ago,” Jain said. But not everyone can hedge, he cautions.

“Most families funding through education loans cannot ‘time the market’ because they do not have spare capital” if they need to rebalance the loans, explains Jain. Saurabh Arora, founder of University Living, said the rupee’s depreciation has increased the overall education budget for most students by 8–12%. The rise is primarily seen in tuition instalments, living expenses, and initial deposits that must be paid in foreign currency.

Families are adapting to this in smaller, incremental ways, he said. Many are spreading out their payments, reconsidering enrolments, or delaying non-essential remittances until the exchange rate is more favourable.

Meanwhile, many are looking at lower-ranked universities outside the top education destinations of the US, UK, Canada and Australia, if they get good scholarships and the job prospects are clear. This shift has been visible in the education loan portfolios of lenders even before the latest round of rupee depreciation started.

“The Big Four’s dominance has collapsed. The US-UK-Canada-Australia share has dropped from roughly 80% to 60% over two years,” while Germany, France and the Netherlands are gaining, Jain said. Conversations on return on investment, Arora said, “have become more structured and analytical” and now include “cost of living, part-time job availability, and the stability of the host country’s immigration and labour policies.”

ASIA ON THE RADAR

The high expense of western education is also driving a shift in the geographic choices of students to Asia, said Collegify founder Adarsh Khandelwal. “This is the first admissions cycle where Asian education hubs are becoming the most rational Plan B, not Europe,” because the rupee has weakened against both the US dollar and the euro, he said.

The sharpest rise is in “Singapore, Hong Kong, Japan, and South Korea”, where degrees are short, the job market is strong and living costs are structured.

Premium Asian universities like “NUS, NTU, SMU, HKU, HKUST, Tokyo, Kyoto, KAIST and Yonsei” are now being chosen over mid-tier Western institutions, while Dubai, Abu Dhabi and Kuala Lumpur are emerging as “value” destinations, Khandelwal said.