Surge in Hong Kong dollar bonds to continue after record US$42 billion year

Hong Kong dollar bond issuance is poised to expand, following a record run of offerings, as easing local interest rates attract more issuers while a global diversification trend persists, according to analysts.

Total issuance in the city’s currency reached a record HK$331 billion (US$42.6 billion) so far this year, nearly 37 per cent higher than 2024’s full-year total of HK$242 billion.

“The Hong Kong dollar bond market will continue to grow over the long term, supported by structural shifts,” said Oliver Greer, global head of medium-term notes at Standard Chartered.

Do you have questions about the biggest topics and trends from around the world? Get the answers with SCMP Knowledge, our new platform of curated content with explainers, FAQs, analyses and infographics brought to you by our award-winning team.

Amid a global shift to diversify away from the US dollar, the Hong Kong dollar emerged as a logical choice for Asian investors, supported by its long-standing US dollar peg and a deep, liquid market underpinned by a clear legal and capital framework, Greer said. The city’s low inflation also translated into higher real returns for bond investors, he added.

Many issuers were broadening their funding mix as US dollar rates remained elevated, said Terrence Pang, portfolio manager at Fidelity International.

“The Hong Kong dollar has offered more competitive all-in costs, particularly for borrowers with natural Hong Kong dollar needs or balance-sheet alignment,” he said.

The Hong Kong dollar bond market has expanded steadily in recent years, but the latest surge was driven by the exceptionally low Hong Kong interbank offered rate (Hibor) earlier this year, which sharply reduced funding costs.

Although the rate gap between Hong Kong dollars and US dollars narrowed recently, Hong Kong dollar interest rates were still likely to stay below US dollar levels because of the city’s lower inflation, Greer said.

“We forecast a continued decline in Hibor throughout 2026, in tandem with the Federal Reserve’s aggressive rate-cutting trajectory,” said Carlos Casanova, an economist at Swiss private bank UBP. “We project a reduction of at least 100 basis points.”

Additionally, the Hong Kong dollar public bond market saw its first international issuer this year, issuing a so-called wonton bond, named after a type of Chinese dumpling.

Oliver Greer, global head of medium-term notes at Standard Chartered, pictured on November 27, 2025. Photo: Jonathan Wong alt=Oliver Greer, global head of medium-term notes at Standard Chartered, pictured on November 27, 2025. Photo: Jonathan Wong>

Foreign entities issuing public bonds in Hong Kong dollars is a departure from their typical practice of using private channels to tap the local currency. The Asian Infrastructure Investment Bank set the precedent by issuing a HK$4 billion three-year bond in February.

The transaction list grew to eight this year, with Korea Expressway raising a HK$2 billion note last week as the latest and first corporate wonton-bond issuer.

“After years of virtually no international public Hong Kong dollar deals, one transaction quickly led to seven more in a year,” Greer said. “The market has matured to a point where international issuers choose to come here because pricing is more attractive and the size is significant.”

Issuance of wonton bonds this year totalled HK$28.9 billion. It could grow further next year as more supranationals and agencies debut or revisit the market, according to analysts.

“Many supranationals and agencies now see this as a long-term market where they plan to be repeat borrowers,” said Greer. “In 2026, we will likely see a number of debut international issuers doing Hong Kong dollar public deals, and the pipeline looks healthy.”

The outlook for Hong Kong dollar bonds next year was “constructive”, supported by fiscal and policy measures that continue to drive funding needs from government, quasi-sovereign and other high-grade local issuers, Pang said, pointing to infrastructure initiatives like the Northern Metropolis.

Local institutional investors tended to be “sticky” too, he added.

“Banks, insurers, [Mandatory Provident Fund] schemes and other long-term buy-and-hold types of investors provided support in the primary and secondary markets,” he said. “Loan-to-deposit ratios have fallen meaningfully since 2022, increasing banks’ and insurers’ appetite for high-quality carry assets.”

As mainland Chinese banks’ offshore balance sheets grew, Hong Kong became a natural funding centre and reinforced the case for allocating a larger share to Hong Kong dollars, Greer said.

Overall, the structural backdrop, including a rate-cutting cycle and tight credit spreads – an indicator that investors see low risk and demand little extra yield over safer government bonds – was expected to support Hong Kong dollar bond issuance, Greer said.

“If this supportive risk sentiment persists and the Fed delivers the expected rate cuts, 2026 is likely to be another strong year for Hong Kong dollar bond issuance,” he said.

More than a year before a massive blaze tore through the Wang Fuk Court housing estate in Hong Kong, residents had raised an alarm over the use of flammable construction materials during ongoing renovation works. Their concerns, largely dismissed at the time, have now resurfaced at the centre of a widening investigation into one of

The 1980s marked a period of profound uncertainty for Hong Kong. With the 1997 handover to China looming and the signing of the Sino-British Joint Declaration in 1984, many residents, particularly the burgeoning middle class, sought stability elsewhere. This political anxiety spurred a significant wave of emigration as people looked to secure foreign passports and

The government should take the lead in assessing the structural safety of the estate engulfed by Hong Kong’s worst fire in decades before deciding whether it should be restored or redeveloped, experts have said, warning of liability problems and a long road ahead. The future of Wang Fuk Court, where a massive fire raged through

This story has been made freely available as a public service to our readers. Please consider supporting SCMP’s journalism by subscribing. Get faster notifications on the latest updates by downloading our app. What we know so far: 128 people, including a firefighter, confirmed dead 79 injured, including 12 firefighters Status of 200 people unclear The

Two hundred still missing, search and rescue ended Eleven arrested in connection with city’s worst fire in decades Hong Kong officials hold three-minute silence on Saturday Britain’s King Charles sends condolences for ‘appalling tragedy’ HONG KONG, Nov 29 (Reuters) – Hong Kong on Saturday mourned the 128 people known to have died in a massive

When Alvin Kwock, co-founder of digital insurer OneDegree, took part in the inaugural Hong Kong FinTech Week in November 2016, it was held at a venue suitable for only a few hundred people. “As it was the first ever fintech event in Hong Kong, only fintech start-ups were interested, no big financial institutions paid attention,”

Systemic failings around supervision of building maintenance in Hong Kong, and a lack of coordination between departments charged with ensuring it is done properly, both needed to be addressed to prevent tragedies such as the Tai Po fire happening again, experts and sector representatives have said. The regulation of polystyrene foam boards was particularly important,

Systemic failings around supervision of building maintenance in Hong Kong, and a lack of coordination between departments charged with ensuring it is done properly, both needed to be addressed to prevent tragedies such as the Tai Po fire happening again, experts and sector representatives have said. The regulation of polystyrene foam boards was particularly important,

HONG KONG, Nov. 29, 2025 /PRNewswire/ — In response to the devastating No. 5 alarm fire at Wang Fuk Court, Tai Po, ANKH Pain Relief Health Group has donated HK$1 million to the Hong Kong Red Cross to support their “Tai Po Fire Emergency Appeal”. The major blaze at Wang Fuk Court has caused serious casualties and

HONG KONG, Nov. 29, 2025 /PRNewswire/ — In response to the devastating No. 5 alarm fire at Wang Fuk Court, Tai Po, ANKH Pain Relief Health Group has donated HK$1 million to the Hong Kong Red Cross to support their “Tai Po Fire Emergency Appeal”. The major blaze at Wang Fuk Court has caused serious casualties and

If there’s one piece of advice Andre Agassi offers, it’s to dream while awake. “It’s way too easy to dream when you’re sleeping,” says the American tennis legend. “Don’t be scared to dream big because it takes as much effort to dream big as it does small.” He advises choosing your definition of success carefully.

Leaving Prince of Wales Hospital in Sha Tin on Thursday, unaware of the whereabouts of some of his relatives, a 76-year-old man surnamed Lam was left uncertain how to arrange the funeral of his older brother, who had just died in Hong Kong’s worst fire in seven decades. He arrived at the interdepartmental help desk

Emperor International Holdings has secured bank approval to resume borrowing under existing terms by nearly two years, providing the embattled Hong Kong developer with much-needed breathing room after it failed to meet HK$16.6 billion (US$2.13 billion) in debt obligations in July. Meanwhile, shares of Lai Sun Development (LSD) resumed trading on the Hong Kong stock

The death toll from Hong Kong’s deadliest fire in seven decades climbed to more than 100 on Friday as the government announced a three-day official mourning period from Saturday for victims of the blaze. National and Hong Kong flags at all its buildings and facilities will fly at half-mast until Monday, with officials cancelling all

Occasional outbursts of children’s laughter were heard on Friday morning at one of the shelters set aside for residents left homeless by a deadly inferno at a Tai Po housing estate in Hong Kong, as classes were still suspended in some of the schools in the aftermath. Scattered across different corners at Tung Cheong Street

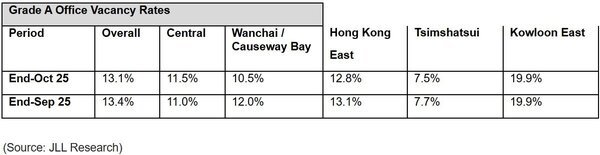

Email Sign Up For Our Free Weekly Newsletter Hong Kong’s Central district posted its first rise in Grade A office rents in more than two years, as tightening vacancy in top-tier towers bolstered landlord confidence, according to new data from JLL. Average Grade A rents in Central edged up 0.1% in November from the prior

The failure of fire alarms in the deadly Tai Po blaze could have delayed the response and evacuation of residents, according to a leading Hong Kong fire safety specialist. Anthony Lam Chun-man, a former director of the Fire Services Department, also said the extreme heat and intense flames both inside and outside made it almost

William Li, 40, is one of the survivors of Hong Kong’s Tai Po fire tragedy. The deadliest inferno in decades set seven blocks in the Wang Fuk Court residential complex ablaze, claiming at least 128 lives as of Friday. Li was rescued from Wang Cheong House – the block that first caught fire – on

Families of residents still missing after a blaze engulfed an estate complex in Hong Kong on Wednesday face an agonising wait for news of their loved ones as the government needs more time to identify many of the bodies. Secretary for Security Chris Tang Ping-keung said on Friday that among the 89 unidentified bodies so